Quick Summary: Getting two title loans is possible but depends on state regulations, lender policies, and your vehicle equity. You can’t have two title loans on the same car simultaneously in most cases, but you can get separate title loans on two different vehicles. Second lien title loans exist in some states but come with higher costs and stricter requirements.

Financial emergencies don’t always arrive one at a time. When unexpected expenses pile up and one title loan isn’t covering everything, borrowers naturally wonder whether they can take out another.

The answer isn’t straightforward. It depends on what type of multiple title loans we’re talking about—two loans on the same car, or separate loans on different vehicles.

Here’s what the regulations and lending practices actually allow.

Understanding How Title Loans Work

Title loans use a vehicle’s title as collateral for a short-term loan. The lender places a lien on the vehicle title, which means they have a legal claim to the vehicle if the borrower defaults.

According to the Consumer Financial Protection Bureau, vehicle title loans fall under regulations governing payday loans and certain high-cost installment loans. These regulations require lenders to make reasonable determinations about a borrower’s ability to repay.

Most title loans range from 25% to 50% of the vehicle’s value. According to competitor content citing Kelley Blue Book, the average used car price in 2024 reached roughly $26,500, which means many borrowers could have thousands of dollars in available equity.

But here’s the thing—having equity doesn’t automatically mean lenders will approve multiple loans.

Can You Get Two Title Loans on the Same Car?

This is where things get complicated. Community discussions reveal confusion around this exact scenario, with some borrowers reporting two loans on the same vehicle through different lenders.

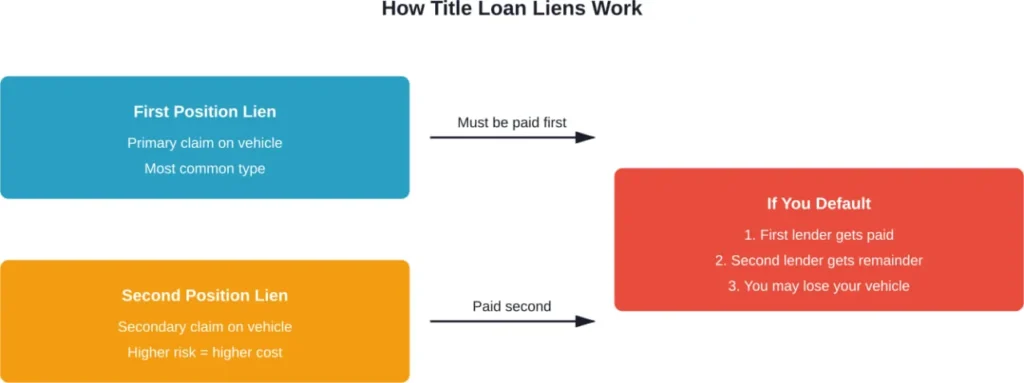

Technically, most states don’t allow two separate title loans on the same vehicle simultaneously. The reason? A vehicle typically can’t have two first-position liens at once.

The first lender holds the primary lien. Until that’s cleared, another lender won’t typically issue a separate first-position loan on that same title.

What Are Second Lien Title Loans?

Second lien title loans do exist in some markets. These loans take a secondary position behind the existing lienholder.

If the borrower defaults, the first lienholder gets paid before the second. Because of this increased risk, second lien title loans typically come with:

- Higher interest rates than first-position loans

- Lower loan amounts relative to vehicle equity

- Stricter approval requirements

- Limited availability depending on state regulations

Not all states permit second lien title loans. California, for instance, has specific regulations around car title loans and truck title loans that limit these arrangements.

Can You Have Two Title Loans on Two Different Cars?

Now this is more straightforward. Yes, borrowers can get separate title loans on different vehicles they own.

If someone owns two cars with clear titles (or one clear title and one with sufficient equity), many lenders will approve separate loans on each vehicle.

Each loan is secured by its own vehicle. The lender evaluates each application based on that specific vehicle’s value and the borrower’s ability to repay.

That said, lenders still consider overall debt-to-income ratios. Multiple title loans increase financial obligations, which could affect approval for the second loan.

State Regulations on Multiple Title Loans

State laws vary significantly. Some states have strict caps on the number of title loans a borrower can have simultaneously.

The Federal Trade Commission has taken enforcement action against car title lenders for deceptive practices, highlighting the importance of understanding state-specific regulations before applying.

| Consideration | First Title Loan | Second Title Loan (Same Car) | Second Title Loan (Different Car) |

|---|---|---|---|

| Approval Difficulty | Moderate | Very Difficult | Moderate to Difficult |

| Interest Rates | High | Very High | High |

| State Availability | Most States | Limited States | Most States |

| Risk Level | High | Extremely High | Very High |

The Risks of Multiple Title Loans

Before pursuing two title loans, understand the serious financial risks involved.

Research from the University of New Mexico showed that from 2007 to 2009, 18.9 percent of bankruptcy debtors in New Mexico reported using payday loans—a finding specific to that state and time period. The study noted that usage of multiple payday loans at one time also increased drastically.

While this data focuses on payday loans, title loans carry similar high-cost characteristics that can trap borrowers in debt cycles.

Key Risk Factors

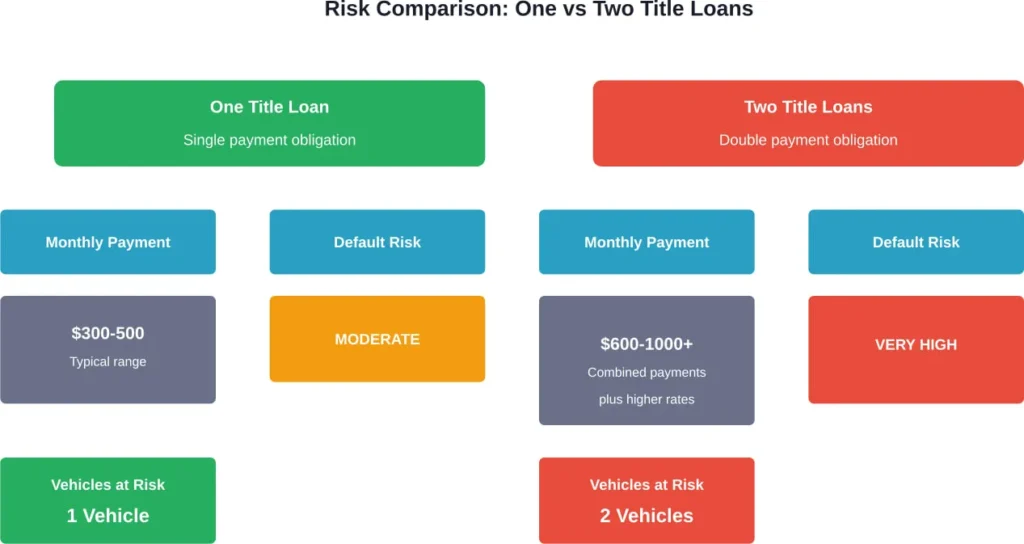

Multiple title loans compound financial pressure. Borrowers face:

- Double the monthly payments

- Higher total interest costs

- Increased risk of defaulting on both loans

- Potential loss of multiple vehicles

The Consumer Financial Protection Bureau requires lenders to make reasonable determinations about repayment ability, but borrowers should conduct their own honest assessment.

Safer Alternatives to Multiple Title Loans

Before taking out a second title loan, consider these alternatives:

Refinance the existing title loan. Some lenders offer refinancing options that could increase the loan amount based on current vehicle equity and payment history.

Personal installment loans. While they may require better credit, these typically come with lower interest rates and longer repayment terms.

Credit union loans. Many credit unions offer small-dollar loan programs specifically designed as alternatives to high-cost title loans.

Payment plans with creditors. Directly negotiating with medical providers, utility companies, or other creditors often yields better terms than borrowing at high interest rates.

Community assistance programs. Local nonprofits, churches, and government programs may provide emergency financial assistance for specific needs.

How to Borrow Responsibly If You Proceed

If alternatives don’t work and multiple title loans seem necessary, take these precautions:

Calculate total costs. Add up all fees, interest charges, and monthly payments across both loans. Can the budget genuinely support these payments?

Check state regulations. Verify whether the state permits multiple title loans and what protections exist for borrowers.

Read all documentation carefully. The Truth in Lending Act requires creditors to make certain written disclosures concerning finance charges. Review these thoroughly.

Have a clear repayment plan. Know exactly where the money will come from each month to make both payments on time.

Frequently Asked Questions

Most lenders won’t issue two separate title loans to the same borrower simultaneously, even on different vehicles. Lender policies typically limit borrowers to one active title loan at a time per company.

Defaulting on multiple title loans could result in losing all vehicles used as collateral. Lenders can repossess the vehicles, sell them, and pursue borrowers for any remaining balance after the sale.

Many lenders check credit reports and vehicle title records, which would reveal existing liens. However, reporting practices vary, and some lenders may not catch existing loans, especially with smaller companies.

Yes, refinancing an existing title loan often makes more sense than taking a second loan. Lenders may increase the loan amount based on remaining equity and payment history, typically at better terms than a second lien loan.

Absolutely. Some states heavily regulate or even prohibit title loans entirely, while others have minimal restrictions. Interest rate caps, loan term limits, and rollover provisions vary significantly by state.

For a second lien title loan, borrowers typically need substantial equity beyond what the first loan covers. Lenders want assurance their loan is secure even in the secondary position, so they may require 50% or more remaining equity.

This depends entirely on state law and lender policies. Some states explicitly limit borrowers to one title loan at a time, while others allow multiple loans on different vehicles but prohibit multiple loans on the same vehicle.

Making the Right Decision

Getting two title loans is technically possible in specific circumstances—either through second lien arrangements on one vehicle or separate loans on multiple vehicles.

But possible doesn’t mean advisable. The financial risks multiply quickly when juggling multiple high-cost loans.

Research from academic institutions shows strong correlations between high-cost short-term loans and financial distress. The data on payday loan users filing bankruptcy at rates nearly double the general population suggests these debt structures can accelerate rather than solve financial problems.

Before pursuing multiple title loans, exhaust safer alternatives. Check state laws, understand total costs, and honestly assess repayment capability.

Need help evaluating whether a title loan makes sense for your situation? Consult a nonprofit credit counselor who can review all options without a financial stake in the lending decision. Many offer free consultations and can identify resources you might not know exist.