Quick Summary: Filing bankruptcy triggers a federal court process that either discharges debts through liquidation (Chapter 7) or creates a repayment plan (Chapter 13). You’ll complete credit counseling, pay filing fees, attend a creditors’ meeting, and potentially surrender non-exempt assets. Bankruptcy remains on credit reports for 7-10 years but provides immediate relief from collections and creditor harassment.

Bankruptcy isn’t just about financial failure. It’s a legal mechanism designed to give people drowning in debt a path forward.

According to the U.S. Bankruptcy Code, bankruptcy helps people who can no longer pay their debts get a fresh start by liquidating assets or creating a repayment plan. Between 2008 and 2023, consumers filed 13.8 million bankruptcy cases across the ninety-four federal bankruptcy districts in the United States, generating over $4 billion in court filing fees alone.

But what actually happens when you file? The process involves federal courts, trustees, creditor meetings, and strict timelines. Understanding each step helps determine whether bankruptcy makes sense for your situation.

Types of Bankruptcy and How They Work

Not all bankruptcies function the same way. The type you file determines what happens to your assets, debts, and financial future.

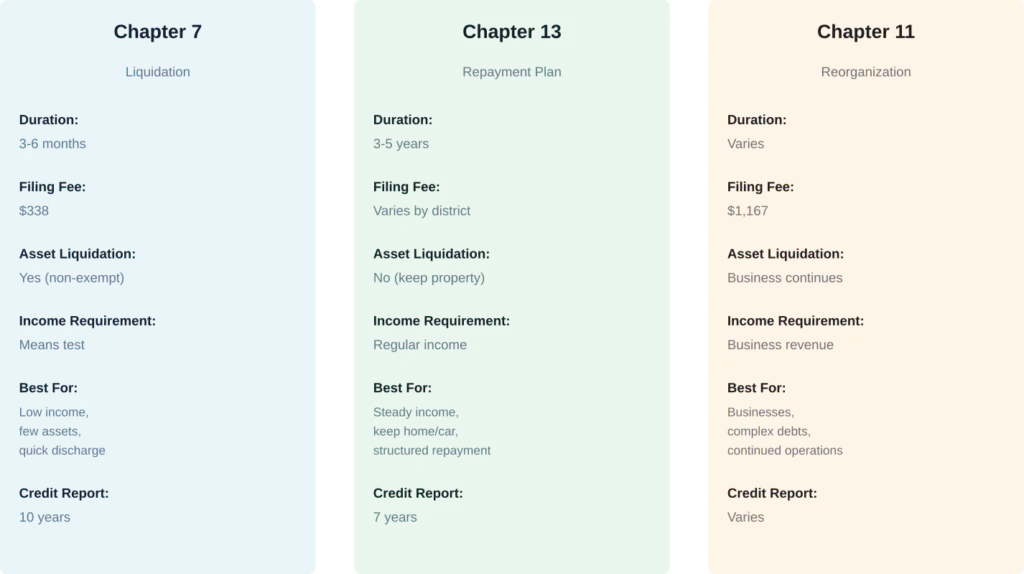

Chapter 7: Liquidation Bankruptcy

Chapter 7 provides for liquidation—the sale of a debtor’s nonexempt property and distribution of proceeds to creditors. This is the most common form for individuals seeking a clean slate.

The process moves quickly, typically completing in three to six months. A court-appointed trustee reviews your assets, sells anything not protected by exemptions, and distributes the money to creditors.

Here’s the catch: not everyone qualifies. If your current monthly income exceeds your state’s median, you’ll face a means test. This calculation determines whether filing Chapter 7 would be considered abusive.

According to the U.S. Trustee Program, if your disposable income over five years (net of certain statutory expenses) could pay a significant portion of unsecured debts, the court may dismiss your case or require conversion to Chapter 13.

Chapter 13: Wage Earner’s Plan

Chapter 13 enables individuals with regular income to develop a plan to repay all or part of their debts. Instead of liquidating assets, you make installment payments to creditors over three to five years.

Income thresholds for means testing vary by state and change regularly. Consult current U.S. Trustee guidelines for your state’s median income.

If your current monthly income sits below the state median, the plan typically runs three years. Above the median? You’re looking at five years.

Chapter 13 acts like a consolidation loan. You make monthly payments to a Chapter 13 trustee who distributes funds to creditors. Direct contact with creditors stops completely.

Chapter 11: Business Reorganization

Chapter 11 generally provides for reorganization, usually involving corporations or partnerships. Businesses can also seek relief under Chapter 11 to keep operations alive while restructuring debts.

The debtor typically remains “in possession,” operating the business while proposing a reorganization plan. Creditors vote on the plan, and if it receives required votes and satisfies legal requirements, the court confirms it.

Chapter 11 filing fees are $1,167 plus a $571 miscellaneous administrative fee (as documented in official sources).

The Step-by-Step Bankruptcy Process

Filing bankruptcy follows a structured federal process with specific deadlines and requirements.

Step 1: Credit Counseling Course

Before filing Chapter 7 bankruptcy, you must complete a credit counseling course from an approved agency. This requirement can only be waived if the United States Trustee determines insufficient approved agencies exist in your area.

If a debt management plan develops during counseling, it must be filed with the court.

Step 2: Filing the Petition

A bankruptcy case begins when the debtor files a petition with the bankruptcy court. Individuals can file alone, spouses can file together, or corporations and other entities can file.

For Chapter 7, the filing fee sits at $338 (as of the time source was published). Chapter 13 fees vary by district (fees differ by jurisdiction).

All bankruptcy cases are handled in federal courts under rules outlined in the U.S. Bankruptcy Code. The petition triggers an automatic stay—immediate legal protection that stops most creditors from seeking to collect debts.

Step 3: The Automatic Stay

The moment your petition is filed, the automatic stay goes into effect. This powerful legal mechanism halts:

- Creditor phone calls and collection letters

- Wage garnishments

- Foreclosure proceedings

- Repossession actions

- Utility disconnections

- Eviction processes (in most cases)

Real talk: this immediate relief represents one of bankruptcy’s most valuable benefits. The constant harassment stops overnight.

Step 4: Meeting of Creditors

Within 21 to 40 days after filing, the bankruptcy trustee schedules a meeting of creditors (called a 341 meeting). Despite the name, creditors rarely attend.

The bankruptcy trustee conducts this meeting, asking questions about your petition, assets, debts, and financial situation under oath. Questions typically cover:

- Whether you reviewed the petition before signing

- If all assets and debts are accurately listed

- How you valued property

- Whether you expect to receive money from inheritances or lawsuits

- Whether you’ve transferred property recently

The meeting usually lasts 10-15 minutes unless complications arise.

Step 5: Asset Evaluation and Liquidation

In Chapter 7, the trustee reviews your assets to determine what can be sold to pay creditors. But here’s where exemptions come in.

Federal law protects certain property from liquidation. Federal exemptions include a homestead exemption of $31,575 (amounts subject to periodic adjustment). If your home equity falls below this amount, the property remains exempt.

Other federal exemptions include:

- $2,125 for jewelry

- $3,175 for tools of your trade

- $16,850 in aggregate ($800 per item) for household goods, furnishings, appliances, clothing, animals, books, crops, or musical instruments

Many states offer alternative exemption schemes. Some provide more generous protections than federal exemptions.

In Chapter 13, asset liquidation doesn’t occur. Instead, you keep property while making plan payments.

Step 6: Debt Discharge or Plan Confirmation

For Chapter 7, the discharge typically arrives three to six months after filing. This legal order releases you from personal liability for discharged debts.

For Chapter 13, the court must confirm your repayment plan before payments begin. Once you complete all plan payments (three to five years later), you receive a discharge.

What Debts Get Discharged in Bankruptcy

Bankruptcy doesn’t eliminate all debts. Understanding which obligations disappear and which survive matters enormously.

Dischargeable Debts

Most unsecured consumer debts qualify for discharge:

- Credit card balances

- Medical bills

- Personal loans

- Utility bills

- Past-due rent (in most cases)

- Business debts from sole proprietorships

- Collection accounts

- Lawsuit judgments (with some exceptions)

Once discharged, creditors cannot attempt collection. They can’t call, write, sue, garnish wages, or take any action to collect the debt.

Non-Dischargeable Debts

Federal law specifically excludes certain debts from discharge. These survive bankruptcy and must be repaid:

- Most domestic support obligations (child support, alimony)

- Most student loans (except in cases of undue hardship)

- Recent tax debts (typically less than three years old)

- Debts from fraud or willful injury

- Government fines and penalties

- DUI-related debts

- HOA fees that continue accruing post-filing

Student loans deserve special mention. They’re notoriously difficult to discharge, requiring proof of “undue hardship”—a high legal bar that few meet.

But tax debts? Those sometimes qualify for discharge if they meet specific criteria: the tax return was due at least three years before filing, you filed the return at least two years before bankruptcy, and the IRS assessed the tax at least 240 days before filing.

Secured Debts Work Differently

Mortgages and car loans are secured—the property serves as collateral. Bankruptcy can discharge your personal obligation to pay, but the lien remains on the property.

Translation: the lender can still foreclose or repossess if you don’t pay. To keep the property, you’ll need to either:

- Continue making payments (reaffirmation in Chapter 7)

- Include payments in your Chapter 13 plan

- Surrender the property and walk away

What Happens to Your Property and Assets

The biggest fear many people have about bankruptcy? Losing everything they own.

The reality is more nuanced.

Exempt vs. Non-Exempt Property

Bankruptcy law distinguishes between exempt property (protected) and non-exempt property (vulnerable to liquidation).

Every state maintains exemption laws. Some states allow filers to choose between state exemptions or federal exemptions. Others require using state exemptions only.

Federal exemptions include homestead protections (amounts vary by state and are subject to periodic adjustment). Consult current federal or state exemption schedules for exact amounts. State exemptions vary wildly—some states like Texas and Florida offer unlimited homestead protection, while others cap it much lower.

Common exempt items typically include:

- Primary residence (up to exemption amount)

- One vehicle (up to a certain equity value)

- Household goods and furnishings

- Clothing

- Retirement accounts (401k, IRA)

- Tools needed for your profession

- Public benefits (Social Security, unemployment)

What Could Be Liquidated

Non-exempt assets might include:

- Second homes or investment property

- Expensive vehicles with substantial equity

- Valuable collections (art, coins, antiques)

- Cash or bank accounts above exemption limits

- Non-retirement investment accounts

- Business equipment beyond exemption amounts

In Chapter 7, the trustee can sell these items and distribute proceeds to creditors. In Chapter 13, you keep the property but your repayment plan must pay creditors at least what they would have received in a Chapter 7 liquidation.

Reaffirmation Agreements

For secured debts like car loans, you might sign a reaffirmation agreement. This legal document essentially takes the debt out of bankruptcy—you agree to remain personally liable in exchange for keeping the property.

Courts scrutinize these agreements carefully. They must not create undue hardship, and you have the right to cancel within 60 days.

The Credit Impact of Filing Bankruptcy

Bankruptcy tanks credit scores. No sugarcoating it.

But the impact isn’t permanent, and recovery often happens faster than expected.

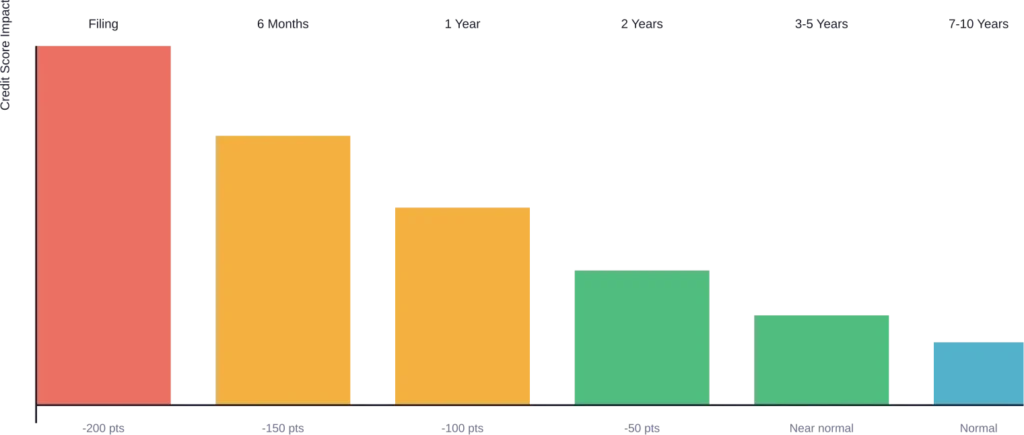

How Long Bankruptcy Stays on Credit Reports

According to the Fair Credit Reporting Act, bankruptcy information appears on credit reports for:

- Chapter 7: 10 years from the filing date (per Fair Credit Reporting Act standards)

- Chapter 13: 7 years from the filing date

Individual discharged accounts may fall off sooner—typically seven years from the date of first delinquency.

Immediate Score Impact

Bankruptcy typically causes credit score reductions, with impact varying based on pre-filing score. Someone with a 780 score might see a larger point drop than someone already at 550. But percentage-wise, both experience significant damage.

Recovery Timeline

Here’s where it gets interesting. A Yale School of Management study found that once bankruptcy flags are removed from credit reports, access to credit improves substantially.

One year after Chapter 13 bankruptcy discharge, former Chapter 13 filers showed improved mortgage access compared to those still under bankruptcy protection. The study suggests bankruptcy may not hurt future employment and credit prospects as severely as commonly believed.

Many experts suggest that rebuilding credit post-bankruptcy follows a predictable pattern:

- Months 1-6: Scores remain low; focus on stability

- Months 6-12: Small improvements with responsible behavior

- Year 2: Secured credit cards and small loans become available

- Years 3-5: Conventional loans possible with higher interest rates

- Years 7-10: Credit normalizes as bankruptcy ages

Getting Credit After Bankruptcy

Contrary to popular belief, credit availability doesn’t disappear entirely post-bankruptcy.

Secured credit cards—where you deposit cash as collateral—become available almost immediately. Car loans, while expensive, often appear within 1-2 years. FHA mortgages become possible two years after Chapter 7 discharge or one year into a Chapter 13 plan with court approval.

The catch? Interest rates run higher. Lenders price in the bankruptcy risk.

Consequences Beyond Credit Scores

Bankruptcy creates ripple effects that extend into other areas of life.

Employment Implications

Can bankruptcy affect your job? It depends.

Federal law prohibits government employers from discriminating based on bankruptcy. Private employers occupy a grayer area—they can’t fire you solely for filing bankruptcy, but they can consider it for positions involving financial responsibility.

Harvard Law research on Chapter 11 business bankruptcies found that employees begin leaving at-risk companies months or years before bankruptcy—not because of the filing itself, but due to underlying financial instability. The filing may actually help retain workers long-term by stabilizing the business.

For individuals, background checks might reveal bankruptcy if employers pull credit reports. Jobs in banking, finance, law enforcement, and positions requiring security clearances often involve credit checks.

Housing Challenges

Landlords frequently check credit. A bankruptcy on your record might trigger:

- Application denials

- Requirements for larger security deposits

- Demands for co-signers

- Higher rent

But it’s not insurable. Explanation letters, proof of stable income, and good rental history help overcome bankruptcy stigma.

Public Records

Bankruptcy filings are public records. Anyone can access them through PACER (Public Access to Court Electronic Records).

This means potential employers, landlords, business partners, or nosy neighbors can find your bankruptcy filing if they look.

Repeat Filing Restrictions

Federal law limits how often you can file bankruptcy and receive a discharge:

- After Chapter 7 or 11 discharge: Must wait 8 years to file another Chapter 7

- After Chapter 7: Must wait 4 years to file Chapter 13

- After Chapter 13: Must wait 6 years to file Chapter 7 (with exceptions)

- After Chapter 13: Must wait 2 years to file another Chapter 13

A Northwestern University Law Review study revealed a startling trend: nearly 46% of the consumers who filed bankruptcy in 2023 were repeat filers, defined as individuals with at least one prior bankruptcy record since 1997.

This percentage has followed an overall upward trend, increasing at an average annual rate of 52 basis points since 2016. The U.S. District Court for the Western District of Tennessee has the highest percentage of repeat filers, with 76% of all filings coming from individuals with prior bankruptcy records. The Southern District of West Virginia has the lowest percentage, with 36% of filings attributed to repeat filers.

These findings challenge assumptions about bankruptcy providing a permanent “fresh start” and raise questions about whether the system adequately addresses root causes of financial distress.

| Previous Bankruptcy Type | New Chapter 7 Filing | New Chapter 13 Filing |

|---|---|---|

| Chapter 7 Discharge | 8 years wait | 4 years wait |

| Chapter 13 Discharge | 6 years wait (exceptions apply) | 2 years wait |

| Chapter 11 Discharge | 8 years wait | Varies |

| Chapter 12 Discharge | 8 years wait | 4 years wait |

Alternatives to Filing Bankruptcy

Bankruptcy isn’t the only option when debt becomes overwhelming.

Debt Consolidation

Combining multiple debts into a single loan with lower interest can make payments manageable. This works when you have decent credit and steady income.

The downside? You’re not reducing the principal—just reorganizing it.

Debt Management Plans

Credit counseling agencies (like those accredited by the National Foundation for Credit Counseling) negotiate with creditors to reduce interest rates and create structured payment plans.

These programs typically run 3-5 years and require closing credit cards. But they avoid bankruptcy’s stigma while still addressing debt.

Debt Settlement

Negotiating with creditors to accept less than the full balance owed can work for consumers with lump sums available.

Settlement companies charge fees, and settled debts create taxable income. Creditors might also sue before agreeing to settlements.

Informal Negotiations

Directly contacting creditors to request hardship programs, interest rate reductions, or payment plans costs nothing and sometimes succeeds.

Many creditors prefer receiving something over nothing.

Do Nothing

Sound crazy? In certain situations, doing nothing makes strategic sense.

If you’re “judgment proof”—meaning you have no assets or income creditors can legally seize—they can sue and win but can’t collect. Social Security income, for instance, is generally protected from garnishment.

Statutes of limitation eventually expire on most debts (typically 3-6 years depending on the state). Once expired, creditors lose the legal right to sue, though they can still ask for payment.

Special Considerations for Specific Debts

Medical Debt and Bankruptcy

Medical debt has historically been one of the leading causes of bankruptcy filings. These debts are typically unsecured and fully dischargeable.

Before filing, verify that medical bills are accurate and that insurance processed claims correctly. Hospital billing errors are common, and financial assistance programs often exist for qualifying patients.

Tax Debt and Bankruptcy

The IRS notes that bankruptcy may be an option for past-due federal taxes, though payment plans and offers in compromise provide alternatives.

For Chapter 13 filers, you must file all required tax returns for periods ending within four years of bankruptcy filing. Priority tax debts must be paid in full through the plan, while older tax debts might qualify for discharge.

Student Loans

Student loans rarely discharge in bankruptcy without proving “undue hardship”—a standard so strict that most attempts fail.

Income-driven repayment plans, deferment, forbearance, or Public Service Loan Forgiveness often provide better relief for struggling student loan borrowers.

The Financial Cost of Filing Bankruptcy

Bankruptcy isn’t free. Understanding the total cost helps with decision-making.

Court Filing Fees

- Chapter 7: $338 (based on sources current through 2025)

- Chapter 13: Varies by district (fees differ by jurisdiction)

- Chapter 11: $1,167

Fee waivers or installment payment plans exist for qualifying low-income filers in Chapter 7.

Attorney Fees

Most bankruptcy attorneys charge flat fees:

- Chapter 7: $1,000-$3,500 depending on complexity and location

- Chapter 13: $3,000-$6,000, often payable through the repayment plan

- Chapter 11: $10,000+ due to complexity

While technically possible to file pro se (without an attorney), bankruptcy’s complexity makes this risky. One mistake can lead to dismissal or loss of exempt property.

Credit Counseling and Debtor Education

Both courses cost roughly $10-50 each from approved providers. These mandatory courses can’t be waived except in rare circumstances.

Trustee Fees

In Chapter 13, trustees receive a percentage of plan payments (typically 3-10% depending on the district). This cost is built into your monthly payment.

In Chapter 7, the trustee’s fee comes from liquidated assets, not your pocket directly.

Hidden Costs

Beyond direct fees, consider:

- Lost time from work for meetings and court appearances

- Higher insurance rates (some insurers use credit scores)

- Higher interest rates on future loans

- Opportunity costs from damaged credit

Life After Bankruptcy: The Recovery Process

Bankruptcy isn’t the end—it’s a reset button. But recovery requires intentional effort.

Immediate Post-Discharge Steps

Once you receive your discharge:

- Obtain your discharge papers and keep them permanently

- Pull credit reports from all three bureaus (Equifax, Experian, TransUnion)

- Verify discharged debts show zero balance

- Dispute any errors with credit bureaus

- Set up fraud alerts or credit monitoring

The Federal Trade Commission notes that consumers have the right to dispute errors on credit reports. If discharged debts still show balances or active collection status, file disputes immediately.

Building New Credit

Secured credit cards offer the fastest path to rebuilding:

- Deposit $200-500 as collateral

- Receive a credit card with a matching limit

- Make small purchases and pay in full monthly

- After 12-18 months, graduate to unsecured cards

Credit-builder loans from credit unions also help. You borrow a small amount that’s held in a savings account while you make payments. Once paid off, you receive the funds plus a positive payment history on your credit report.

Financial Habits That Prevent Repeat Filing

With 46% of 2023 bankruptcy filers being repeat filers, clearly many people struggle to maintain financial stability post-bankruptcy.

Preventing repeat filing requires:

- Emergency fund accumulation (start with $500, build to 3-6 months expenses)

- Budgeting with actual tracking (not just intentions)

- Avoiding new debt during the first 2 years

- Adequate insurance (health, disability, auto, renters/homeowners)

- Income diversification or skills development

The National Foundation for Credit Counseling emphasizes that filing bankruptcy is the financial equivalent of emergency surgery—necessary in crisis but requiring serious rehabilitation afterward.

When Bankruptcy Makes Sense (And When It Doesn’t)

Not everyone drowning in debt should file bankruptcy.

Good Candidates for Bankruptcy

Filing makes sense when:

- Debt exceeds annual income by 2x or more

- Creditors are actively garnishing wages

- Foreclosure or repossession is imminent

- Most debts are unsecured and dischargeable

- No recent luxury purchases or cash advances

- You’ve explored alternatives without success

- Medical crisis created overwhelming debt

- Job loss eliminated repayment ability

Poor Candidates for Bankruptcy

Bankruptcy might be premature or ineffective when:

- Most debts are non-dischargeable (student loans, recent taxes, child support)

- You recently transferred assets or made large purchases

- Income significantly exceeds expenses

- Debt is manageable with budgeting adjustments

- You’ll need to make major purchases soon (home, car)

- You already filed bankruptcy recently

- Retirement accounts could cover debts (don’t raid these in most cases)

Timing Considerations

According to U.S. Courts, the timing of bankruptcy filing can be crucial. Consider waiting if:

- You’ll receive a tax refund, bonus, or inheritance soon (might become part of bankruptcy estate)

- Recent luxury purchases could be challenged as fraudulent

- A lawsuit judgment hasn’t finalized yet

- You’re about to qualify for student loan forgiveness

Conversely, file sooner when foreclosure sales are scheduled or garnishments are draining accounts.

Common Bankruptcy Myths Debunked

Misconceptions about bankruptcy prevent some people from getting needed relief while encouraging others to file prematurely.

Myth: Bankruptcy Means Losing Everything

Exemptions protect most people’s basic property. Many Chapter 7 filers lose nothing because everything they own falls under exemption limits.

Myth: Both Spouses Must File

Spouses can file jointly or individually. If most debt belongs to one spouse, individual filing might make more sense.

Myth: Bankruptcy Eliminates All Debts

As covered earlier, student loans, recent taxes, child support, alimony, and debts from fraud survive bankruptcy.

Myth: Everyone Will Know

While bankruptcy is public record, most people never check PACER. Unless you’re a public figure or someone has reason to investigate, filings typically fly under the radar.

Myth: Bankruptcy Ruins Credit Forever

Credit scores start recovering within months of discharge. After seven to ten years, bankruptcy falls off credit reports entirely.

Myth: You Can’t Get Credit for Years

Secured credit cards are available immediately. Car loans within 1-2 years. Mortgages within 2-4 years depending on the bankruptcy chapter and loan type.

Myth: Bankruptcy Is Immoral or Irresponsible

Bankruptcy exists precisely because lawmakers recognized that financial catastrophes happen. Medical emergencies, job losses, divorces, and economic downturns can devastate finances through no fault of the debtor.

Frequently Asked Questions

Chapter 7 typically completes in 3-6 months from filing to discharge. Chapter 13 runs 3-5 years depending on income level and the repayment plan structure. Chapter 11 varies widely based on complexity but often takes 1-2 years for small businesses.

Usually yes, if you’re current on payments and the equity falls within exemption limits. For Chapter 7, you may need to reaffirm the loans. For Chapter 13, you continue making payments through the plan. Federal exemptions include homestead protections (amounts vary by state and are subject to periodic adjustment). Consult current federal or state exemption schedules for exact amounts.

Not necessarily. Employers don’t receive automatic notification. However, if your employer pulled a credit report for hiring or if you’re subject to security clearance, they might discover it. Federal law prohibits government employers from discriminating based on bankruptcy. Private employers face restrictions but can consider bankruptcy for certain positions.

Legally yes, but it’s risky. Bankruptcy involves complex federal procedures, exemption calculations, and legal filings. Mistakes can result in case dismissal, loss of property, or denial of discharge. Chapter 7 attorney fees typically range $1,000-$3,500, while Chapter 13 runs $3,000-$6,000 and can be paid through the repayment plan.

Bankruptcy typically causes credit score reductions, with impact varying based on pre-filing score. Those with higher scores often see larger drops. However, if you were already delinquent on multiple accounts before filing, the additional bankruptcy impact might be smaller since your score was already damaged.

It depends on the previous and new bankruptcy type. After a Chapter 7 discharge, you must wait 8 years to file another Chapter 7, or 4 years to file Chapter 13. After Chapter 13 discharge, wait 6 years for Chapter 7 (with exceptions) or 2 years for another Chapter 13. Research shows nearly 46% of 2023 bankruptcy filers had prior bankruptcy records since 1997.

No. While most unsecured debts like credit cards and medical bills discharge completely, certain debts survive bankruptcy including most student loans, recent tax debts, child support, alimony, debts from fraud or willful injury, government fines, and DUI-related obligations. Secured debts like mortgages and car loans are discharged as personal obligations, but liens remain on the property.

Finding Professional Help

Navigating bankruptcy alone is possible but not advisable for most people.

Bankruptcy Attorneys

Look for attorneys who specialize in bankruptcy specifically, not general practitioners. Many offer free consultations. Questions to ask:

- How many bankruptcy cases have you handled?

- What percentage of your practice is bankruptcy?

- Do you recommend Chapter 7 or 13 for my situation?

- What are the total costs, including filing fees?

- What documents will I need to provide?

State bar associations maintain attorney directories. The National Association of Consumer Bankruptcy Attorneys provides referrals.

Credit Counseling Agencies

The mandatory credit counseling course must come from an approved provider. The U.S. Trustee Program maintains a list of approved agencies by state.

Many agencies also offer ongoing financial counseling post-bankruptcy. The National Foundation for Credit Counseling (NFCC) represents a network of nonprofit credit counseling agencies nationwide.

Legal Aid Organizations

Low-income filers might qualify for free legal services. Legal aid organizations sometimes handle bankruptcy cases or provide limited assistance with form completion.

The Legal Services Corporation maintains a directory of legal aid programs. Some law schools operate bankruptcy clinics where supervised students provide assistance.

Final Thoughts: Is Bankruptcy Right for You?

Bankruptcy represents one of the most consequential financial decisions anyone makes. The process provides genuine relief from overwhelming debt but carries costs—financial, emotional, and reputational.

For some people, bankruptcy offers the only realistic path from crushing debt to financial stability. Medical bankruptcies, job loss situations, and cases involving predatory lending often fall into this category.

For others, alternatives like debt management plans, settlement negotiations, or simple budgeting adjustments provide sufficient relief without bankruptcy’s lasting consequences.

The key is honest assessment. Can you realistically repay your debts within five years through budgeting and possibly a second job? Or has debt become genuinely unmanageable?

Consider consulting a bankruptcy attorney for a free evaluation even if you’re unsure. Understanding your options costs nothing and provides clarity.

Remember that 13.8 million Americans filed bankruptcy between 2008 and 2023. You’re not alone. Financial setbacks happen to hardworking, responsible people every day.

Bankruptcy exists because society recognizes that sometimes, people need a second chance. Using that mechanism wisely—when truly necessary—isn’t failure. It’s a strategic reset that allows rebuilding.

Take action today: If you’re struggling with unmanageable debt, schedule consultations with both a bankruptcy attorney and a nonprofit credit counseling agency. Compare your options objectively. Whether bankruptcy is right for you depends on your specific situation—but understanding the process is the first step toward informed decision-making.