Quick Summary: Yes, getting a loan with bad credit is possible through various options including online lenders that consider alternative data, credit unions, secured loans, and government-backed programs. While borrowers with poor credit face higher interest rates and stricter terms, lenders like Upstart, OneMain Financial, and specialized bad credit lenders approve applicants with scores as low as 300 or no credit history at all.

Bad credit feels like a financial prison. One mistake, one medical bill, one unexpected layoff, and suddenly traditional banks won’t even look at your application.

But here’s the thing: more than 45 million American adults have no credit score because they have limited or no credit history, according to the Consumer Financial Protection Bureau. That’s roughly one in five adults. And millions more carry credit scores below 600.

So if lenders turned away everyone with imperfect credit, they’d be ignoring a massive portion of potential borrowers. That’s why the lending landscape has evolved significantly in recent years, with new players and innovative approaches making loans accessible even to those with seriously damaged credit.

What Actually Counts as Bad Credit?

Credit scores range from 300 to 850. Most scoring models consider anything below 580 as poor credit, while scores between 580 and 669 fall into the fair category.

If you’re sitting around 580 or below, traditional banks will likely decline your application. That’s just reality. But that doesn’t mean you’re out of options entirely.

The Consumer Financial Protection Bureau notes that credit scoring models look at how close you are to being maxed out on existing credit, your payment history, length of credit history, types of credit used, and recent credit inquiries. They recommend keeping credit utilization below 30 percent of your total limit.

Lenders That Actually Approve Bad Credit Applications

Several lenders specialize in working with borrowers who have less-than-perfect credit. These aren’t your traditional banks.

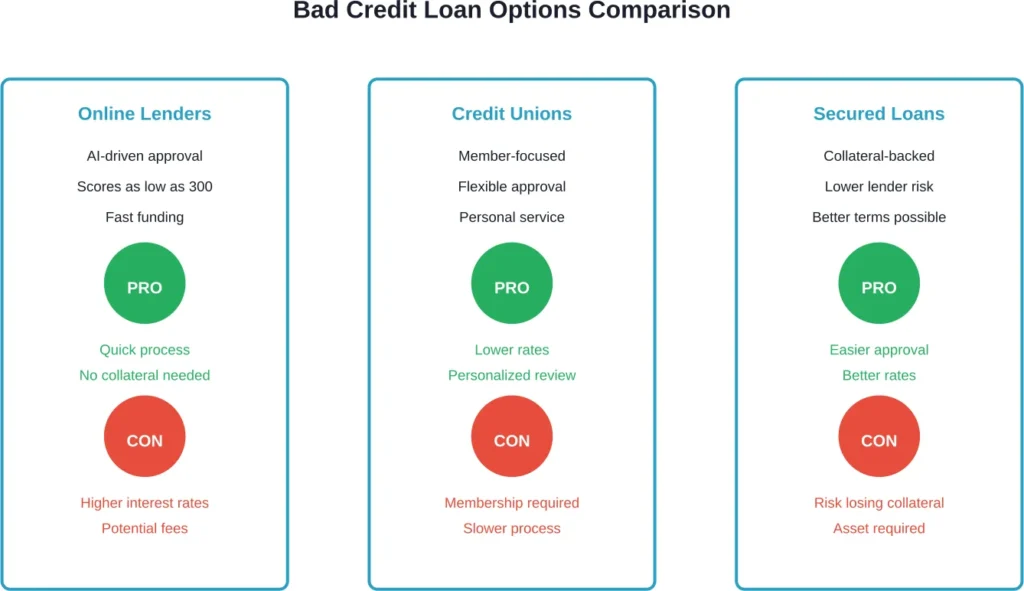

Online Lenders Using Alternative Data

Upstart stands out by approving borrowers with credit scores as low as 300, and they’ll even consider applicants with no credit history at all. The platform uses artificial intelligence to evaluate factors beyond credit scores, including education, employment history, and income stability.

Loan amounts range from $1,000 to $75,000, giving borrowers flexibility based on their needs. The application process happens entirely online, which speeds things up considerably compared to traditional bank applications.

Other online lenders like Avant require a minimum credit score of 580, while Universal Credit sets the bar at 560. Oportun specifically targets borrowers with no credit history, offering smaller loans designed for those just starting to build credit.

| Lender | Minimum Credit Score | Loan Amounts | Key Feature |

|---|---|---|---|

| Upstart | 300 (or no credit history) | $1,000 – $75,000 | AI-driven approval considering education and employment |

| Avant | 580 | Varies by state | Quick funding process |

| Universal Credit | 560 | Business focus available | Flexible terms for business needs |

| Oportun | No credit history accepted | Small loans | Designed for credit building |

| OneMain Financial | No stated minimum | $1,500 – $20,000 | Secured loan options available |

Credit Unions and Community Banks

Credit unions operate differently than traditional banks. They’re member-owned, which means they’re often more willing to work with borrowers who have credit challenges.

Florida Credit Union, for example, offers personal loans ranging from $3,001 to $50,000 even for borrowers with imperfect credit. They market specifically to people who “need money in a hurry” and whose “credit isn’t perfect.”

The advantage? Credit unions typically offer lower interest rates than online bad credit lenders. The disadvantage? You usually need to become a member first, which may require living in a specific area or working for certain employers.

Secured Loan Options

OneMain Financial specializes in secured loans, where you put up collateral like a vehicle to back the loan. This reduces the lender’s risk, which means they’re more willing to approve borrowers with poor credit.

Secured loans generally come with lower interest rates than unsecured bad credit loans. But the trade-off is obvious: if you can’t make payments, you lose whatever asset you put up as collateral.

What About Government-Backed Loans?

Government programs offer some of the most accessible lending options for people with credit challenges, particularly for home purchases.

The Department of Veterans Affairs operates a loan program for eligible veterans, active servicemembers, and surviving spouses. These loans are made by private lenders but guaranteed by the VA, which means lenders take on less risk and can offer more favorable terms.

According to the Consumer Financial Protection Bureau, special loan programs can be more affordable than conventional or FHA loans for those who qualify. They always recommend comparing official loan offers, called Loan Estimates, before making a final decision.

For home purchases specifically, the CFPB notes that as of March 2025, borrowers may be able to access up to 80 percent of their home’s value through home equity loans or lines of credit (according to the Federal Trade Commission), even with less-than-perfect credit.

The Reality of Bad Credit Loan Terms

Look, nobody’s going to pretend that bad credit loans come with great terms. They don’t.

Interest rates on bad credit loans typically run significantly higher than prime lending rates. Where someone with excellent credit might qualify for a personal loan at 6-8%, someone with a 580 credit score could be looking at rates of 20%, 30%, or even higher.

Federal Reserve research on subprime lending shows that delinquency rates increased significantly in recent years for borrowers with lower credit scores. During the pandemic, income support and forbearance programs led consumer loan delinquency rates to fall to near-record lows. But since the second half of 2021, delinquency rates have climbed, and by 2023:Q3, overall rates for auto and credit card loans had exceeded their pre-pandemic levels, particularly for subprime borrowers.

Monthly payments also increased substantially. For auto loans specifically, Federal Reserve data indicates that monthly payments rose nearly 30 percent between 2020 and 2023, driven by higher vehicle prices requiring households to borrow more.

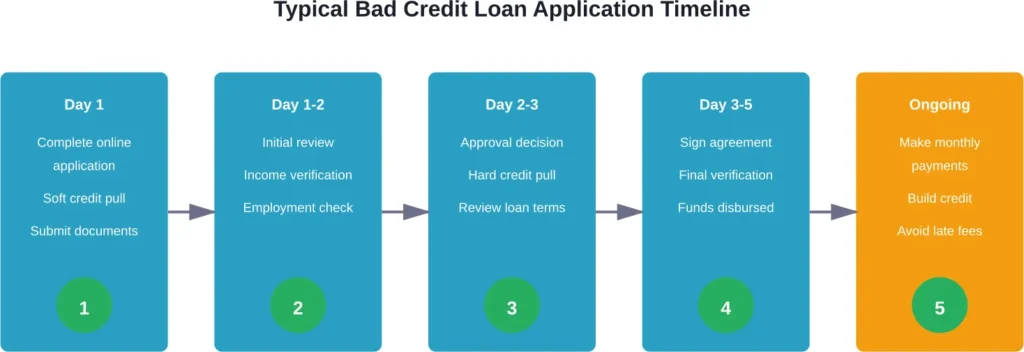

How the Application Process Actually Works

Most bad credit lenders perform what’s called a soft credit inquiry during the initial application stage. This doesn’t affect your credit score.

OppLoans, for example, performs a soft credit inquiry on your Experian credit report and a hard credit inquiry on your Clarity report, so applying won’t negatively impact your FICO score according to their documentation.

The application process typically involves:

- Providing personal information including Social Security number, address, and employment details

- Documenting income through pay stubs, tax returns, or bank statements

- Listing current debts and monthly obligations

- Choosing loan amount and preferred repayment term

- Reviewing and accepting loan terms if approved

Some lenders offer same-day funding if approved early in the day. Others take 2-5 business days to disburse funds.

Alternatives Worth Considering

Sometimes a traditional loan isn’t the best answer. Several alternatives exist that might work better depending on your situation.

Credit Counseling and Debt Management

The National Foundation for Credit Counseling operates a nonprofit network of certified credit counseling agencies. These organizations offer confidential financial counseling, often at low or no cost.

NFCC-certified counselors can help negotiate with creditors, stop collection calls, prevent additional late fees and interest charges, and potentially set up a debt management plan. According to their documentation, they’ve served over 35 million clients since 2006.

A debt management plan consolidates multiple credit card payments into one monthly payment, often with reduced interest rates negotiated by the counselor. This doesn’t technically require taking out a new loan.

Family Loans

The Consumer Financial Protection Bureau mentions getting help from family members or other trusted individuals as a legitimate option for situations like down payments. The same approach can work for other financial needs.

Family loans avoid credit checks entirely. But they come with their own risks, primarily the potential damage to relationships if repayment becomes difficult.

Red Flags and Predatory Lending

Bad credit makes borrowers vulnerable to predatory lending practices. Watch out for these warning signs:

- Lenders who guarantee approval regardless of credit

- Upfront fees before loan approval

- Pressure to apply immediately without time to review terms

- Requests to wire money or pay with gift cards

- APRs exceeding state legal limits

- Vague or confusing loan terms

The Equal Credit Opportunity Act prohibits discrimination based on race, color, religion, national origin, sex, marital status, age, or receipt of public assistance. Lenders must also provide applicants with specific reasons for credit denials.

The Fair Credit Reporting Act protects information collected by consumer reporting agencies. Borrowers have rights regarding how their credit information is used and shared.

Improving Approval Odds

Even with bad credit, certain steps can improve approval chances and potentially secure better terms.

First, check credit reports for errors. The CFPB notes that information in consumer reports cannot be provided to anyone who doesn’t have a legitimate business need. But mistakes happen, and disputing inaccurate negative items can boost scores quickly.

Second, consider a co-signer with better credit. This reduces lender risk substantially. The co-signer becomes equally responsible for the debt, which means their credit is on the line too.

Third, apply for the minimum amount needed. Smaller loan requests are easier to approve than larger ones, especially for borrowers with credit challenges.

Fourth, demonstrate stable income and employment. Lenders care deeply about ability to repay. Two years of steady employment in the same field carries significant weight.

| Strategy | Impact on Approval | Timeline |

|---|---|---|

| Dispute credit report errors | High – can boost score immediately | 30-45 days |

| Lower credit utilization below 30% | Medium – improves credit score | 1-2 billing cycles |

| Add qualified co-signer | Very High – major risk reduction | Immediate |

| Request smaller loan amount | Medium – easier to approve | Immediate |

| Document stable employment | Medium – proves repayment ability | Immediate |

| Offer collateral (secured loan) | High – reduces lender risk | Immediate |

Using Bad Credit Loans to Rebuild Credit

Here’s something counterintuitive: a bad credit loan, managed properly, can actually help repair damaged credit.

Payment history accounts for the largest portion of credit score calculations. Making consistent, on-time payments on a bad credit loan demonstrates creditworthiness to future lenders.

Research from Harvard Kennedy School found that credit reports influence not just lending decisions but increasingly employment decisions as well. Improving credit scores can therefore impact both financial and career opportunities.

The key is treating the loan as a credit-building tool, not just a source of emergency cash. Set up automatic payments to ensure nothing gets missed. Pay more than the minimum when possible to reduce interest costs and shorten the repayment timeline.

Frequently Asked Questions

Yes, some lenders approve borrowers with credit scores as low as 300. Upstart, for instance, considers applicants with scores of 300 or no credit history at all by evaluating alternative data like education and employment. However, expect significantly higher interest rates and potentially smaller loan amounts with scores below 500.

Most lenders perform a soft credit inquiry during the initial application, which doesn’t affect credit scores. But once approved and moving forward with the loan, a hard credit inquiry typically occurs. Some lenders like OppLoans structure their process to minimize FICO score impact by pulling from alternative credit bureaus.

Interest rates vary widely based on credit score, income, loan amount, and lender. Generally speaking, borrowers with scores around 580 might see rates between 20-36% APR from online lenders, while credit unions may offer slightly better terms. Secured loans typically come with lower rates than unsecured options.

Funding timelines depend on the lender and when approval occurs. Some online lenders offer same-day funding if approved early in the business day. Most disburse funds within 1-5 business days of final approval. Credit unions and traditional lenders typically take longer, sometimes 1-2 weeks.

The initial hard credit inquiry may cause a small, temporary score decrease of 5-10 points. However, making on-time payments helps rebuild credit over time. The bigger risk comes from missed payments, which can damage credit significantly. The Federal Reserve notes that delinquency rates have increased for subprime borrowers in recent years, so realistic budgeting before borrowing is crucial.

The Consumer Financial Protection Bureau provides extensive warnings about payday loans. While accessible to bad credit borrowers, payday loans typically carry extremely high costs and short repayment periods that can trap borrowers in debt cycles. Most financial counselors recommend exhausting all other options before considering payday lending.

According to the CFPB, more than 45 million American adults have limited or no credit history, yet homeownership remains possible through FHA loans, VA loans, and other special programs. These government-backed options offer more flexible credit requirements than conventional mortgages, though borrowers should expect higher interest rates and potentially larger down payment requirements.

Making the Right Decision

Bad credit doesn’t permanently close the door on borrowing. Multiple legitimate options exist, from AI-driven online lenders to community credit unions to government-backed programs.

But getting approved is only half the battle. The real challenge is managing the loan responsibly, making payments on time, and using the opportunity to rebuild credit rather than sink deeper into debt.

Before applying anywhere, calculate exactly how much borrowing costs over the full loan term. Compare multiple offers. Read the fine print about fees, prepayment penalties, and rate adjustment clauses.

And honestly assess whether borrowing is the right move. Sometimes the answer is saving longer, negotiating with creditors directly, or working with nonprofit credit counseling services instead of taking on new debt.

Bad credit makes borrowing harder and more expensive. That’s just reality. But it doesn’t make borrowing impossible, and for some situations, a carefully chosen bad credit loan serves as a bridge to better financial stability.

Check current rates from multiple lenders, read reviews from actual borrowers, and don’t let urgency push you into predatory lending arrangements. The options exist. Finding the right one just takes more research and realistic planning than it would with excellent credit.