Quick Summary: Yes, it is possible to pay for college with cash through savings, payment plans, and income without taking loans. Most families use a combination of grants, scholarships, 529 plans, and out-of-pocket funds. According to College Board data, many students cover costs using multiple payment methods simultaneously, making cash-based education achievable with proper planning.

The idea of paying for college entirely with cash might sound impossible in today’s economic landscape. With tuition costs climbing year after year, many families assume that student loans are the only viable path forward.

But here’s the reality: thousands of students graduate debt-free every year. They’re not all trust fund beneficiaries or lottery winners. They’re regular families who planned strategically, leveraged available resources, and made informed choices about how to fund higher education.

According to College Board, most families pay for college using some combination of savings, income, and financial aid. The key word there? Combination. Rarely does a single funding source cover everything, but when families stack multiple cash-based strategies together, they can eliminate or dramatically reduce the need for loans.

This guide breaks down the most effective methods for paying college expenses without borrowing. Some strategies work better for families who started planning early, while others can help even if college is just months away.

Understanding the True Cost of College

Before exploring payment strategies, it’s crucial to understand what families actually pay versus what colleges advertise.

The sticker price—what schools publish in brochures and websites—represents the maximum cost. But according to NACUBO data, net price (what students actually pay after scholarships and aid from federal, state, and institutional sources) is considerably lower than the sticker price across all institution types.

This distinction matters enormously when planning how to pay cash for college. A school with a $50,000 sticker price might cost a specific family only $25,000 after grants and institutional aid. That’s still a substantial amount, but it’s far more manageable from a cash-flow perspective.

Tuition itself typically doesn’t include all charges. According to the U.S. Department of Education resources, cost of attendance encompasses tuition, fees, room and board, books, supplies, transportation, and personal expenses. Families focusing on cash payment need to account for this complete picture, not just the tuition line item.

What Tuition Actually Covers

As NACUBO explains, tuition is the price institutions charge for courses. But what does that money fund? It supports faculty salaries, academic resources, facilities maintenance, technology infrastructure, and countless administrative functions that keep the educational experience running.

Understanding this helps families evaluate whether they’re getting value for their cash investment. It also clarifies why different institutions have vastly different price points—community colleges operate with different cost structures than private research universities.

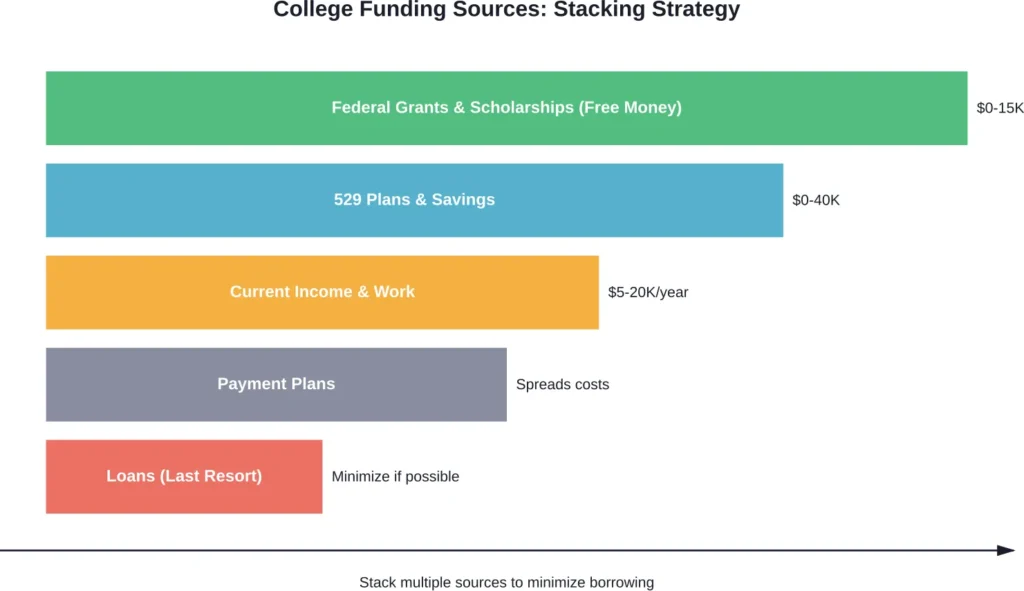

Free Money First: Grants and Scholarships

The absolute best way to “pay” for college with cash is to reduce how much cash is needed in the first place. Grants and scholarships represent money that never needs to be repaid, effectively lowering the sticker price to something more manageable.

Federal Grants

Federal Pell Grant stands as the foundation of federal grant aid. According to Federal Student Aid data, the maximum scheduled award for 2024-25 is up to $7,395. While that doesn’t cover full tuition at most four-year institutions, it significantly reduces the cash burden for eligible families.

Here’s what many families don’t realize: even those earning over $100,000 may qualify for federal aid through the FAFSA, especially when multiple children attend college simultaneously. According to Sallie Mae’s How America Pays for College 2025 study, 3 in 10 families skipped the FAFSA, and misconceptions about financial aid eligibility may be costing families more money than necessary.

The Federal Supplemental Education Opportunity Grant (FSEOG) provides additional funding for students with exceptional financial need. These grants are campus-based, meaning the school’s financial aid office determines eligibility and award amounts.

Scholarship Strategies

Scholarships come from countless sources: institutions themselves, private organizations, corporations, community groups, and specialty foundations. The challenge isn’t finding scholarships—it’s applying to enough of them consistently.

Institutional scholarships often represent the largest awards. Many colleges automatically consider admitted students for merit aid based on their application. But plenty of opportunities require separate applications, essays, or portfolios.

Private scholarships vary wildly in scope. Some award $500, others provide full tuition. Some financial institutions offer scholarships toward tuition; for example, certain annual scholarship programs may provide substantial awards with no purchase necessary. Small awards add up—ten $1,000 scholarships equal $10,000 in cash a family doesn’t need to produce from savings or income.

Community discussions on forums reveal that successful scholarship applicants treat the process like a part-time job during senior year. They set weekly application goals, reuse essays where possible, and cast a wide net across local, regional, and national opportunities.

Tax-Advantaged Savings Plans

For families with time before college starts, tax-advantaged savings vehicles offer powerful ways to accumulate cash for education expenses.

529 College Savings Plans

These state-sponsored investment accounts allow families to save for college with significant tax benefits. According to College Board, contributions grow tax-free, and withdrawals for qualified education expenses aren’t taxed either.

The earlier families start contributing, the more time investment growth has to compound. Even modest monthly contributions can build substantial balances over 10-15 years. But here’s something many overlook: it’s never too late to start. Even opening a 529 plan when a child is in high school provides some tax-advantaged growth, and contributions from relatives can quickly boost the balance.

Different states offer different 529 plans with varying investment options, fees, and state tax benefits. Some states provide tax deductions or credits for contributions, effectively giving residents an immediate return on their savings.

Other Savings Vehicles

While 529 plans offer the best tax treatment specifically for education, families might also accumulate college funds in regular savings accounts, Roth IRAs (contributions can be withdrawn penalty-free), or taxable investment accounts.

The key principle remains the same: consistent saving over time, even in small amounts, creates cash reserves that reduce reliance on borrowing. As College Board notes, families can save for college costs tax-free through 529 plans, making them the optimal vehicle when available.

Working Your Way Through College

Earning income while enrolled provides cash to cover immediate expenses and reduces the amount families need to produce from savings or loans.

Federal Work-Study Programs

Federal work-study provides part-time jobs for undergraduate and graduate students with financial need. These positions are often on-campus and designed to work around class schedules. The program is funded partially by the federal government, encouraging schools to hire eligible students.

Work-study earnings go directly to students, who can use the money for tuition, fees, books, or living expenses. The key advantage? Work-study income receives favorable treatment in financial aid calculations for subsequent years.

Part-Time Employment

Students can also work regular part-time jobs outside the work-study program. Many find positions in retail, food service, tutoring, or campus roles that aren’t work-study designated.

The trade-off involves balancing work hours against academic performance. But for motivated students, earning $5,000-$10,000 annually through part-time work makes a substantial dent in college costs. That’s $20,000-$40,000 over four years—potentially the difference between graduating debt-free or carrying significant loans.

Some students leverage specialized skills for higher pay. Freelance writing, graphic design, web development, or tutoring in high-demand subjects can generate significantly more per hour than minimum wage.

Summer and Break Employment

Full-time summer work represents an even bigger earning opportunity. A student working full-time for three months at minimum wage or higher earns several thousand dollars before taxes. Working summers between high school and college, then after each college year, could generate $30,000 or more over four years.

Some students pursue paid internships that simultaneously build career skills and generate income. While unpaid internships offer valuable experience, paid positions serve the dual purpose of professional development and college funding.

Strategic Payment Options

Even when families have the cash to pay for college, how they structure payments can provide breathing room and better cash flow management.

Tuition Payment Plans

Most colleges offer payment plans that divide semester charges into monthly installments, spreading costs across multiple months rather than requiring lump sum payments.

These plans typically charge a setup fee but no interest. That’s dramatically cheaper than borrowing. For families with steady income but limited savings, payment plans convert large, unmanageable bills into smaller, budget-able monthly obligations.

The psychology matters too. Spreading payments across the academic year makes costs feel more manageable and helps families maintain emergency funds rather than depleting savings accounts completely at the start of each term.

Employer Tuition Assistance

Many employers offer tuition assistance or reimbursement programs for employees pursuing degrees. These programs often require students to maintain certain grades and may limit assistance to courses relevant to current or future roles within the company.

For working adults returning to school, or students who can work full-time while taking classes part-time, employer assistance can cover substantial portions of costs. Some programs provide several hundred to thousands of dollars annually in direct tuition payment.

Alternative Education Paths

The traditional four-year residential college experience represents just one path to a degree. Alternative routes can dramatically reduce cash requirements while still delivering quality education and credentials.

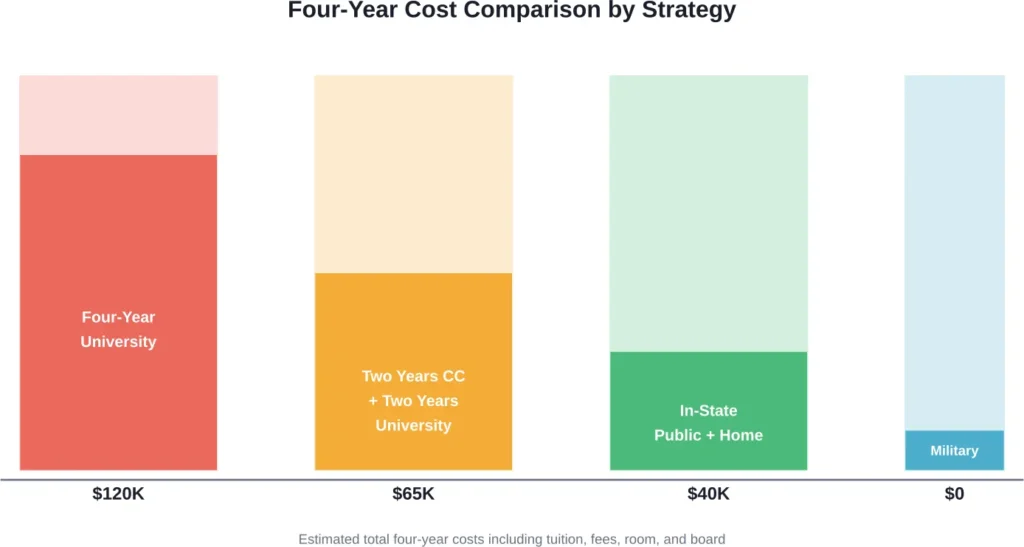

Community College Transfer

Starting at community college for general education requirements, then transferring to a four-year institution for the final two years, can cut total costs nearly in half. Community college tuition typically runs several thousand dollars per year compared to $20,000-$50,000+ at four-year schools.

Students who live at home while attending community college save even more by eliminating room and board expenses. The degree ultimately comes from the four-year transfer institution, so graduates face no credential disadvantage.

Military Service Academies

According to available data, students can apply to one of the five prestigious military academies across the country. Tuition at these institutions is $0, though the admissions process is quite rigorous. A minimum service of five years is required after graduation.

For students interested in military careers, this path provides a world-class education completely free of tuition costs while also paying a modest salary during enrollment.

ROTC Scholarships

Reserve Officers’ Training Corps programs offer scholarships that cover tuition and fees at participating colleges in exchange for military service after graduation. These scholarships are competitive but available at hundreds of institutions.

Tax Credits and Deductions

Federal tax benefits won’t pay tuition bills directly, but they return cash to families at tax time, effectively reducing the net cost of college.

American Opportunity Tax Credit

The American Opportunity Tax Credit provides up to $2,500 per eligible student per year for the first four years of higher education. It’s partially refundable, meaning families might receive up to $1,000 even if they don’t owe taxes.

To qualify, students must be pursuing a degree or credential, be enrolled at least half-time, and not have completed four years of higher education before the tax year. Income limits apply, but many middle-income families qualify.

Lifetime Learning Credit

For students beyond their first four years, graduate students, or those taking courses to improve job skills, the Lifetime Learning Credit offers up to $2,000 per tax return (not per student). It’s non-refundable but still provides valuable tax savings.

These tax benefits require careful record-keeping. Schools provide Form 1098-T documenting qualified education expenses, which taxpayers use when claiming credits.

Making It Work: Realistic Planning

Paying for college entirely with cash requires honest assessment of resources, realistic expectations, and often some compromise.

Start with the FAFSA

Every family should complete the Free Application for Federal Student Aid, regardless of income level. This single form unlocks access to federal grants, work-study, and provides the basis for institutional aid decisions.

Many families mistakenly believe they earn too much to qualify for anything. But aid formulas consider multiple children in college, unusual expenses, and other factors beyond gross income. The only way to know what aid is available is to apply.

Compare Real Costs, Not Sticker Prices

According to College Board, the sticker price of a specific college is usually higher than what most students would actually pay, thanks to financial aid. When evaluating options, compare net price—what the family will actually pay after grants and scholarships.

A $50,000 private school offering $30,000 in grants costs less than a $25,000 public university offering no aid. Schools provide net price calculators on their websites that estimate actual costs based on family financial information.

Build a Payment Strategy

Most families should plan to cover college costs through multiple sources simultaneously:

- Free money from grants and scholarships

- Savings accumulated before college starts

- Current income from parents and student during college years

- Payment plans to spread costs over time

- Tax credits that return cash at year-end

This layered approach makes cash payment realistic even when no single source covers everything. A family might cover 30% from 529 savings, 20% from grants, 15% from student earnings, 25% from parent current income, and 10% from tax credits and other sources.

| Payment Source | Typical Contribution | Best For | Timing |

|---|---|---|---|

| Federal Pell Grant | $0-$7,395/year | Lower-income families | Awarded annually |

| Institutional Scholarships | $1,000-$30,000+/year | High-achieving students | Often renewable 4 years |

| 529 Savings Plan | Varies widely | Families who started early | Available immediately |

| Student Work-Study | $2,000-$5,000/year | Students with time for work | Earned during semester |

| Student Summer Work | $3,000-$8,000/summer | All students | Before each academic year |

| Parent Current Income | Varies widely | Families with steady earnings | Monthly via payment plan |

| Tax Credits | Up to $2,500/year | Middle-income families | Refund following year |

When Cash Isn’t Enough

Real talk: not every family can cover all college costs with cash, especially without years of advance planning. That’s okay. The goal isn’t perfection—it’s minimizing debt.

If families need to borrow after exhausting cash options, federal student loans typically offer better terms than private loans. They come with fixed interest rates, income-driven repayment options, and certain borrower protections.

But even families who ultimately take some loans benefit from cash payment strategies. The difference between graduating with $40,000 in debt versus $15,000 is enormous in terms of monthly payments, interest costs, and financial flexibility after graduation.

According to Brookings Institution research on Federal Reserve data, the highest-income 40 percent of households account for a disproportionate share of student loan debt—and an even larger share of monthly out-of-pocket student debt payments. This suggests that many families could pay cash for more of their education costs but choose to borrow instead, sometimes unnecessarily.

What About Graduate School?

The strategies discussed apply primarily to undergraduate education, but many principles extend to graduate programs as well.

Graduate students can’t receive Pell Grants, but they remain eligible for federal unsubsidized loans, work-study, and certain fellowships or assistantships. Many graduate programs offer teaching or research positions that provide tuition waivers plus stipends, effectively making advanced degrees free for students who secure these positions.

Professional programs like law or medicine typically require significant borrowing, but students can still minimize debt through scholarships, part-time work, and living frugally.

Frequently Asked Questions

Most colleges accept payment via check, electronic bank transfer, credit card, or payment plan—physical currency is rarely accepted for large tuition payments due to security and accounting concerns. When people talk about paying for college with cash, they typically mean using savings and current income rather than borrowed funds.

This depends on the child’s age and target college costs. For a family starting when a child is born and aiming to cover substantial college costs 18 years later, consistent monthly contributions to a 529 plan with tax-advantaged growth could help reach that goal.

Outside scholarships typically reduce the aid package a college offers, but they usually replace loans and work-study first before reducing grants. The net effect is still positive—families pay less out of pocket. However, policies vary by institution, so students should check with financial aid offices about how outside scholarships affect their specific packages.

Financial planners generally advise against raiding retirement accounts to pay for college. Early withdrawal penalties, taxes, and lost retirement growth often cost more than student loan interest. Students can borrow for college, but nobody offers loans for retirement. Families should maximize other options before touching retirement funds.

Lack of savings doesn’t preclude cash payment—it just requires more reliance on current income, student earnings, grants, and scholarships. Many students from families with zero college savings graduate debt-free by attending affordable schools, working throughout college, earning scholarships, and using payment plans to manage cash flow.

Colleges typically charge a setup fee and divide the semester’s charges into equal monthly payments over 4-6 months. There’s usually no interest, making these plans essentially free financing. Families apply each semester, and automatic bank withdrawals handle the monthly payments.

Research shows working 10-15 hours per week generally doesn’t harm academic performance and may actually improve time management skills. Working 20+ hours weekly can become problematic, particularly for students in demanding majors. The key is finding balance—modest work hours help pay costs without derailing education quality.

Taking Action: Your Next Steps

Understanding that cash payment is possible represents the first step. Actually executing requires planning and action.

Start by calculating realistic college costs using net price calculators on college websites. Factor in all expenses—tuition, fees, room, board, books, transportation, and personal expenses. This provides the target number.

Next, inventory available resources: current savings, projected savings by college start, expected family income during college years, likely merit or need-based aid, and realistic student earnings. Be honest but optimistic.

The gap between costs and resources indicates how much work remains. That gap might close through additional scholarship applications, choosing more affordable schools, or adjusting expectations about campus living arrangements.

File the FAFSA early each year to maximize aid eligibility. Apply to multiple schools to compare aid packages. Cast a wide net on scholarship applications, treating it like a part-time job if necessary.

Conclusion

Yes, it’s absolutely possible to pay for college with cash rather than loans. Most families who achieve this success do so by combining multiple funding sources: grants, scholarships, savings, current income, student earnings, and smart payment strategies.

The path looks different for every family based on income, savings, student qualifications, and college choices. A family earning $200,000 annually faces different challenges than one earning $50,000, but both can minimize or eliminate debt with proper planning.

According to College Board, most full-time students at four-year colleges receive financial aid to help pay for college. The sticker price is usually higher than what families actually pay. Students and parents can save tax-free for college costs. And many payment options exist beyond simply taking loans.

The key is starting early, staying informed, and being strategic. Even families beginning this process late—when students are already in high school—can dramatically reduce costs through smart college selection, aggressive scholarship pursuit, and creative payment approaches.

Ready to create a debt-free college plan? Start by completing the FAFSA, running net price calculators for target schools, and exploring 529 plan options in your state. The sooner action begins, the more options remain available. College is expensive, but with the right approach, it’s manageable without mortgaging your future through excessive loans.