Quick Summary: Driving without insurance is illegal in nearly every U.S. state and carries serious consequences including fines ranging from $250 to $1,000, license suspension, vehicle impoundment, and personal liability for all damages in an accident. States use tiered penalty systems where consequences escalate with repeat offenses and longer insurance lapses. Beyond legal penalties, uninsured drivers face devastating financial risk—paying out-of-pocket for injuries, property damage, and legal costs that can easily reach hundreds of thousands of dollars.

Every driver knows they need car insurance. But what actually happens when you drive without it?

The consequences go far beyond a simple ticket. Driving uninsured puts you at risk for immediate legal penalties, crushing financial liability, and long-term complications that can follow you for years. According to the NAIC, everyone who owns a car should purchase auto insurance to cover property damage, medical bills, and legal costs—because without it, you’re personally responsible for every dollar.

Real talk: motor vehicle crashes cause significant societal harm, with one Congressional record valuing the cost at $836,000,000,000 annually. When uninsured drivers are involved, those costs get shifted to everyone else through higher premiums and uncompensated damages.

This guide breaks down exactly what happens if you’re caught driving without insurance, from state-by-state penalties to the financial devastation that follows an uninsured accident.

Why Auto Insurance Is Legally Required

States require auto insurance for one fundamental reason: financial protection. According to California’s DMV, insurance laws ensure that people who own or operate motor vehicles are financially able to provide monetary protection to those injured or having property damaged in accidents, regardless of fault.

Operating a vehicle is a privilege, not a right. That privilege comes with the responsibility to protect others from financial harm when accidents occur.

Here’s the thing though—insurance requirements aren’t just about protecting victims. They also protect the entire insurance system. The IIHS notes that insurance data represents more than 85% of the U.S. auto insurance market, and uninsured motorists create a ripple effect that increases costs for everyone.

Financial Responsibility Laws

Most states enforce what’s called financial responsibility laws. These laws require drivers to prove they can pay for damages they cause. For the vast majority of drivers, that proof comes through liability insurance.

Georgia’s Safety Responsibility Law, for example, aims to remove irresponsible drivers from highways and protect insured motorists from uninsured ones. If a driver fails to satisfy a claim for damage resulting from a crash, their license gets suspended until they can demonstrate financial responsibility.

Some states allow alternatives to traditional insurance—like cash bonds or certificates of deposit—but these options typically require substantial upfront capital that makes them impractical for most people.

Minimum Insurance Requirements by State

While nearly every state mandates auto insurance, the minimum coverage amounts vary significantly. Most states use a split-limit liability structure expressed in three numbers.

Take Nevada as an example. Drivers must carry minimum coverage of:

- $25,000 for bodily injury to one person

- $50,000 for bodily injury to two or more persons

- $20,000 for property damage

These minimums represent the floor, not the ceiling. Many experts suggest carrying higher limits since accidents frequently result in damages exceeding these amounts.

| Coverage Type | Nevada Minimum | What It Covers |

|---|---|---|

| Bodily Injury (per person) | $25,000 | Medical expenses, lost wages for one injured person |

| Bodily Injury (per accident) | $50,000 | Total coverage when multiple people are injured |

| Property Damage | $20,000 | Damage to other vehicles, structures, or property |

According to the California Department of Insurance, Good Drivers—those licensed for at least three consecutive years with no more than one point on their record—must receive rates at least 20% lower than non-Good Driver rates at the same company.

Immediate Consequences of Getting Caught Without Insurance

What happens when law enforcement discovers you’re driving uninsured? The consequences hit immediately and escalate quickly.

Traffic Stop Penalties

When pulled over, drivers must provide proof of insurance. Can’t produce it? The penalties kick in right away.

Nevada uses an offense-based tier system. According to NRS 485.187, first-offense penalties include:

- $250 to $1,000 fine (amount depends on how long you’ve been uninsured)

- A $250 reinstatement fee to restore vehicle registration

- Driver’s license suspension until proof of insurance is provided

- Vehicle registration suspension

- Possible vehicle impoundment

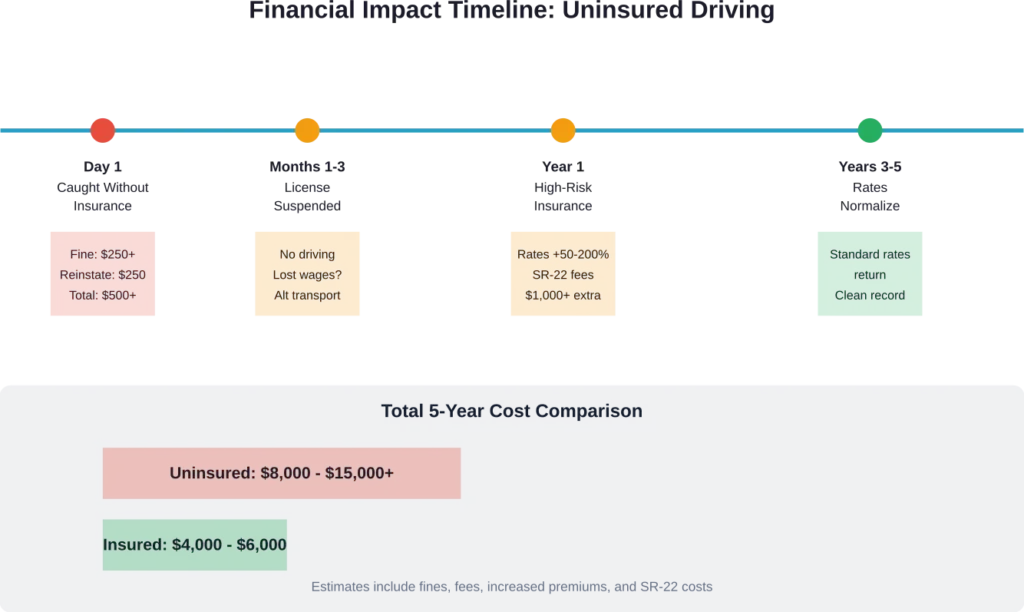

But wait. The fines increase based on how long you’ve gone without coverage. Even a one-day lapse can trigger fines up to $250. Longer lapses mean steeper penalties.

License and Registration Suspension

Most states suspend your driver’s license immediately when you’re caught without insurance. The suspension remains in effect until you provide proof of current insurance and pay all reinstatement fees.

According to Oregon’s DMV, driving during a period of suspension or revocation can result in additional criminal charges. Once any withdrawal action becomes effective, driving before reinstatement compounds the legal problems exponentially.

Your vehicle registration gets suspended too. That means your plates are invalid, and the vehicle legally cannot be operated on public roads until insurance is reinstated and registration fees are paid.

SR-22 Certificate Requirements

For insurance lapses exceeding 90 days, many states require an SR-22 certificate. This isn’t insurance itself—it’s a certificate of financial responsibility that your insurance company files with the state to prove you’re carrying coverage.

SR-22 requirements typically last for three years. During that time, any lapse in coverage gets reported immediately to the DMV, triggering new penalties. And SR-22 insurance costs significantly more than standard policies because insurers classify you as high-risk.

What Happens If You Have an Accident Without Insurance

Getting caught during a traffic stop is bad. Having an accident without insurance? That’s a financial catastrophe.

Personal Liability for All Damages

Without insurance, you’re personally liable for every dollar of damage you cause. According to the California DMV, if anyone is injured or vehicle damage exceeds $750, drivers must report the accident to the DMV within 10 days. Failure to report can result in license suspension.

But reporting is just the beginning. The real damage comes from the financial liability.

Medical expenses from serious injuries easily reach six figures. Property damage to multiple vehicles can cost tens of thousands. Then add legal fees, lost wages, pain and suffering claims, and potential punitive damages.

Sound familiar? This is why insurance exists—to protect drivers from financial ruin. Without it, victims can sue you directly and pursue your assets: bank accounts, property, wages, future earnings.

The Financial Reality of Uninsured Accidents

Let’s break down a typical scenario. You cause an accident that injures two people and damages three vehicles. The damages stack up fast:

| Expense Category | Typical Cost Range | Who Pays Without Insurance |

|---|---|---|

| Emergency medical treatment | $15,000 – $75,000 per person | You, personally |

| Vehicle repairs/replacement | $5,000 – $30,000 per vehicle | You, personally |

| Lost wages (injured parties) | $10,000 – $100,000+ | You, personally |

| Legal fees and court costs | $5,000 – $50,000 | You, personally |

| Pain and suffering claims | $20,000 – $500,000+ | You, personally |

Total liability can easily exceed $300,000 for a serious accident. Minimum insurance coverage would have protected you. Without it, you’re facing potential bankruptcy, wage garnishment, and property liens that can last for decades.

Criminal Charges and Legal Consequences

In some cases, driving without insurance after an accident can lead to criminal charges—not just civil liability. Leaving the scene of an accident (hit and run) carries felony charges in most states.

Even if you remain at the scene, you’ll face the administrative penalties: fines, license suspension, reinstatement fees, and mandatory SR-22 filing. But now those penalties come on top of massive civil liability.

State-Specific Tracking and Enforcement

How do states know when you’re driving without insurance? The enforcement mechanisms have become increasingly sophisticated.

Electronic Insurance Verification Systems

Many states now use electronic verification systems that allow law enforcement to check insurance status instantly during traffic stops. These databases receive real-time updates from insurance companies.

When your policy cancels or lapses, the insurance company notifies the state immediately. That notification triggers automatic suspension of your registration in many jurisdictions.

Nevada has been particularly aggressive with insurance tracking. The state receives continuous updates from insurers, making it extremely difficult to drive uninsured without detection.

Random Verification and Mail Notices

Some states conduct random insurance verification checks. If your vehicle registration is active but the state has no record of current insurance, you’ll receive a notice demanding proof of coverage within a specified timeframe.

Failure to respond results in automatic registration suspension. And once your registration is suspended, driving becomes illegal even if you later obtain insurance—until you complete the reinstatement process and pay all fees.

The Difference Between No Insurance and No Proof

Here’s an important distinction: being uninsured is not the same as failing to provide proof of insurance during a traffic stop.

If you have active insurance but simply forgot your insurance card, you can typically resolve the situation by providing proof to the court before your hearing date. Many jurisdictions will dismiss the citation entirely or reduce it to a minimal administrative fee.

But if you actually have no insurance coverage, providing proof becomes impossible. The penalties outlined above apply in full.

Some drivers think they can buy insurance after getting pulled over, then show proof to avoid penalties. That doesn’t work. Insurance companies report effective dates, and purchasing coverage after the violation date doesn’t satisfy the requirement for being insured at the time of the stop.

Long-Term Consequences of Driving Uninsured

The penalties don’t end once you pay your fines and reinstate your license. Driving without insurance creates long-term complications that can affect you for years.

Higher Insurance Premiums

When you eventually do get insurance—and you’ll need it to reinstate your license—expect to pay significantly higher premiums. Insurance companies view uninsured driving history as a major risk factor.

The premium increase can range from 30% to 200% higher than standard rates, depending on the length of your uninsured period and whether you had accidents or violations during that time.

These elevated rates typically persist for three to five years, meaning the financial impact extends far beyond the initial fine.

Limited Insurance Options

Many standard insurance carriers won’t accept drivers with recent uninsured driving on their record. You may be forced into high-risk insurance pools or specialty insurers that charge premium rates.

Some drivers find themselves in a catch-22: they can’t afford insurance, but they can’t drive legally without it, and they can’t get to work without driving.

Employment and Background Checks

License suspensions and driving violations appear on background checks. For jobs that require driving—from delivery drivers to sales positions—a suspended license or uninsured driving record can disqualify you from employment.

Even jobs that don’t require driving may view license suspensions negatively, particularly if the position involves responsibility, trustworthiness, or financial management.

Exceptions and Special Circumstances

A few situations create exceptions to standard insurance requirements, though they’re limited and specific.

Parked or Non-Operational Vehicles

Generally speaking, vehicles that are parked on private property and not being operated don’t require active insurance. However, if the vehicle is registered, many states still expect continuous coverage or will suspend the registration.

The safer approach? Surrender your license plates to the DMV if you’re not using the vehicle. This suspends the registration without penalty and eliminates the insurance requirement until you’re ready to drive again.

Military Deployment

Some states offer exemptions for military personnel deployed overseas. These exemptions typically require proper documentation and advance notification to the DMV.

New Hampshire’s Exception

New Hampshire is the only state that doesn’t require auto insurance for all drivers. However, drivers must still prove financial responsibility if involved in an accident, and most people find maintaining insurance far easier than demonstrating alternative financial capability.

How to Get Back on Track After Driving Uninsured

If you’ve been caught driving without insurance, taking immediate action minimizes the long-term damage.

Step 1: Purchase Insurance Immediately

The first step is obvious but critical: get insured right away. Even though purchasing insurance after the violation won’t retroactively eliminate penalties, it’s required for reinstatement and demonstrates responsibility.

Shop around despite your high-risk status. Some insurers specialize in high-risk drivers and offer more competitive rates than others. Get quotes from at least three companies.

Step 2: Complete All Court Requirements

Attend your court hearing or pay your citation as required. Ignoring court dates compounds your problems with additional charges and potential arrest warrants.

If fines create financial hardship, ask about payment plans. Many courts offer installment options that make penalties more manageable.

Step 3: File SR-22 If Required

For insurance lapses over 90 days or certain violations, you’ll need an SR-22 certificate. Contact your insurance company to file this—most insurers handle the process directly with the DMV.

SR-22 filing typically costs $15-$50, though the bigger expense comes from the elevated insurance premiums.

Step 4: Pay Reinstatement Fees

Once you have insurance (and SR-22 if required), pay all DMV reinstatement fees. These fees vary by state but typically range from $250 to $500 for first offenses.

Keep documentation of every payment. The reinstatement process can be slow, and having proof of payment helps resolve any administrative delays.

Step 5: Maintain Continuous Coverage

The most critical step: maintain continuous insurance coverage going forward. Any future lapse triggers immediate suspension and dramatically increases penalties for subsequent offenses.

Set up automatic payments through your bank to prevent accidental lapses. Even missing a payment by a few days can trigger DMV notification and suspension.

Preventing Uninsured Driving Situations

The best strategy is avoiding uninsured driving altogether. Here’s how to prevent coverage lapses:

Set Up Payment Reminders

Use automatic payments or calendar reminders to ensure premiums get paid on time. Most insurers offer grace periods of 10-30 days, but relying on grace periods risks administrative errors or notification delays.

Communicate With Your Insurer

If financial hardship makes payments difficult, contact your insurance company before your policy lapses. Many insurers offer payment plans, reduced coverage options, or temporary payment deferrals.

Downgrading to minimum coverage temporarily is better than having no coverage at all.

Consider Pay-Per-Mile Insurance

If cost is the primary barrier, look into usage-based or pay-per-mile insurance programs. These policies charge based on actual driving, making coverage more affordable for people who drive infrequently.

Understand Your State’s Requirements

Know exactly what your state requires for minimum coverage. According to the NAIC, understanding what insurance will cover and how to protect yourself is essential for all drivers. Don’t assume your current coverage meets requirements—verify it.

When Uninsured Drivers Cause Accidents

What happens when an uninsured driver hits you? The situation creates frustration and potential financial loss for victims.

Uninsured Motorist Coverage

This is why uninsured motorist (UM) coverage exists. UM coverage protects you when an at-fault driver has no insurance. It covers your medical expenses, lost wages, and property damage up to your policy limits.

Many states require insurers to offer UM coverage, and some make it mandatory. The IIHS notes that insurance claims provide valuable data showing how often uninsured motorist claims occur and their costs.

Pursuing Legal Action

Victims can sue uninsured drivers directly, but collecting judgments proves difficult. Many uninsured drivers lack assets to satisfy judgments, making lawsuits pyrrhic victories—you win in court but recover nothing.

Georgia’s Safety Responsibility Law allows claims to be filed against uninsured drivers, resulting in license suspensions until the driver satisfies the claim. But suspension doesn’t put money in victims’ pockets.

Frequently Asked Questions

Driving without insurance is typically a civil infraction, not a criminal offense, for a first violation. However, driving with a suspended license—which results from being caught uninsured—can lead to criminal charges and potential jail time. Multiple offenses or aggravating factors like accidents can also result in criminal prosecution in some states.

Even if you’re not at fault, you’ll still face penalties for driving without insurance: fines, license suspension, and reinstatement fees. For the accident itself, the at-fault driver’s insurance should cover your damages. However, your own lack of insurance may limit your ability to recover certain damages, and you still face all the administrative penalties for being uninsured.

Uninsured driving violations typically remain on your motor vehicle record for three to five years, depending on your state. Insurance companies can see these violations when calculating premiums, which is why rates remain elevated for several years after the violation. The suspension itself gets removed once you reinstate your license, but the violation history persists.

Yes, you can get insurance after being caught uninsured—in fact, you must get insurance to reinstate your license. However, expect to pay significantly higher premiums as a high-risk driver. You may need to shop with specialized high-risk insurers, and you’ll likely need to file an SR-22 certificate. The key is acting immediately to minimize the time you remain uninsured.

If cost is prohibitive, explore these options: contact your state insurance department about low-income programs, ask insurers about payment plans or reduced coverage options, consider pay-per-mile or usage-based insurance, look into public transportation alternatives, or temporarily surrender your plates rather than driving uninsured. Driving without insurance creates far greater long-term costs than any of these alternatives.

According to the NAIC, insurance typically follows the vehicle, not the driver. If someone else drives your car with your permission, your insurance generally covers accidents they cause. However, if an uninsured person drives your car and causes an accident, both the driver and the vehicle owner face legal and financial consequences. Always verify that anyone driving your vehicle has appropriate coverage.

Most states use electronic insurance verification systems that allow officers to check insurance status instantly through their patrol car computers. When you’re pulled over, the officer can see in real-time whether your vehicle has active insurance coverage. Insurance companies report policy status directly to state databases, making it nearly impossible to claim coverage that doesn’t exist.

Conclusion: The Real Cost of Going Uninsured

Driving without insurance isn’t just illegal—it’s financially catastrophic. The immediate penalties of fines up to $1,000, license suspension, and vehicle impoundment are only the beginning.

The real damage comes from the long-term consequences: years of elevated insurance premiums, limited carrier options, employment complications, and the devastating potential for personal bankruptcy if an accident occurs.

According to California’s Department of Insurance, accidents must be reported if anyone is injured or vehicle damage exceeds $750. When uninsured, you’re personally liable for every dollar of damage—medical expenses, property damage, lost wages, and legal costs that can easily exceed hundreds of thousands.

The math is simple: maintaining insurance costs far less than the cumulative penalties, increased premiums, and financial risk of driving uninsured. For the price of a few hundred dollars in monthly premiums, drivers protect themselves from financial ruin and legal consequences that can persist for years.

If cost is a barrier, explore payment plans, reduced coverage options, or usage-based insurance rather than gambling with no coverage. If you’re already facing penalties for uninsured driving, take immediate action: purchase insurance, complete all court requirements, file any required SR-22 certificates, and maintain continuous coverage going forward.

The privilege of driving comes with the responsibility of financial protection. Meeting that responsibility isn’t optional—it’s legally required, financially essential, and the only way to protect yourself from consequences that can follow you for years.

Need to reinstate your license or find affordable coverage? Contact your state’s DMV and insurance department for resources, payment plan options, and information about low-income insurance programs available in your area.