Quick Summary: Missing a car payment can result in late fees (often ranging between $25 and $50 per missed payment, though this varies by lender), credit score damage if you’re 30+ days late, and potential repossession if you fall 60-90 days behind. According to the Consumer Financial Protection Bureau, contacting your lender immediately when you anticipate payment trouble often opens up assistance options like payment deferrals or loan modifications that can prevent these consequences.

Life throws curveballs. A medical emergency, unexpected job loss, or even a simple oversight can leave you scrambling to cover your car payment. And when your vehicle is how you get to work, drop kids at school, or handle daily errands, the stakes feel incredibly high.

The reality? Missing a car payment sets off a chain of events that can impact your finances for months or even years. But it’s not an automatic disaster.

Understanding what happens at each stage—and what options exist—makes all the difference between a temporary setback and a financial crisis.

The Immediate Consequences of a Missed Car Payment

The moment a payment goes unpaid, the clock starts ticking. Most lenders don’t immediately panic, but the financial impact begins faster than many borrowers expect.

Grace Periods: The Brief Window

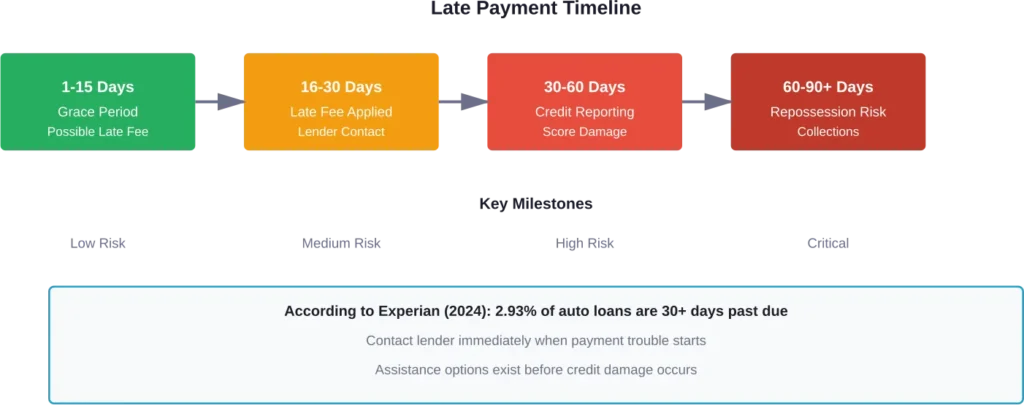

Some auto lenders offer a grace period—typically 10 to 15 days after the due date—during which late fees don’t apply. This isn’t universal, though. The terms live in your loan agreement, and not every lender provides this breathing room.

Even during a grace period, the payment is still considered late. It just means fees haven’t kicked in yet.

Late Fees Add Up Fast

Once the grace period expires (or immediately if there isn’t one), late fees hit. According to information from credit unions and lenders, late fees often range between $25 and $50 per missed payment, though this varies by lender.

That might not sound catastrophic. But here’s the thing—repeated late payments mean repeated fees. Missing three payments could add $75 to $150 to an already strained budget, making it even harder to catch up.

Credit Score Impact: When Late Payments Get Reported

Here’s where things get serious. Late payments don’t immediately appear on credit reports, but once they do, the damage can be substantial.

The 30-Day Mark

Lenders typically report late payments to credit bureaus once an account reaches 30 days past due. Before that threshold, the late payment is between borrower and lender.

Once reported, credit scores can drop significantly. The exact impact varies based on overall credit history and credit scoring model used, but a previously strong score may fall substantially from a single 30-day late payment, though the exact impact varies based on overall credit history and credit scoring model used.

According to the Consumer Financial Protection Bureau, these negative marks remain on credit reports and can affect borrowing ability for years. The impact diminishes over time, but recent late payments carry more weight than older ones.

Multiple Missed Payments

Each subsequent missed payment that crosses the 30-day threshold gets reported separately. A payment that’s 60 days late is worse than one that’s 30 days late. At 90 days, the damage intensifies further.

Community discussions reveal a common pattern: borrowers often underestimate how quickly one missed payment can snowball into three or four, each compounding the credit damage.

Repossession: When Lenders Take Your Vehicle

This is the scenario that keeps borrowers up at night. And the Federal Trade Commission is clear: lenders can repossess vehicles without going to court or providing advance notice in most states.

How Many Payments Before Repossession?

There’s no universal answer. Technically, missing just one payment can put a vehicle at risk of repossession if the loan agreement allows it. But in practice, most lenders don’t act that quickly.

Generally speaking, lenders typically wait until accounts are 60-90 days past due before repossessing vehicles, though this varies by lender and state law. Some lenders wait longer, especially if borrowers maintain communication and show good faith.

State laws and individual lender policies create significant variation. But waiting to find out isn’t a strategy—once repossession happens, options narrow dramatically.

What Happens After Repossession

The Consumer Financial Protection Bureau outlines the post-repossession process: lenders must sell repossessed vehicles in a “commercially reasonable manner.” The sale proceeds go toward the outstanding loan balance.

If the sale doesn’t cover what’s owed, borrowers remain responsible for the “deficiency balance”—the difference between the sale price and the loan amount, plus repossession and sale costs.

That’s right. Losing the car doesn’t necessarily mean the debt disappears.

| Days Past Due | Typical Consequences | Credit Impact | Repossession Risk |

|---|---|---|---|

| 1-15 Days | Grace period (if offered); possible late fee | None yet | Very Low |

| 16-29 Days | Late fee applied; lender contact begins | None yet | Low |

| 30-59 Days | Credit bureau reporting; additional fees | Significant drop | Moderate |

| 60-89 Days | Serious delinquency; collection calls | Major damage | High |

| 90+ Days | Imminent repossession; possible default | Severe damage | Very High |

What to Do When Payment Trouble Starts

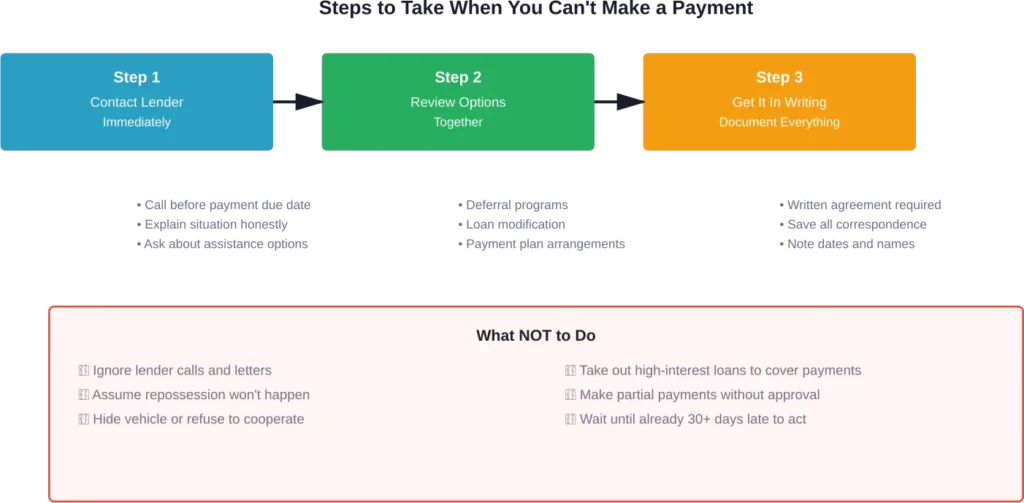

The Consumer Financial Protection Bureau emphasizes one critical step: contact the lender or servicer immediately when payment problems emerge.

Contacting the lender is a critical step that can help borrowers access available assistance options.

Assistance Options Lenders May Offer

According to government consumer resources, lenders may provide several assistance options for borrowers experiencing temporary financial hardship:

- Payment deferral: Postponing one or more payments to the end of the loan term

- Loan modification: Adjusting loan terms to reduce monthly payment amounts

- Refinancing: Restructuring the loan with different terms or interest rates

- Forbearance: Temporarily reducing or suspending payments during hardship periods

These options aren’t guaranteed, and availability varies by lender and circumstance. But they’re rarely available to borrowers who avoid contact and simply stop paying.

Document Everything

When communicating with lenders about payment difficulties, keep records of every conversation. Note dates, times, representative names, and what was discussed or agreed upon.

If assistance is offered, get it in writing before assuming the arrangement is official.

Preventing Future Payment Problems

Once the immediate crisis is handled, the focus shifts to preventing recurrence.

Budget Adjustment

Real talk: if car payments consistently strain the budget, something needs to change. That might mean cutting other expenses, finding additional income, or acknowledging the vehicle is beyond current financial means.

Financial counselors at organizations like the National Foundation for Credit Counseling can help create realistic budgets and identify sustainable solutions.

Automatic Payments

For borrowers who miss payments due to simple oversight rather than cash flow problems, automatic payments eliminate that risk. Most lenders offer automatic withdrawal from checking accounts on specified dates.

The downside? Insufficient funds can trigger overdraft fees on top of late payment fees, creating a worse situation. Automatic payments work best when paired with consistent cash flow monitoring.

Emergency Fund Priority

The unexpected happens. Car repairs, medical bills, temporary income loss—these aren’t unusual events. They’re predictable unpredictabilities.

Building even a small emergency fund (starting with $500-$1,000) creates breathing room when expenses spike or income dips temporarily.

Understanding Your Rights

The Federal Trade Commission and Consumer Financial Protection Bureau outline important protections for borrowers facing repossession or payment difficulties.

Lenders must conduct lawful repossessions. They can’t “breach the peace”—meaning they can’t use physical force, threats, or enter locked garages without permission.

Borrowers are entitled to notification about how and when a repossessed vehicle will be sold. If the sale creates a deficiency balance, notification must include the amount owed and the right to an accounting of how it was calculated.

Some states offer “reinstatement” rights—allowing borrowers to get vehicles back by paying overdue amounts plus fees before the car is sold. Other states provide “redemption” rights—the option to buy back the vehicle by paying the full loan balance.

These rights vary significantly by state. Understanding local laws matters when navigating payment problems.

Frequently Asked Questions

Credit reporting typically begins at 30 days past due. Late payments before that threshold usually don’t appear on credit reports, though late fees and lender contact will still occur. Once reported, the exact impact varies based on overall credit history and credit scoring model used.

Depending on state law, two options may exist. Reinstatement allows getting the vehicle back by paying overdue amounts plus repossession costs. Redemption requires paying the entire loan balance. The Consumer Financial Protection Bureau notes these rights vary by state and must be exercised before the lender sells the vehicle.

According to the Consumer Financial Protection Bureau, many lenders offer assistance options—including payment deferrals, loan modifications, or forbearance—for borrowers experiencing temporary financial hardship. These options aren’t guaranteed, but lenders are more likely to work with borrowers who communicate proactively rather than simply stopping payment.

Partial payments may not be accepted or applied to the account unless the lender agrees in advance. Some lenders hold partial payments in a suspense account without applying them to the loan balance, meaning the account continues accruing late fees and moving toward delinquency. Always confirm with the lender how partial payments will be handled.

Technically, even one missed payment can trigger repossession rights under most loan agreements. In practice, lenders typically wait until accounts are 60-90 days past due before repossessing vehicles. However, this varies significantly by lender policy and state law—waiting to find out isn’t advisable.

Yes. Late payments remain on credit reports and can impact borrowing ability for years, though the effect diminishes over time. Recent late payments carry more weight than older ones. Lenders reviewing future applications will see the payment history, potentially resulting in higher interest rates or loan denials.

Contact the lender immediately to explain the situation. The National Foundation for Credit Counseling notes that temporary financial burdens—including job loss—are common reasons for payment difficulties, and lenders may offer forbearance or modified payment plans during unemployment periods. Additionally, review the loan agreement for any unemployment protection provisions.

Moving Forward After a Missed Payment

Missing a car payment isn’t ideal. But it’s also not uncommon—data from Experian shows 2.93% of auto loans are 30+ days past due, meaning thousands of borrowers face this situation.

The difference between a temporary setback and a long-term financial problem often comes down to action. Lenders have more flexibility and willingness to help borrowers who communicate early, honestly, and consistently.

Ignoring the problem doesn’t make it disappear. It just narrows the options and accelerates the consequences.

If payment trouble is on the horizon—or already here—contact the lender today. Not next week. Not after missing another payment. Today.

Most lenders would rather work out a solution than repossess a vehicle. But that willingness has limits, and those limits shrink with each day of silence.