Quick Summary: Not paying taxes triggers a series of escalating consequences. The IRS imposes penalties starting at 0.5% monthly (up to 25%) plus interest on unpaid amounts. If you continue to ignore notices, the IRS can garnish wages, levy bank accounts, place liens on property, and in severe cases, pursue criminal prosecution.

Tax season wraps up, and suddenly there’s a problem. Maybe the numbers didn’t add up the way they should have. Maybe an unexpected bill landed, and now there’s no money left to pay what’s owed to the IRS.

Here’s the thing though—ignoring a tax bill doesn’t make it disappear. According to the IRS, April 15 is the deadline for most people to file their individual income tax returns and pay any tax owed. Miss that deadline or fail to pay, and the consequences start accumulating immediately.

The question isn’t whether something will happen. The question is what happens, how quickly it escalates, and what options exist to stop the bleeding.

The Immediate Consequences: Penalties and Interest Start Immediately

The moment a tax payment is late, two things happen simultaneously: penalties start accruing and interest begins compounding.

Failure to Pay Penalty

The IRS applies a failure to pay penalty when taxes remain unpaid after the due date. According to IRS data, this penalty equals 0.5% of the unpaid taxes for each month or part of a month the tax remains unpaid. The penalty won’t exceed 25% of the total unpaid taxes.

That might sound small. But it adds up fast.

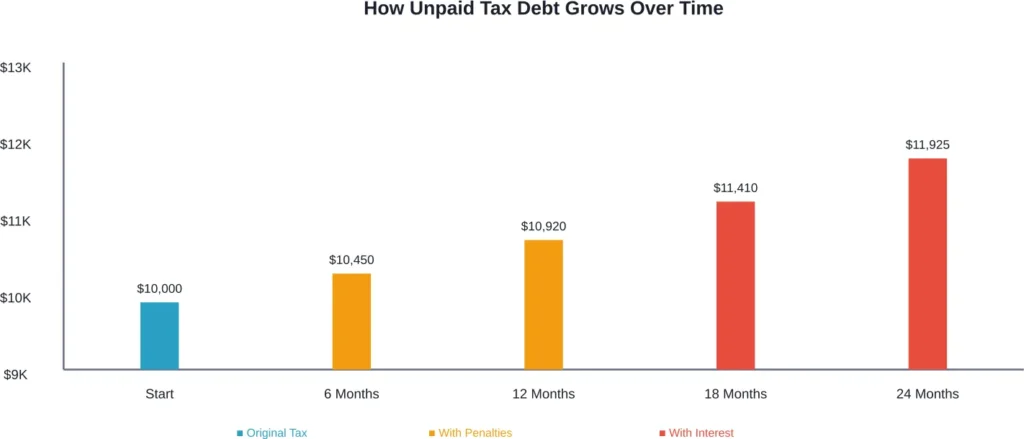

On a $10,000 tax bill, that’s $50 the first month. Then another $50. Then another. Over two years, that’s $1,200 in penalties alone—before considering interest.

Interest Charges That Never Stop

Interest accrues on any unpaid tax from the due date of the return until the payment date in full. The IRS sets this rate quarterly based on the federal short-term rate plus 3%.

Unlike penalties that cap at 25%, interest compounds continuously. There’s no maximum. It keeps accumulating until every dollar is paid.

The IRS also charges interest on penalties if they aren’t paid in full. That’s interest on interest—a double compounding effect that accelerates debt growth.

What the IRS Does Next: Collection Actions Escalate

The IRS doesn’t immediately seize assets. The agency follows a predictable escalation pattern, starting with notices and building toward enforcement actions.

Notice and Billing Phase

When processing is complete, if any tax, penalty, or interest is owed, the IRS sends a bill. These notices explain the amount owed and provide payment instructions.

The first notice is just that—a notice. Not a threat. Just information.

But ignore it, and more notices follow. Each one becomes more insistent. The language shifts from informational to urgent.

Federal Tax Liens

After repeated non-payment, the IRS can file a Notice of Federal Tax Lien. This is a public record that alerts creditors the government has a legal claim to property.

A tax lien doesn’t mean the IRS immediately takes property. It means the IRS has established first claim on assets—ahead of other creditors. This devastates credit scores and makes securing loans nearly impossible.

Levies: When the IRS Takes Assets

A levy is different from a lien. A levy means the IRS actually seizes assets.

Bank account levies freeze accounts and transfer balances to the IRS. Wage garnishment redirects a portion of each paycheck directly to the government. The IRS can also seize and sell property, vehicles, and other assets.

According to the Government Accountability Office, IRS enforcement actions help recover billions in unpaid taxes annually. The IRS has matching systems that compare income reported by employers against what taxpayers report, catching discrepancies before refunds are issued—saving about $65 million.

Criminal Consequences: When Does Tax Evasion Become a Crime?

Most people who don’t pay taxes face civil penalties, not criminal charges. But there’s a line.

The difference between owing taxes and committing tax evasion comes down to intent and action.

What Triggers Criminal Investigation

Simply not having money to pay taxes isn’t a crime. Filing a return that shows taxes owed, even if payment doesn’t follow, isn’t criminal.

Criminal cases involve deliberate evasion: hiding income, falsifying records, using fake documents, or creating elaborate schemes to avoid detection.

Real talk: the threshold is high. In February 2026, a prominent appellate attorney was convicted of tax evasion for hiding millions in gambling income and diverting legal fees to personal accounts to satisfy poker debts. That’s the level of deliberate deception that triggers criminal prosecution.

Another case from May 2025 involved an attorney charged with tax crimes for lying to a tax preparer, concealing approximately $1 million in income by falsely claiming to be a general manager rather than CEO and hiding bonuses and company-paid expenses.

These aren’t accidental mistakes. These are intentional schemes.

Potential Criminal Penalties

Tax evasion is a felony. Convictions can result in substantial fines and prison time. The Justice Department actively prosecutes cases involving significant amounts or egregious conduct.

For ordinary taxpayers who simply can’t afford to pay, criminal prosecution is extremely rare. The IRS focuses on collection, not incarceration, for civil tax debts.

| Violation Type | Civil vs. Criminal | Typical Consequence |

|---|---|---|

| Late payment of known tax | Civil | Penalties and interest |

| Failure to file return | Civil (usually) | Failure to file penalty (5% monthly, up to 25%) |

| Underreporting income accidentally | Civil | Accuracy-related penalties |

| Hiding income intentionally | Criminal | Fines and potential imprisonment |

| Creating false documents | Criminal | Felony charges, prosecution |

Payment Options When Money Is Tight

Here’s where it gets practical. Not having the full amount doesn’t mean there are no options.

The IRS offers several programs specifically designed for taxpayers who can’t pay immediately.

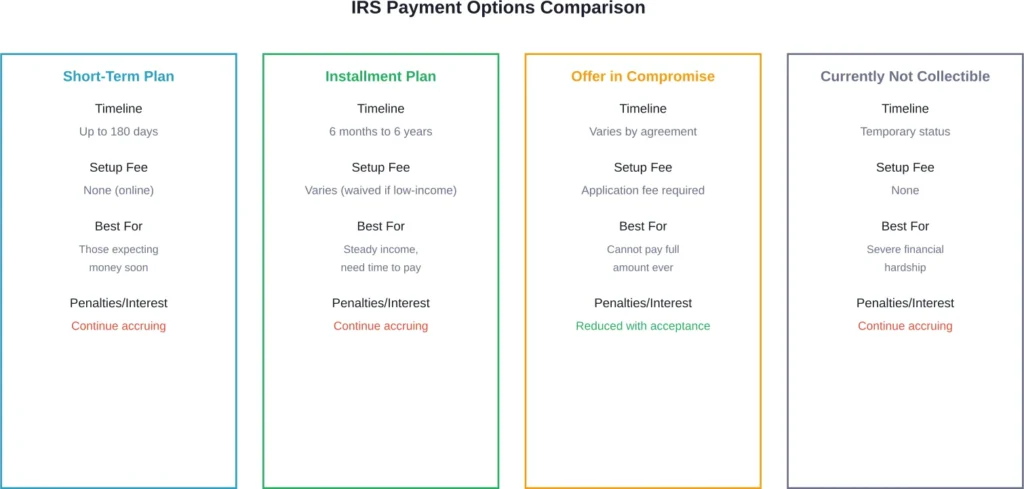

Short-Term Payment Plans

For those who can pay within 180 days, the IRS offers short-term payment plans. There’s no setup fee for online applications, though penalties and interest continue accruing until the balance is paid.

Installment Agreements

Installment agreements allow taxpayers to pay over time—sometimes several years. Monthly payments spread the burden into manageable chunks.

The IRS provides an online payment agreement application for qualifying taxpayers. This is faster than filing Form 9465 on paper and provides immediate confirmation.

Setup fees apply, but they’re reduced for direct debit payments and can be waived for low-income taxpayers.

Offer in Compromise

An Offer in Compromise allows taxpayers to settle tax debt for less than the full amount owed. The IRS accepts these offers when the reduced amount represents the most the agency can reasonably expect to collect.

Sound too good to be true? It’s not easy to qualify. The IRS evaluates ability to pay, income, expenses, and asset equity. Only taxpayers who genuinely can’t pay the full amount—even over time—qualify.

Currently Not Collectible Status

For taxpayers facing genuine financial hardship, the IRS can temporarily classify the account as Currently Not Collectible. This pauses collection actions.

But debt doesn’t disappear. Interest and penalties continue accruing. The IRS periodically reviews financial situations, and collection resumes when circumstances improve.

The Difference Between Not Filing and Not Paying

These are two separate issues with different penalties.

Not paying taxes means filing a return that shows taxes owed, but not sending payment. The failure to pay penalty applies—0.5% monthly, capped at 25%.

Not filing means never submitting a return at all. According to the IRS, the failure to file penalty is much steeper: 5% of the tax owed for each month or part of a month the return is late, up to a maximum of 25%.

If a return is more than 60 days late, there’s a minimum penalty.

When both penalties apply simultaneously, the failure to file penalty is reduced by the failure to pay penalty amount. But even with this offset, the combined penalty is significantly higher than just paying late.

The lesson? Always file, even when payment isn’t possible. Filing on time while explaining inability to pay results in far lower penalties than disappearing entirely.

How to Prevent Tax Problems Before They Start

Prevention beats damage control.

Adjust Withholding

Many tax bills result from insufficient withholding throughout the year. Adjusting W-4 forms with employers ensures enough tax is withheld from each paycheck, preventing surprise bills at filing time.

Make Estimated Tax Payments

Self-employed individuals, freelancers, and those with income not subject to withholding should make quarterly estimated tax payments. This spreads the burden across the year rather than creating a massive April liability.

File Extensions When Needed

Filing an extension provides an additional six months to submit a return. But here’s the catch: an extension to file is not an extension to pay. Taxes are still due by the original deadline. Extensions prevent failure to file penalties, but they don’t stop failure to pay penalties.

Seek Professional Help Early

When tax situations become complicated, professional help pays for itself. Tax professionals, enrolled agents, and CPAs understand IRS procedures and can negotiate on behalf of taxpayers.

Waiting until collection actions start makes everything harder. Early intervention opens more options.

State Taxes Add Another Layer

Everything discussed so far focuses on federal taxes. But most states have their own income taxes with separate penalties, interest rates, and collection procedures.

State tax agencies can be even more aggressive than the IRS. Some states suspend professional licenses, driver’s licenses, or business permits for unpaid taxes.

Addressing federal tax debt while ignoring state obligations is incomplete. Both must be handled.

What Community Discussions Reveal

Community discussions on platforms like Reddit show common patterns among people dealing with unpaid taxes.

Community members express concerns about contacting the IRS. Others share experiences with installment agreements. Some note that setting up payment plans involves ongoing penalty and interest accrual.

Frequently Asked Questions

The IRS begins charging a failure to pay penalty of 0.5% monthly on unpaid amounts, plus interest that compounds continuously. File the return on time even without payment to avoid the much steeper failure to file penalty. Then contact the IRS to set up a payment plan or explore other options.

Penalties and interest start immediately after the deadline. After several months of unpaid bills and ignored notices, the IRS can file a tax lien (typically after 10 days of a final notice). Levies on bank accounts or wages generally don’t happen until significant time has passed and multiple notices have been ignored, but the timeline varies by case.

Criminal prosecution for tax crimes is rare and reserved for cases involving deliberate evasion, fraud, or hiding income. Simply being unable to afford taxes is not a crime. The IRS pursues civil collection actions—penalties, liens, levies—not criminal charges for ordinary unpaid tax debts.

The IRS can place a lien on property, including houses, which establishes a legal claim. Actually seizing and selling a home is possible but extremely rare, typically reserved for cases involving substantial debt and complete non-cooperation. The IRS generally prefers payment arrangements to property seizure.

The IRS generally has 10 years from the date of assessment to collect tax debt. This is called the Collection Statute Expiration Date. After 10 years, the debt may expire if not collected. However, certain actions—like filing for an installment agreement or offer in compromise—can extend this period.

It depends on financial circumstances. Those who can pay within 180 days should use a short-term payment plan with no setup fee. For longer timelines, an installment agreement spreads payments over years. If truly unable to pay even over time, an Offer in Compromise might settle for less. Currently Not Collectible status is available for genuine hardship cases.

Absolutely. The failure to file penalty is 10 times higher than the failure to pay penalty (5% monthly versus 0.5% monthly). Filing the return shows good faith and dramatically reduces penalties. Then work with the IRS on payment arrangements.

Taking Action: Next Steps

The worst response to a tax bill is inaction.

Ignoring notices doesn’t make debt disappear. It makes debt grow. Penalties compound. Interest accumulates. Collection actions escalate.

The IRS is not unreachable. The agency offers multiple payment options specifically designed for people who can’t pay immediately. But these options require proactive communication.

File returns on time, even without payment. Contact the IRS as soon as a problem becomes apparent. Explore installment agreements, offers in compromise, or hardship status based on individual circumstances.

Professional help from tax attorneys, CPAs, or enrolled agents can navigate complex situations and negotiate with the IRS on behalf of taxpayers.

The key is movement. Action beats paralysis. Address the problem before it becomes a crisis, and more options remain available. Wait too long, and the IRS makes decisions without input.

Tax debt feels overwhelming. But it’s solvable. The first step is understanding what happens—and then taking action to prevent the worst consequences.