Quick Summary: Going over your credit limit can result in declined transactions, over-limit fees (typically $25-$35), and damage to your credit score through increased credit utilization. However, transactions only process above your limit if you’ve opted into over-limit protection—otherwise, purchases exceeding your limit are automatically declined.

Standing at the checkout counter watching your credit card get declined is frustrating. Even worse? Discovering later that you’ve racked up fees because you exceeded your credit limit without realizing it.

The consequences of going over your credit limit extend beyond immediate embarrassment. Depending on your card issuer’s policies and whether you’ve enrolled in certain protections, you could face declined transactions, penalty fees, or damage to your credit score.

Here’s the thing though—not all credit cards handle over-limit situations the same way. Federal regulations introduced through the Credit Card Accountability Responsibility and Disclosure Act of 2009 (CARD Act) fundamentally changed how issuers manage over-limit transactions.

Can You Actually Go Over Your Credit Limit?

The short answer? Sometimes, but only if you’ve specifically opted in.

According to the Consumer Financial Protection Bureau, card issuers cannot allow you to exceed your credit limit unless you’ve affirmatively consented to over-limit protection. This opt-in requirement is a key protection established under Regulation Z, which implements provisions of the CARD Act.

Without this opt-in, your transaction gets declined when you attempt to charge more than your available credit. The card issuer simply won’t authorize the purchase.

But if you’ve enrolled in over-limit coverage, the issuer may approve transactions that push you beyond your limit. That approval comes with consequences, which we’ll examine next.

What Happens When You Exceed Your Limit

Several outcomes become possible once you cross that credit threshold. The specific consequences depend on your card agreement and whether you’ve opted into over-limit protection.

Your Transaction Gets Declined

For cardholders who haven’t opted into over-limit protection, this is the most common outcome. The card issuer denies authorization for any purchase that would exceed your credit limit.

Real talk: This is actually the safest scenario. While momentarily inconvenient, a declined transaction prevents you from triggering fees or damaging your credit utilization ratio.

You Get Charged Over-Limit Fees

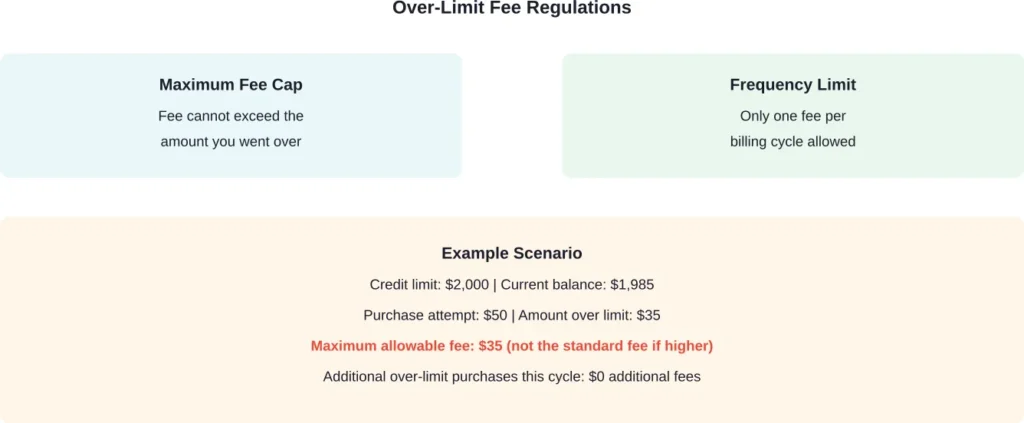

When you’ve opted into over-limit protection and the issuer approves a transaction exceeding your limit, you’ll typically face an over-limit fee. According to the Consumer Financial Protection Bureau, these fees are typically around $25 to $35.

Federal regulations impose important restrictions on these fees. Under the CARD Act, the fee cannot exceed the amount you went over your limit. So if you exceeded your limit by $20, the maximum fee is $20, not the standard $35.

Additionally, card issuers can only charge one over-limit fee per billing cycle, regardless of how many transactions push you above your limit during that period.

Your Credit Utilization Increases

Credit utilization—the percentage of available credit you’re using—accounts for roughly 30% of your FICO score calculation. When you go over your limit, you’re using over 100% of that card’s available credit. This dramatically increases your utilization ratio on that specific card and potentially your overall utilization if that card represents a significant portion of your total available credit.

Lenders view lower utilization ratios more favorably. High credit utilization signals financial stress to lenders and credit scoring models, which can result in a lower credit score.

Your Minimum Payment Increases

Exceeding your credit limit means you’re carrying a higher balance. Minimum payment calculations typically represent a percentage of your total balance (often 1-3% plus any fees and interest).

The over-limit fee itself gets added to your balance, and you’ll owe a minimum payment that covers this increased total. Missing or making only partial minimum payments creates additional problems, including late fees and further credit score damage.

How Over-Limit Spending Damages Your Credit Score

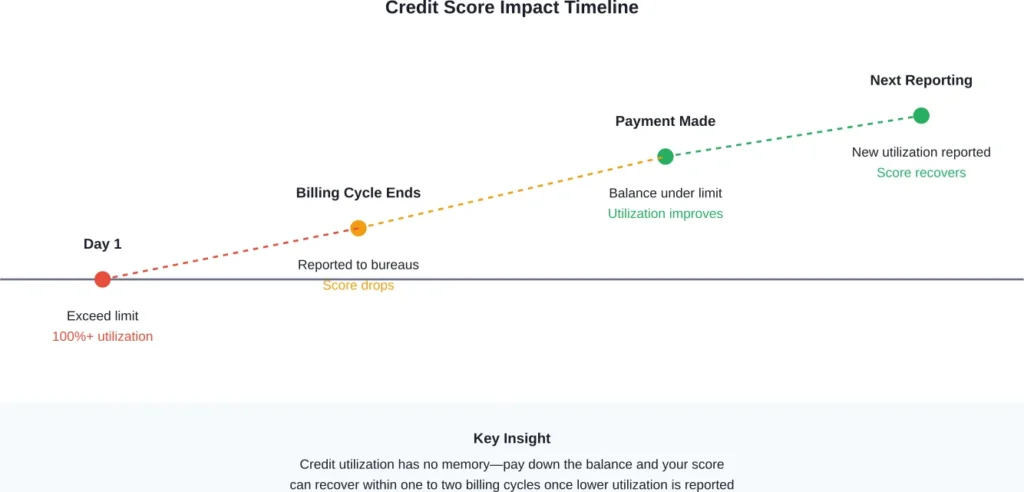

The credit score impact from exceeding your limit stems primarily from credit utilization, which accounts for roughly 30% of your FICO score calculation.

When you go over 100% utilization on a card, credit bureaus record this elevated usage. Even if you have other cards with available credit, the per-card utilization matters alongside your overall utilization across all accounts.

That said, credit utilization has no memory in scoring models. Once you pay down the balance and your updated utilization gets reported to credit bureaus, your score can recover relatively quickly—assuming you haven’t triggered other negative factors like missed payments.

Strategies to Avoid Exceeding Your Credit Limit

Prevention beats recovery. Here are practical approaches to keep your balance safely below your limit.

Monitor Your Balance Regularly

Most card issuers provide mobile apps with real-time balance updates. Check your current balance before making large purchases, especially if you’re carrying a higher balance than usual.

Setting up balance alerts can help. Many issuers allow you to configure notifications when your balance reaches a certain threshold—say, 75% of your limit.

Understand Pending Transactions

Your available credit reflects both posted transactions and pending authorizations. A purchase might not appear in your posted balance immediately, but it reduces your available credit right away.

Forgetting about pending transactions is a common way people accidentally exceed their limits.

Make Multiple Payments Per Month

You’re not restricted to one payment per billing cycle. Making payments throughout the month—especially before large purchases—keeps your balance lower and maintains better utilization.

Some cardholders on tight credit limits make weekly payments to ensure they have available credit when needed.

Request a Credit Limit Increase

Higher credit limits provide more cushion and automatically improve your credit utilization ratio (assuming your balance stays the same).

Card issuers periodically review accounts for automatic increases. You can also request an increase, though this typically triggers a hard credit inquiry that might temporarily affect your score.

Opt Out of Over-Limit Protection

If you haven’t already, consider declining over-limit coverage. This ensures transactions that would exceed your limit get declined rather than processed with fees attached.

While a declined transaction feels embarrassing in the moment, it’s far better than triggering fees and credit score damage.

| Prevention Strategy | Effectiveness | Implementation Difficulty |

|---|---|---|

| Balance monitoring apps | High | Easy |

| Automatic balance alerts | High | Easy |

| Multiple monthly payments | High | Moderate |

| Credit limit increase | Moderate | Moderate |

| Opt out of over-limit protection | High | Easy |

| Tracking pending transactions | Moderate | Moderate |

What to Do If You’ve Already Gone Over Your Limit

Okay, so what if you’ve already exceeded your limit? Here’s your recovery plan.

First, make a payment as quickly as possible to bring your balance back under your limit. Even a partial payment helps. The faster you reduce your balance, the less damage to your credit utilization and the fewer interest charges you’ll accrue.

Second, review your statement for over-limit fees. If you believe the fee was charged in error—perhaps you didn’t opt into over-limit protection—contact your card issuer immediately to dispute it.

Third, consider whether you actually need over-limit protection. If this situation happened because you opted in, you can revoke that consent at any time by contacting your issuer.

According to CFPB data, consumers paid about $2.5 billion less in overlimit fees than they paid in 2008. The opt-in requirement established by the CARD Act essentially eliminated over-limit fees as a major revenue source for issuers.

Frequently Asked Questions

If you’ve exceeded your limit, most issuers will decline additional transactions until you make a payment to bring your balance back under your limit. Even with over-limit protection, there’s no guarantee the issuer will approve transactions once you’re already above your limit.

There’s no standard amount. If you’ve opted into over-limit protection, issuers have discretion about whether to approve over-limit transactions and how far above your limit they’ll allow. Some may approve small amounts over, while others maintain stricter controls. Without opt-in protection, you cannot go over at all.

No. Credit utilization doesn’t have memory in scoring models. Once you pay down your balance and the lower utilization gets reported to credit bureaus (typically at your next statement closing date), your score can recover. However, if going over your limit led to missed payments or other negative items, those can remain on your report for years.

Yes. Card issuers can reduce credit limits based on their risk assessment, and repeatedly going over your limit might trigger such a review. They typically must provide notice before reducing your limit, though exceptions exist for accounts the issuer believes present significant risk.

No. Over-limit fees apply when your balance exceeds your credit limit (and you’ve opted into over-limit protection). Late payment fees apply when you don’t make at least the minimum payment by the due date. These are separate fees that can both appear on the same statement if you’ve triggered both situations.

Credit utilization updates typically occur when your issuer reports your balance to credit bureaus, usually at your statement closing date. If you pay down your balance before that reporting date, the high utilization might never appear on your credit report. If it does get reported, your score can recover within one to two billing cycles once lower utilization is reported.

Your credit limit is the maximum amount the issuer has authorized you to borrow. Your available credit is your limit minus your current balance (including pending transactions). For example, with a $5,000 limit and a $2,000 balance, you have $3,000 in available credit.

The Bottom Line

Going over your credit limit triggers a cascade of consequences—declined transactions, penalty fees, increased minimum payments, and potentially significant credit score damage through elevated utilization.

But wait. Federal protections under the CARD Act mean you won’t accidentally incur over-limit fees unless you’ve specifically opted into that coverage. For most cardholders, the worst outcome is a declined transaction.

The key is proactive management: monitor your balance, understand your available credit, set up alerts, and consider whether over-limit protection actually serves your interests. Most consumer advocates suggest declining this coverage, as a declined transaction causes far less harm than the fees and credit score impact of processing over-limit charges.

If you’ve already exceeded your limit, act quickly. Make a payment to bring your balance down, review any fees charged, and adjust your credit management strategies to prevent future occurrences. Your credit score can recover once you bring utilization back to healthy levels.