Quick Summary: If you become disabled while receiving Social Security retirement benefits, you cannot switch to SSDI since both programs use the same benefit amount based on your work record. However, if you’re already on SSDI and reach full retirement age, your benefits automatically convert to retirement benefits at the same payment level. Disabled individuals under retirement age should apply for SSDI, which provides benefits plus potential Medicare coverage after 24 months.

The intersection of disability and Social Security benefits creates confusion for millions of Americans. Understanding what happens when disability strikes during retirement—or how retirement affects existing disability benefits—requires navigating complex Social Security Administration rules.

Here’s the thing though—the answer depends entirely on which benefit came first and your current age.

Understanding SSDI vs. Retirement Benefits

Social Security Disability Insurance (SSDI) and retirement benefits operate under the same umbrella program, but serve different purposes. Both calculate payment amounts using identical formulas based on lifetime earnings records.

According to the Social Security Administration, SSDI provides monthly payments to people who have a disability that stops or limits their ability to work. To qualify, individuals must have worked in jobs covered by Social Security and accumulated sufficient work credits.

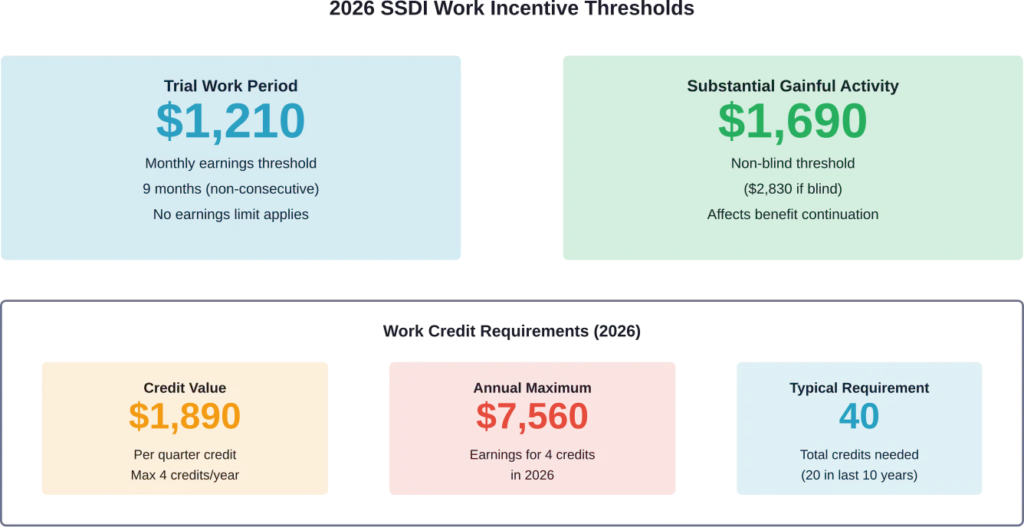

In 2026, workers earn one credit for each $1,890 in wages or self-employment income, with a maximum of four credits per year. Most disability applicants need 40 credits total, with 20 earned in the last 10 years before becoming disabled.

| Benefit Type | Eligibility Requirement | Payment Basis | Medicare Eligibility |

|---|---|---|---|

| SSDI | Disability + work credits | Lifetime earnings | After 24 months |

| Retirement | Age + work credits | Lifetime earnings | Age 65 |

| SSI | Disability + low income | Federal rate ($943 in 2026) | Immediate Medicaid |

If You’re Already Receiving Retirement Benefits

Becoming disabled after retirement benefits start doesn’t allow switching to SSDI. The payment amount remains identical because both programs use the same earnings calculation.

Real talk: There’s no financial advantage to changing benefit types. The Social Security Administration calculates both SSDI and retirement benefits from the same Primary Insurance Amount derived from your work history.

However, early retirement creates a complication. Taking retirement benefits before full retirement age permanently reduces the monthly amount to 75 percent or less of the full benefit. This reduction applies whether disability develops later or not.

That said, disabled individuals who took early retirement might qualify for Supplemental Security Income (SSI) if income and resources fall below program limits. According to source material provided, SSI provides monthly payments of up to $994, though this amount may vary by state and year.

If You’re Receiving SSDI Benefits

SSDI beneficiaries experience automatic conversion when reaching full retirement age. The Social Security Administration transitions disability benefits to retirement benefits seamlessly, maintaining the same payment amount.

According to SSA policy, this conversion happens without application or action required from beneficiaries. The benefit classification changes, but monthly payments continue uninterrupted.

Sound familiar? Many SSDI recipients worry this conversion reduces payments. It doesn’t. The amount stays constant because both programs reference identical earnings records.

Work Requirements and Eligibility

SSDI eligibility hinges on recent work history. The Social Security Administration requires applicants to have worked recently enough and long enough under Social Security coverage.

Younger workers need fewer credits. Workers disabled before age 24 might qualify with just six credits earned in the three years before disability onset. Those disabled between 24 and 31 need credits for half the time between age 21 and disability.

But wait. What defines disability for Social Security purposes?

According to SSA criteria, disability means inability to engage in substantial gainful activity due to a medically determinable physical or mental impairment expected to last at least 12 consecutive months or result in death. In 2026, substantial gainful activity means earning $1,690 or more monthly ($2,830 for blind individuals).

Medical Requirements and the Definition of Disability

The Social Security Administration maintains strict disability definitions. Medical conditions must meet severity standards outlined in SSA’s Blue Book of listed impairments or equal their severity.

SSA evaluates disability through a five-step sequential process:

- Current work activity assessment

- Severity determination of medical condition

- Comparison against listed impairments

- Past work capability evaluation

- Any work capability assessment

The process considers age, education, and transferable work skills. Older workers face less stringent standards because adapting to new work types becomes increasingly difficult with age.

Trial Work Period and Return to Work

SSDI beneficiaries can test their ability to work without immediately losing benefits. The trial work period allows nine months of work activity while receiving full disability payments.

In 2026, any month with earnings exceeding $1,210 before taxes counts toward the trial. These months need not be consecutive—just within a rolling five-year period. No earnings limit applies during these nine months.

After the trial work period ends, a 36-month extended eligibility period begins. During this phase, beneficiaries receive payments for months when earnings fall below substantial gainful activity levels.

Medicare and Health Coverage Considerations

SSDI beneficiaries automatically qualify for Medicare 24 months after disability entitlement begins. The Social Security Administration handles enrollment automatically, sending welcome packages approximately three months before coverage starts.

This creates a significant advantage over retirement benefits for disabled individuals under age 65. Early retirees must wait until 65 for Medicare, while SSDI recipients gain access based on disability duration.

Continuing Disability Reviews periodically verify ongoing eligibility. Review frequency depends on improvement likelihood—from every six months to every seven years. Medical improvement or return to substantial work can terminate benefits.

Frequently Asked Questions

No. Social Security does not pay both SSDI and retirement benefits because both programs calculate payments from identical earnings records. Beneficiaries receive whichever amount is higher—which remains the same for both programs.

SSDI automatically converts to retirement benefits at full retirement age. The monthly payment amount stays constant, and Medicare coverage continues uninterrupted. The Social Security Administration handles this conversion without requiring application or action from beneficiaries.

Technically yes, but it provides no financial benefit. Both programs use the same benefit calculation, so switching from early retirement to SSDI won’t increase monthly payments. The early retirement reduction remains permanent regardless of subsequent disability.

Initial SSDI decisions typically take three to five months. Denied applicants can appeal through multiple levels—reconsideration, administrative law judge hearing, Appeals Council review, and federal court. The entire appeals process can extend one to two years depending on case complexity.

Not necessarily. Earnings below substantial gainful activity levels ($1,690 monthly in 2026 for non-blind individuals) don’t automatically disqualify applicants. The Social Security Administration evaluates whether work constitutes substantial activity based on earnings, hours, and job responsibilities.

Certain severe conditions meet SSA’s Compassionate Allowances criteria for expedited processing, including specific cancers, early-onset Alzheimer’s disease, and ALS. However, applicants must still meet work credit requirements and demonstrate the condition prevents substantial work activity.

SSDI benefits receive annual cost-of-living adjustments matching Social Security’s overall COLA increases. However, the base benefit amount remains tied to earnings records and doesn’t increase through continued disability or medical worsening.

Making the Right Choice for Your Situation

Disability during Social Security receipt requires careful analysis of timing, benefit types, and long-term implications. The automatic SSDI-to-retirement conversion protects beneficiaries from payment reductions while maintaining Medicare access.

For those considering early retirement who might become disabled, understanding that both programs yield identical payment amounts helps inform decisions. The primary advantage of SSDI over early retirement lies in earlier Medicare eligibility and protection from permanent early-claim reductions.

Consulting with Social Security representatives provides personalized guidance based on individual work histories and circumstances. The SSA offers free benefit estimates through online accounts, helping applicants understand potential payment amounts before filing.

Ready to explore Social Security options? Create a my Social Security account at SSA.gov to view personalized benefit estimates and understand how disability or retirement timing affects your financial future.