Quick Summary: While payment bonds are typically issued alongside performance bonds in a single document, it is legally possible to obtain a payment bond independently. The feasibility depends on project requirements, whether the work is public or private, and the surety company’s underwriting policies—though most sureties and project owners prefer bundling both bonds for comprehensive protection.

The question of whether contractors can secure only a payment bond—without an accompanying performance bond—comes up frequently in construction circles. The short answer? Technically yes, but there’s nuance here worth understanding.

Payment bonds guarantee that subcontractors and suppliers get paid for their work and materials. Performance bonds guarantee the contractor completes the project according to contract terms. While these are distinct protections, they typically travel together for good reasons.

Understanding Payment Bonds as Standalone Instruments

Payment bonds function as three-party agreements between the contractor (principal), the project owner or higher-tier contractor (obligee), and the surety company providing the guarantee. According to surety bond experts, payment bonds protect projects from mechanic’s liens by ensuring suppliers and subcontractors receive compensation even if the contractor defaults financially.

Here’s the thing though—one document can serve as both a payment bond and performance bond simultaneously. The distinction comes down to wording in the bond document itself. Legal analysis shows that whether a single writing functions as one type or both depends entirely on its specific language.

But that doesn’t mean you can’t request just payment coverage. Private projects especially have flexibility here.

Legal Framework for Bond Requirements

The Federal Miller Act requires contractors to provide both payment and performance bonds for most federally funded construction contracts exceeding $150,000. This federal mandate sets the standard that many state and local jurisdictions follow.

Many state and municipal governments have adopted similar “Little Miller Act” statutes requiring both bond types for public works. These legal requirements make standalone payment bonds uncommon in government contracting.

Private projects operate under different rules. No federal law mandates bonds for privately funded construction, giving owners discretion to require payment bonds only, performance bonds only, both, or neither.

When Standalone Payment Bonds Make Sense

Several scenarios make standalone payment bonds attractive:

Supply-only contracts: When a company supplies materials without installation responsibilities, payment bond protection matters more than performance guarantees. The supplier’s main risk involves non-payment, not project completion.

Lower-risk private projects: Some private owners assess their contractor’s track record and decide completion risk is minimal but still want subcontractor payment protection. Payment bonds prevent mechanic’s liens that could cloud property titles.

Cost considerations: Though combined payment and performance bonds typically cost around 1.5-3% of the contract amount, requesting only payment coverage might reduce premiums slightly. For a $200,000 contract, a 3% premium would translate to approximately $6,000 in bond costs.

The Surety Perspective on Unbundled Bonds

Most surety companies prefer issuing payment and performance bonds together. Why? Risk assessment becomes cleaner when underwriters evaluate complete project protection.

According to the U.S. Small Business Administration’s Surety Bond Guarantee Program, sureties approved by the U.S. Treasury Department to issue surety bonds evaluate contractors based on comprehensive project risk. The SBA guarantees 90% of a surety’s losses on contracts up to $100,000, and 80% on larger contracts, if a small business defaults, making thorough risk evaluation critical.

When contractors request only payment bonds, sureties question what completion risks they’re not seeing. This can complicate underwriting and potentially increase premiums rather than decrease them.

Sound familiar? The surety needs confidence in the contractor’s ability to complete work—not just pay bills. Separating these guarantees creates underwriting complications many sureties would rather avoid.

Practical Challenges with Standalone Requests

Contractors attempting to secure only payment bonds often encounter resistance because sureties view project completion and payment capacity as interconnected risks. Financial capacity supporting payment obligations often correlates with operational capacity ensuring completion.

Some surety agents report that standalone payment bond requests trigger additional scrutiny during the application process, potentially extending approval timelines.

Cost Implications and Premium Calculations

Payment bond costs depend on the contractor’s financial standing, project size, and risk factors. While combined payment and performance bonds typically cost around 1.5-3% of the contract amount for applicants with sound financials, isolating just payment coverage doesn’t necessarily halve that premium.

The penal sum—the bond’s maximum payout amount—for payment bonds usually equals 100% of the contract value. For performance bonds, the same applies. Bid bonds, another surety bond type, typically carry penal sums of 10% of the bid amount (though some Tennessee statutes require 10% for certain construction manager services).

| Bond Type | Typical Penal Sum | When Required | Premium Range |

|---|---|---|---|

| Bid Bond | 10% of bid amount | Competitive bidding | Minimal to no cost |

| Payment Bond | 100% of contract value | Public projects over $150K | 1.5-3% of contract |

| Performance Bond | 100% of contract value | Public projects over $150K | 1.5-3% of contract |

| Combined Payment/Performance | 100% of contract value | Most public contracts | 1.5-3% of contract total |

For contracts valued at $500,000 or less, the SBA’s Quick Bond Guarantee program streamlines approval for Prior Approval sureties, making bond acquisition faster regardless of configuration.

Public vs Private Project Requirements

The divide between public and private projects creates vastly different bonding landscapes.

Public projects: Federal contracts require both bond types under the Miller Act. State and municipal contracts follow similar patterns with their respective Little Miller Acts. Getting only a payment bond on public work remains essentially impossible due to statutory requirements.

Private projects: No legal mandate exists for bonds on privately funded construction. Payment bonds are becoming more common on private work specifically because owners want lien protection without necessarily requiring performance guarantees.

This trend reflects growing owner sophistication. They recognize that payment bonds protect their property from mechanic’s liens filed by unpaid subcontractors or suppliers—a real financial and legal headache.

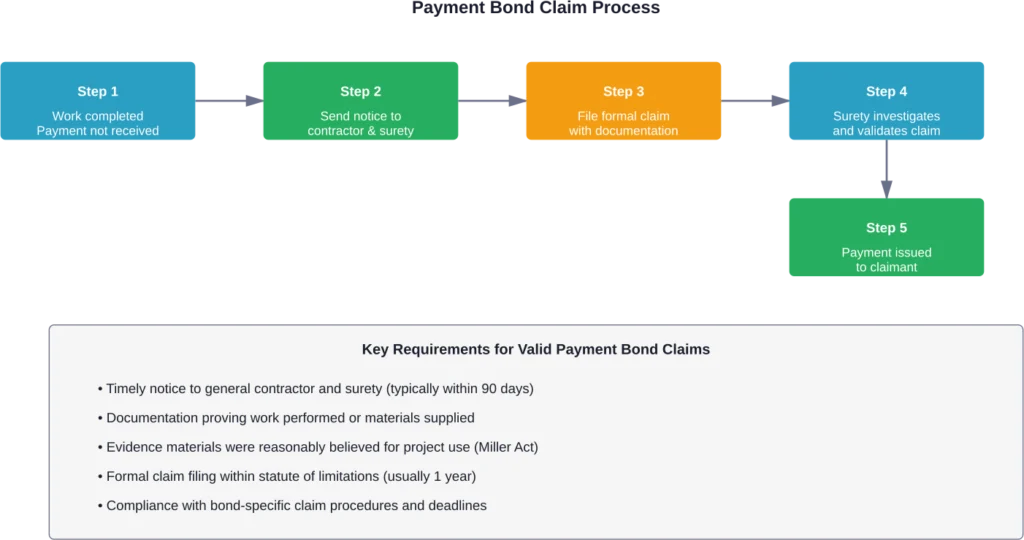

How Payment Bond Claims Work

Understanding the claims process reveals why standalone payment bonds can function effectively when structured properly.

Unpaid subcontractors or suppliers must follow specific procedures to file payment bond claims. Under the Miller Act, claimants must demonstrate that materials were “reasonably believed” to be used in the project to gain protection. Courts have ruled favorably for suppliers meeting this standard.

Payment bond coverage extends beyond just labor and materials to include equipment rentals, fuel costs, and other project necessities in many cases. The bond’s protection proves comprehensive for payment-related disputes even without performance coverage.

Strategies for Obtaining Standalone Payment Bonds

Contractors determined to secure only payment bonds should approach the process strategically.

Start with private projects: Focus efforts on privately funded work where legal flexibility exists. Public contracts won’t budge on dual bond requirements.

Build surety relationships: Established contractors with strong surety relationships have better negotiating positions. Long-term partnerships create flexibility that new relationships lack.

Present compelling rationale: Explain clearly why performance bonding doesn’t apply—perhaps it’s a supply-only contract or the owner specifically requested payment protection alone.

Consider owner requirements first: Even if sureties would issue standalone payment bonds, owners often want comprehensive protection. Understanding owner priorities prevents wasted effort.

Frequently Asked Questions

No. The Miller Act requires both payment and performance bonds for federal construction contracts exceeding $150,000. This federal law mandates dual bond coverage with no exceptions for standalone payment bonds on government work.

Not always. While one document can function as both a payment bond and performance bond depending on its wording, sureties can issue separate documents for each bond type. The legal effect depends on the specific language used in the bond agreement.

Not necessarily. While combined payment and performance bonds typically cost around 1.5-3% of the contract amount, requesting only payment coverage may not significantly reduce premiums. Sureties often view separated bonds as creating additional underwriting complexity, which can maintain or increase costs.

Private owners sometimes require only payment bonds when they’re confident in the contractor’s ability to complete work but want protection against mechanic’s liens. Payment bonds prevent unpaid subcontractors and suppliers from filing liens against the property, protecting the owner’s title.

Mechanic’s liens are legal claims filed against property by unpaid contractors, subcontractors, or suppliers. Payment bonds prevent the need for mechanic’s liens by guaranteeing payment through the surety. When payment bonds exist, lien rights are typically replaced by bond claim rights.

For contracts valued at $500,000 or less, the SBA’s Quick Bond Guarantee program enables rapid approval through Prior Approval sureties. Larger contracts or standalone requests may face extended underwriting timelines as sureties evaluate the unusual bonding structure more carefully.

Subcontractors, suppliers, laborers, and material providers who weren’t paid for work or materials provided to the bonded project can file payment bond claims. The Miller Act extends this protection to anyone who can demonstrate materials were reasonably believed to be used in the project.

Making the Right Bonding Decision

So is it possible to get only a payment bond? Absolutely—particularly for private construction projects where legal mandates don’t apply.

But possible doesn’t always mean practical. Most sureties prefer issuing comprehensive protection through combined payment and performance bonds. Project owners often want that complete coverage too. The premium savings from unbundling bonds may prove minimal or nonexistent.

For contractors working on private projects with specific circumstances—supply contracts, owner preferences, or unique risk profiles—standalone payment bonds represent viable options worth discussing with surety partners.

Ready to explore bonding options for your next project? Contact a licensed surety agent to discuss whether standalone payment bonds or combined coverage best fits your situation. Professional guidance navigates the complexities of bond requirements, surety preferences, and project-specific needs to secure optimal protection at competitive rates.