Quick Summary: If you owe the IRS more than $25,000, you face serious consequences including federal tax liens, wage garnishment, bank levies, and asset seizures. However, the IRS offers multiple resolution options: streamlined installment agreements (up to 72 months for debts under $50,000), non-streamlined payment plans requiring financial disclosure, Offers in Compromise, and Currently Not Collectible status for those facing financial hardship.

Discovering you owe the IRS a substantial sum can trigger immediate panic. When that number crosses the $25,000 threshold, the stakes get considerably higher.

But here’s the thing: while the IRS has powerful collection tools at its disposal, the agency also recognizes that crushing taxpayers into financial ruin serves nobody’s interests. The tax code includes multiple pathways for resolving significant tax debts, even when the amount seems overwhelming.

The $25,000 mark matters because it triggers different IRS procedures and changes which payment options remain available. Understanding what happens at this threshold and knowing your options can mean the difference between financial recovery and devastating consequences.

Why the $25,000 Threshold Changes Everything

The IRS treats tax debts differently based on the total amount owed. According to the IRS, taxpayers who owe $25,000 or less can typically qualify for streamlined payment arrangements that require minimal paperwork and no detailed financial disclosure.

Cross that line, and the rules shift.

For debts exceeding $25,000, the IRS may require a Collection Information Statement (Form 433-F or 433-A), which demands comprehensive details about your income, assets, expenses, and overall financial condition. This additional scrutiny isn’t arbitrary—it determines what collection actions the IRS might take and which resolution options remain available.

The $25,000 threshold also affects federal tax lien withdrawals. According to IRS guidelines, qualifying taxpayers who owe $25,000 or less may request withdrawal of a Notice of Federal Tax Lien under certain conditions, including entering a Direct Debit Installment Agreement. Those who owe more than $25,000 must first pay down the balance to $25,000 before requesting withdrawal.

Immediate Consequences of Owing More Than $25,000

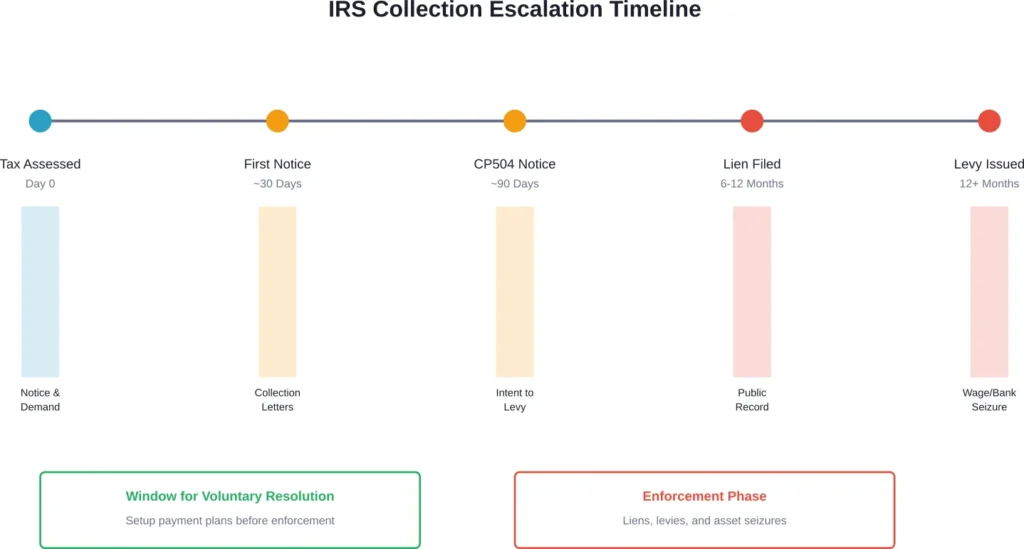

When your tax debt exceeds $25,000 and remains unpaid, the IRS escalates its collection activities. These aren’t scare tactics—they’re legal actions the agency regularly employs.

Federal Tax Liens

A federal tax lien represents the government’s legal claim against your property. According to the IRS, a lien arises automatically when the agency assesses your liability, sends a Notice and Demand for Payment, and you neglect or refuse to pay the debt in time.

The IRS files a public Notice of Federal Tax Lien, which:

- Attaches to all your current and future property, including real estate, vehicles, and financial assets

- Appears on your credit reports, severely damaging your credit score

- Makes selling or refinancing property extremely difficult

- Gives the IRS priority over other creditors in bankruptcy proceedings

- Remains public record, visible to employers, lenders, and business partners

While the IRS doesn’t automatically file liens for every debt over $25,000, larger balances increase the likelihood dramatically. The agency generally files liens when the debt reaches $10,000 or more and collection efforts have stalled.

Wage Garnishment and Bank Levies

A levy differs from a lien. According to IRS definitions, a levy is the actual legal seizure of property to satisfy tax debt, whereas a lien is merely a claim against property.

The IRS can levy:

- Wages and salary—continuous garnishment until the debt is paid

- Bank accounts—one-time seizure of available funds

- Social Security benefits—up to 15% of each payment

- Retirement accounts—subject to applicable taxes and penalties

- Business income and accounts receivable

- Rental income from investment properties

Before issuing a levy, the IRS must send a CP504 notice, which serves as the Notice of Intent to Levy under Internal Revenue Code section 6331(d). This gives taxpayers a final opportunity to address the debt before enforcement actions begin.

Asset Seizure

For substantial debts, the IRS can seize and sell physical assets including vehicles, real estate, and business equipment. While less common than levies, asset seizures happen regularly for significant unpaid tax debts.

The Collection Statute Expiration Date (CSED) creates urgency for the IRS. According to the agency, the IRS generally has 10 years from the date of assessment to collect tax debt. As this deadline approaches, collection actions often intensify.

Passport Restrictions

For tax debts exceeding $50,000, the IRS can certify the debt to the State Department, which may revoke or deny passport renewal. This threshold includes tax, penalties, and interest combined.

Payment Plan Options for Debts Over $25,000

Despite these serious consequences, the IRS offers legitimate pathways to resolve tax debts exceeding $25,000. The key lies in taking action before enforcement escalates.

Streamlined Installment Agreements (Under $50,000)

According to IRS payment plan guidelines (updated March 3, 2026), taxpayers who owe between $25,000 and $50,000 in combined tax, penalties, and interest can qualify for streamlined installment agreements without providing detailed financial information.

These agreements allow monthly payments over up to 72 months. The monthly payment must be sufficient to pay the full balance before the Collection Statute Expiration Date.

Requirements include:

- All required tax returns must be filed

- Total debt must be under $50,000

- Direct debit payment method strongly encouraged

- No defaults on previous installment agreements

Setup fees apply. As of March 3, 2026, applying online through your IRS online account costs significantly less than applying by phone, mail, or in person. Low-income taxpayers may qualify for fee waivers or reimbursements.

Non-Streamlined Installment Agreements (Over $50,000)

For debts exceeding $50,000, the IRS requires a Collection Information Statement detailing income, expenses, assets, and liabilities. The agency analyzes this information to determine payment capacity.

These agreements may require:

- Form 433-F (individuals) or 433-A (self-employed individuals)

- Documentation of income and expenses

- Financial statements for businesses

- Regular reviews of financial condition

Payment terms depend on demonstrated ability to pay. In some cases, the IRS accepts partial payment agreements where monthly payments don’t cover the full balance before the CSED expires.

Short-Term Payment Plans

According to IRS Topic No. 201, individual taxpayers who owe less than $100,000 in combined tax, penalties, and interest can request a short-term payment plan of up to 180 days. This option carries no setup fee and provides additional time to pay in full.

| Payment Plan Type | Debt Amount | Duration | Financial Disclosure |

|---|---|---|---|

| Short-term | Under $100,000 | Up to 180 days | Not required |

| Streamlined | $25,000-$50,000 | Up to 72 months | Not required |

| Non-streamlined | Over $50,000 | Varies | Required (Form 433-F/433-A) |

Alternative Resolution Options

Payment plans aren’t the only solution. Depending on financial circumstances, other options may provide better outcomes.

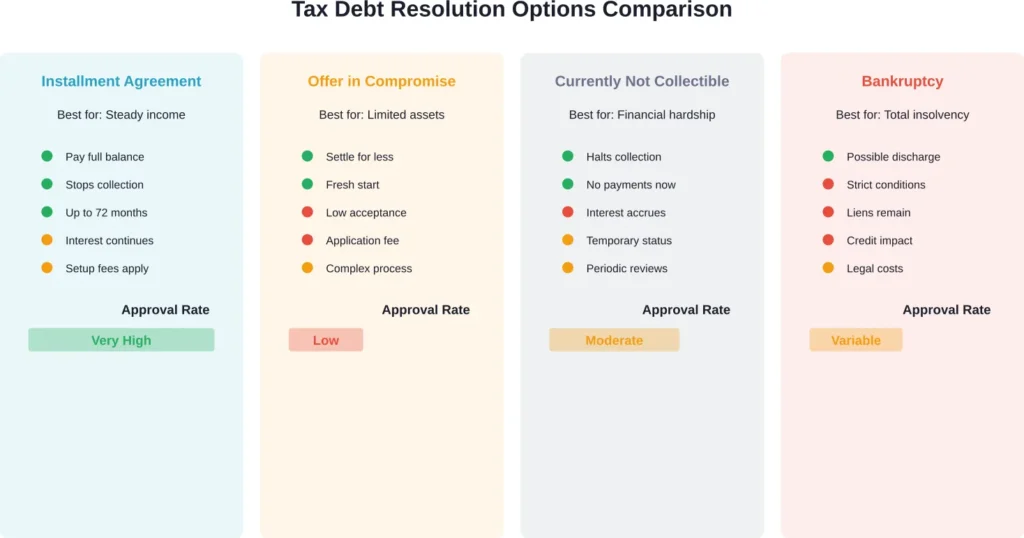

Offer in Compromise

An Offer in Compromise allows qualifying taxpayers to settle tax debt for less than the full amount owed. The IRS accepts offers when the amount represents the most the agency can expect to collect within a reasonable timeframe.

The IRS evaluates:

- Asset equity

- Income capacity

- Expenses allowed by IRS standards

- Ability to pay

Offers in Compromise sound attractive, but acceptance rates remain low. Historical data suggests the IRS approves a relatively small percentage of offers submitted annually. The agency rejects offers when it believes the taxpayer can pay through installment agreements or other means.

Currently Not Collectible Status

If paying any amount creates financial hardship, the IRS may place your account in Currently Not Collectible (CNC) status. This temporarily halts collection activities, though interest and penalties continue accruing.

The IRS periodically reviews CNC accounts. If financial conditions improve, collection resumes. If the Collection Statute Expiration Date passes while the account remains in CNC status, the debt may expire uncollected.

Bankruptcy

Some tax debts qualify for discharge in bankruptcy, though strict conditions apply. Generally, income tax debts may be dischargeable if:

- The tax return was due at least three years ago

- The return was filed at least two years ago

- The tax was assessed at least 240 days ago

- The return wasn’t fraudulent

- The taxpayer didn’t willfully attempt to evade taxes

Bankruptcy doesn’t discharge federal tax liens already filed, though it may eliminate personal liability.

Penalties and Interest That Never Stop

Here’s what makes large tax debts particularly painful: interest and penalties compound the original amount relentlessly.

According to IRS guidelines, unpaid tax debt accrues:

- Failure to Pay Penalty: 0.5% of unpaid taxes per month, up to 25% of the unpaid balance

- Interest: The federal short-term rate plus 3%, compounded daily

- Failure to File Penalty: 5% per month if returns remain unfiled, up to 25%

On a $30,000 tax debt, these charges can add hundreds of dollars monthly. Over time, penalties and interest can equal or exceed the original tax liability.

Payment plans don’t eliminate interest and penalties—they continue accruing until the balance reaches zero. This makes early resolution critical. Every month of delay increases the total amount owed.

How to Apply for IRS Payment Plans

The IRS strongly encourages online applications through your IRS Online Account. According to the agency, online applications receive immediate approval notifications for qualified taxpayers.

To apply online:

- Create an IRS Online Account at IRS.gov

- Verify your identity using photo identification

- Review your current tax balance and payment history

- Select the payment plan option that fits your situation

- Provide bank account information for direct debit (recommended)

- Receive immediate approval or denial notification

For debts exceeding $50,000, or if the online system doesn’t approve your request, contact the IRS at the number shown on your most recent notice. Be prepared to discuss your financial situation in detail.

What to Do Right Now

If you owe the IRS more than $25,000, taking immediate action protects your assets and reduces total costs.

First, file all required tax returns. The IRS won’t approve payment plans or other relief options while returns remain unfiled. Even if you can’t pay, filing prevents additional failure-to-file penalties.

Second, respond to IRS notices immediately. Ignoring correspondence escalates collection activities. Every notice includes contact information and response deadlines—use them.

Third, document your financial situation thoroughly. Whether applying for payment plans, offers in compromise, or hardship status, accurate financial documentation speeds approval and prevents delays.

Fourth, consider professional assistance. Tax attorneys, enrolled agents, and CPAs specializing in tax resolution understand IRS procedures and can negotiate on your behalf. For debts exceeding $25,000, professional fees often pay for themselves through better resolution outcomes.

Common Mistakes That Make Everything Worse

Certain actions guarantee worse outcomes when dealing with large tax debts.

Avoiding IRS communications ranks first. When taxpayers ignore notices and phone calls, the IRS assumes unwillingness to resolve the debt and accelerates enforcement. Every ignored notice moves you closer to levies and liens.

Continuing to accrue new tax debt while resolving old debt also creates problems. The IRS requires current compliance—filing returns and paying current taxes—before approving installment agreements or other relief. Additional tax debts can default existing payment plans.

Making promises you can’t keep sets up failure. Agreeing to monthly payments beyond your actual ability to pay inevitably results in default, which triggers immediate enforcement actions.

Hiding assets or income from the IRS during negotiations constitutes fraud. The penalties for providing false information on Collection Information Statements can exceed the original tax debt.

The Collection Statute Expiration Date

According to Internal Revenue Code provisions, the IRS generally has 10 years from the assessment date to collect tax debts through levy or court proceedings. This Collection Statute Expiration Date creates a theoretical endpoint for collection activities.

But here’s the catch: certain actions extend or suspend the CSED, including:

- Filing bankruptcy (suspends the CSED during bankruptcy plus six months)

- Submitting an Offer in Compromise (suspends during evaluation)

- Requesting a Collection Due Process hearing

- Filing lawsuits against the IRS

- Living outside the United States for six continuous months

Each suspension adds time to the 10-year collection period. Taxpayers who assume they can wait out the clock often discover the CSED extended years beyond the original expiration date.

Business Tax Debts Over $25,000

Business tax debts—particularly payroll tax liabilities—receive especially aggressive IRS treatment. The agency considers employment taxes as money held in trust for employees, making non-payment a serious offense.

For businesses, the IRS may pursue responsible persons individually through the Trust Fund Recovery Penalty. This makes officers, directors, or employees who willfully failed to pay employment taxes personally liable for the unpaid amount.

According to recent IRS updates, businesses now qualify for Simple Payment Plans in certain circumstances, expanding access to streamlined agreements previously limited to individuals.

Frequently Asked Questions

Yes, the IRS can seize and sell real property to satisfy tax debts, though this represents a last resort after other collection methods fail. The agency must provide notice and opportunity to resolve the debt before seizing a primary residence. Property seizures typically occur only when taxpayers refuse to cooperate with reasonable payment arrangements.

Not necessarily. For streamlined installment agreements, the monthly payment must pay the full balance before the Collection Statute Expiration Date (generally 10 years from assessment). For debts requiring financial disclosure, the IRS calculates payment capacity based on income minus allowable expenses. The agency may reject payment offers considered too low based on demonstrated ability to pay.

Generally yes, if the IRS approves your payment plan and you remain current on payments and tax filing obligations. However, the agency may still file a Notice of Federal Tax Lien even with an approved payment plan, particularly for larger balances. Defaulting on the payment plan immediately reinstates collection activities including levies and seizures.

The IRS doesn’t negotiate properly assessed tax liabilities. However, you can dispute the amount if you believe the assessment is incorrect by filing an appeal or amended return. For debts you legitimately owe, an Offer in Compromise may reduce the total amount based on inability to pay, though acceptance requires proving the offer represents the maximum the IRS can collect.

Request Currently Not Collectible status by demonstrating that making payments would create financial hardship preventing you from meeting basic living expenses. The IRS temporarily suspends collection activities, though interest and penalties continue accruing. The agency periodically reviews CNC status and resumes collection if financial conditions improve.

Resolution timeframes vary dramatically based on the method chosen. Streamlined installment agreements can be approved online in minutes but take up to 72 months to complete payments. Offers in Compromise typically take 6-12 months for IRS evaluation. Currently Not Collectible status can last months or years depending on financial circumstances. Professional representation often accelerates the resolution process.

Tax debt itself doesn’t appear on credit reports. However, the IRS files Notices of Federal Tax Lien as public records, which credit bureaus include in credit reports. Tax liens severely damage credit scores and remain on credit reports for years, affecting ability to obtain loans, credit cards, and sometimes employment. Recent changes mean some credit bureaus no longer include tax liens, but the public record remains accessible to lenders and employers who search court records.

Moving Forward With Large Tax Debt

Owing the IRS more than $25,000 creates legitimate financial stress, but it doesn’t mean financial ruin is inevitable. The tax code includes multiple pathways designed to resolve even substantial tax debts while protecting taxpayers from complete financial devastation.

The critical factor is action. Taxpayers who engage proactively with the IRS, file required returns, and work toward realistic resolution typically avoid the most severe collection consequences. Those who ignore the problem face liens, levies, and seizures that could be prevented through timely cooperation.

Every situation differs. Financial circumstances, the specific taxes owed, compliance history, and willingness to work with the IRS all influence available options and likely outcomes.

But the $25,000 threshold, while significant, isn’t a cliff edge. Payment plans, offers in compromise, hardship status, and other relief options remain available. The IRS, despite its reputation, operates under legal guidelines that include taxpayer protections and reasonable resolution options.

The worst approach is paralysis. Tax debts don’t improve with time—they worsen as interest and penalties compound. The sooner you address the debt, the more options remain available and the lower the total cost.

If you’re facing IRS debt exceeding $25,000, start by creating an IRS Online Account to view your exact balance and payment history. File any missing returns immediately. Then evaluate your financial capacity honestly and choose the resolution path that fits your circumstances. When in doubt, consult a tax professional who can navigate IRS procedures and negotiate on your behalf.

The debt is serious, but it’s manageable. Thousands of taxpayers successfully resolve large IRS debts every year through the programs described above. With informed action and persistence, you can too.