Quick Summary: Yes, buying a house with bad credit is possible through government-backed programs like FHA loans, which accept credit scores as low as 500 with a 10% down payment. Alternative financing options include USDA loans, VA loans for veterans, and working with specialized lenders who consider factors beyond credit scores. Improving your credit score, increasing your down payment, and reducing debt-to-income ratio significantly improve approval chances.

Bad credit feels like a locked door between you and homeownership. But here’s the thing—that door isn’t actually locked. It just requires a different key.

According to the Consumer Financial Protection Bureau, more than 45 million American adults have no credit score because they have limited or no credit history. And millions more are rebuilding after financial setbacks. If you’re worried your credit history disqualifies you from buying a home, you’re not alone—and you have more options than you might think.

The path to homeownership with less-than-perfect credit isn’t identical to the traditional route. It requires understanding which loan programs work with lower credit scores, what lenders actually look for beyond that three-digit number, and how to position yourself as the strongest possible borrower.

What Credit Score Is Considered ‘Bad’ for Buying a House?

Before exploring solutions, it helps to understand where you stand. Credit scores range from 300 to 850, and mortgage lenders categorize these numbers differently than you might expect.

According to the Consumer Financial Protection Bureau’s borrower risk profiles based on FICO® Score 8, credit scores are categorized as follows:

| Credit Score Range | Classification |

|---|---|

| 300-579 | Deep Subprime (Poor) |

| 580-619 | Subprime |

| 620-659 | Near-Prime |

| 660-719 | Prime |

| 720-850 | Super-Prime |

Most conventional mortgage lenders prefer scores above 620. But that doesn’t mean scores below this threshold lock you out.

Different loan programs have different thresholds. What one lender considers too risky, another program explicitly accommodates. The Federal Housing Administration exists specifically to help people with lower credit scores access homeownership.

Can You Actually Buy a House with Bad Credit?

The short answer? Absolutely.

According to HUD.gov, FHA loans have been helping people become homeowners since 1934. The program exists specifically for borrowers who can’t meet conventional lending standards. The Federal Housing Administration insures these loans, allowing lenders to offer better terms to borrowers with lower credit scores.

Real people with credit scores in the 500s and 600s buy homes every year. Borrowers with past financial difficulties have successfully purchased homes after taking steps to improve their financial position.

But there’s no magic here. Lower credit scores typically mean higher interest rates, larger down payments, or both. The question isn’t whether you can buy a house with bad credit—it’s which path makes the most sense for your situation.

Government-Backed Loan Programs for Bad Credit

Several government programs specifically accommodate borrowers with lower credit scores. These programs exist because access to homeownership strengthens communities and the economy.

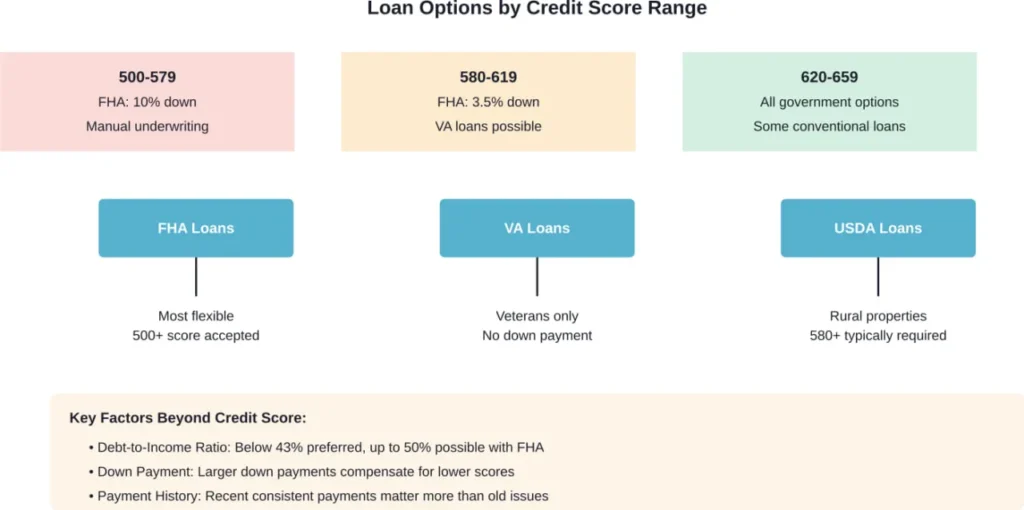

FHA Loans: The Most Accessible Option

FHA loans represent the most common path for borrowers with bad credit. According to HUD, these loans offer low down payments, low closing costs, and easy credit qualifying.

Here’s what makes FHA loans work for bad credit:

- Minimum credit score of 580 with 3.5% down payment (as offered by Rocket Mortgage; other lenders may have different requirements)

- Credit scores between 500-579 may be accepted with 10% down payment (varies by lender)

- More flexible debt-to-income ratio requirements

- Consideration of payment history beyond credit scores

Some lenders, including Rocket Mortgage, require a 580 minimum score for FHA loans. Other lenders work with scores as low as 500. The specific requirements vary by lender, so shopping around matters.

Many lenders assess debt-to-income ratios with FHA loans allowing flexibility in certain cases, compared to conventional loan standards.

VA Loans for Veterans

Veterans and active military members have access to VA loans, which don’t have a minimum credit score requirement set by the Department of Veterans Affairs. Individual lenders set their own minimums, often around 580-620.

VA loans offer benefits including zero down payment options. For eligible borrowers with lower credit scores, VA loans often provide better terms than FHA alternatives.

USDA Loans for Rural Properties

USDA loans serve rural and suburban homebuyers. While USDA doesn’t set a minimum credit score requirement, individual lenders establish their own minimums.

These loans offer zero down payment options, making them powerful for borrowers with limited savings but steady income.

What Lenders Actually Look For Beyond Your Credit Score

Credit scores matter, but they don’t tell the whole story. Mortgage underwriters evaluate multiple factors when assessing loan applications.

Debt-to-Income Ratio

Your debt-to-income (DTI) ratio compares monthly debt payments to gross monthly income. Most lenders prefer DTI below 43%, though FHA loans can accommodate up to 50% with strong compensating factors.

Calculate DTI by dividing total monthly debt obligations (including the proposed mortgage payment) by gross monthly income. Someone earning $5,000 monthly with $1,500 in debt payments has a 30% DTI—well within acceptable ranges.

Employment History and Income Stability

Lenders want to see steady employment, typically at least two years in the same field. Consistent income matters more than high income. A borrower earning $50,000 annually with three years at the same employer looks more stable than someone earning $80,000 but switching jobs every six months.

Down Payment Size

Larger down payments reduce lender risk and improve approval odds. According to the Consumer Financial Protection Bureau, keeping credit utilization below 30% demonstrates financial responsibility—and the same principle applies to home equity.

A 10% down payment shows significantly more commitment than 3.5%. For borrowers with credit scores in the 500-579 range, that 10% down payment isn’t just recommended for FHA loans—it’s required.

Payment History and Recent Credit Behavior

Recent payment patterns matter more than old mistakes. Lenders look at the last 12-24 months most closely. A borrower who had collections three years ago but has made every payment on time since demonstrates recovery. Someone with late payments last month raises immediate red flags.

Research from the Minneapolis Federal Reserve highlights that repayment patterns can be influenced by factors beyond what traditional credit scores capture, including hometown influences and family financial behaviors. This suggests lenders increasingly recognize that credit scores alone don’t predict future payment behavior.

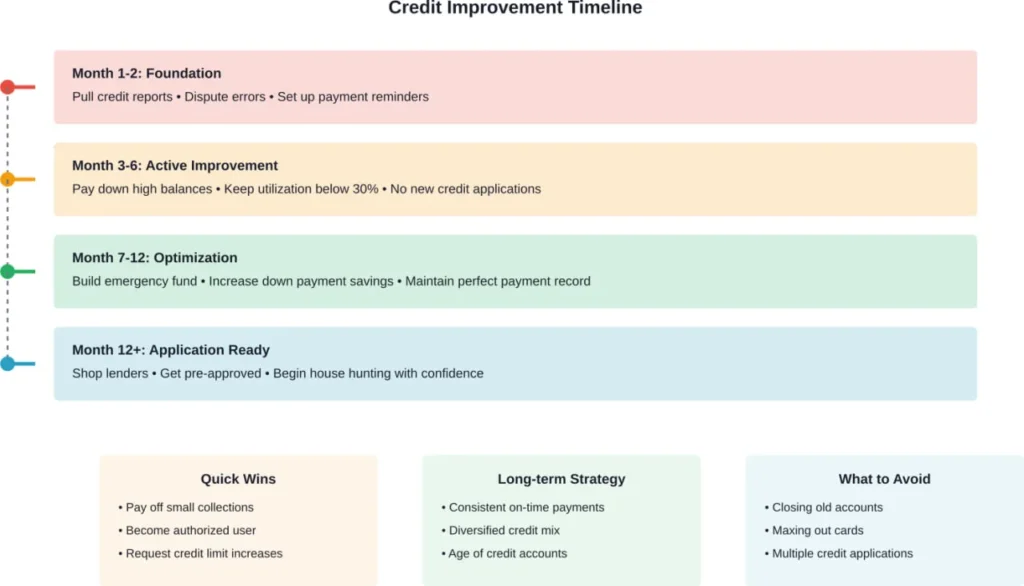

Steps to Improve Your Chances of Approval

Getting approved with bad credit requires strategic preparation. These steps improve both approval odds and loan terms.

Check Your Credit Reports for Errors

According to the Federal Trade Commission, consumers can check their credit reports for free at annualcreditreport.com. The Consumer Financial Protection Bureau emphasizes that consumers want credit reports to be accurate because they affect borrowing ability and costs.

Dispute any errors found. Collections that don’t belong to you, accounts reporting incorrect balances, or late payments you made on time—all these can be corrected through the dispute process outlined by the Fair Credit Reporting Act.

Pay Down Existing Debt

Reducing credit card balances improves both credit scores and DTI ratios. According to the Consumer Financial Protection Bureau, experts advise keeping your use of credit at no more than 30 percent of your total credit limit. For example, if your credit limit is $1,000, you’d want to limit your use to $300 or less.

Avoid New Credit Applications

Each credit application generates a hard inquiry that temporarily lowers credit scores. Multiple applications signal financial stress to lenders.

Focus on existing accounts. Make payments on time. Don’t open new credit cards or take out new loans during the months leading up to mortgage application.

Build a Larger Down Payment

Every dollar saved for down payment improves loan terms and approval odds. Consider these strategies:

- Set up automatic transfers to a dedicated savings account

- Use windfalls like tax refunds or bonuses entirely for down payment

- Explore down payment assistance programs in your state or county

- Consider gift funds from family members (allowed by most loan programs)

That larger down payment might mean waiting six more months. But the difference between 3.5% and 10% down could mean the difference between approval and rejection.

Get Pre-Approved Before House Hunting

Pre-approval provides a realistic budget and shows sellers you’re serious. The pre-approval process involves actual underwriting review of income, assets, and credit—not just the preliminary pre-qualification many online calculators provide.

Shop multiple lenders. One might offer FHA loans starting at 580 while another works with scores as low as 500. Rate and fee structures vary significantly, and comparing at least three lenders often saves thousands over the loan term.

Alternative Financing Options

Traditional mortgages aren’t the only path. Several alternatives work for borrowers with credit challenges.

Owner Financing

Some sellers finance the purchase directly, essentially acting as the lender. This arrangement bypasses traditional mortgage underwriting entirely.

Owner financing typically involves higher interest rates and shorter terms (often 5-10 years with a balloon payment). But it allows purchase when traditional financing isn’t available. Sellers willing to finance are often those with paid-off homes who want steady monthly income.

Rent-to-Own Agreements

Rent-to-own (lease-option) agreements allow renting with an option to purchase later. A portion of rent payments typically credit toward the eventual down payment.

These arrangements provide time to improve credit while locking in a purchase price. The downside? Monthly payments often exceed standard rent, and failing to complete the purchase forfeits accumulated credits.

Co-Signers

A co-signer with good credit strengthens applications. The co-signer assumes equal responsibility for the loan, and the lender evaluates their credit and income alongside the primary borrower’s.

Co-signing carries serious risk for the co-signer. Missing payments damages their credit equally. This option works best with trusted family members who understand the commitment.

Credit Unions and Community Banks

Smaller local lenders often provide more flexibility than large national banks. Credit unions, in particular, sometimes consider factors like local employment, community ties, and personal circumstances that automated underwriting systems miss.

These lenders may offer portfolio loans kept on their own books rather than sold to secondary markets. Portfolio loans follow the lender’s own guidelines, not government or investor standards.

The True Cost of Bad Credit Mortgages

Bad credit doesn’t just affect approval—it affects price. Interest rates for borrowers with lower credit scores run significantly higher than rates for those with excellent credit.

Interest rate differences significantly impact total loan cost.

The following table shows estimated rates for borrowers with different credit score ranges:

| Credit Score | Estimated Rate Range | Monthly Payment (30-year, $250K) |

|---|---|---|

| 760+ | 6.5%-7.0% | Approx. $1,580-$1,663 |

| 660-679 | 7.0%-7.5% | Approx. $1,663-$1,748 |

| 620-639 | 7.5%-8.0% | Approx. $1,748-$1,834 |

| 580-619 | 8.0%+ | Approx. $1,834+ |

These numbers illustrate why improving credit before applying—even waiting six months to raise scores from 590 to 640—can save thousands of dollars.

FHA loans require mortgage insurance. FHA mortgage insurance includes both upfront premiums and annual premiums that may continue based on down payment amount and loan duration.

Special Circumstances: Bankruptcy and Foreclosure

Bankruptcy and foreclosure create significant credit damage, but they don’t permanently prevent homeownership.

Waiting Periods After Bankruptcy

Waiting periods after bankruptcy vary by loan program. Different programs establish different requirements, so consulting with lenders about specific timelines is important.

Rebuilding After Foreclosure

Waiting periods for FHA, conventional, and VA loans after foreclosure vary. During these waiting periods, focus on rebuilding credit. Secured credit cards, credit-builder loans, and becoming an authorized user on someone else’s account all help establish positive payment history.

Common Mistakes to Avoid

Several missteps sabotage mortgage applications for borrowers with bad credit.

Taking on new debt right before applying. That new car loan or furniture financing drops credit scores and increases DTI. Wait until after mortgage closing for major purchases.

Closing old credit accounts. Closing accounts reduces available credit and shortens average credit age—both hurt scores. Keep old accounts open even if not actively used.

Job changes during the application process. Lenders verify employment right before closing. Switching jobs mid-process can derail approval. Wait until after closing to make career moves unless absolutely necessary.

Making large deposits without documentation. Unexplained large deposits raise money laundering concerns. Document all deposits over $500 with clear paper trails.

Ignoring pre-approval feedback. If a lender says waiting three months to pay down debt would significantly improve terms, listen. The rush to buy immediately often costs far more than patience would.

Working with the Right Lender

Not all lenders handle bad credit applications equally. Some specialize in challenging credit situations while others focus on prime borrowers.

Look for lenders who:

- Explicitly advertise FHA, VA, or USDA loan programs

- Mention minimum credit scores in the 500-600 range

- Offer manual underwriting (human review rather than just automated systems)

- Provide free consultations to discuss specific situations

Ask direct questions during initial consultations. What’s the lowest credit score they’ve recently approved? What compensating factors do they value most? Do they keep loans in portfolio or sell them?

Mortgage brokers sometimes access more lender options than applying directly. Brokers work with multiple lenders and can shop applications to those most likely to approve challenging credit situations.

Frequently Asked Questions

The lowest credit score that can qualify for a mortgage is 500 through the FHA loan program. However, a 500-579 credit score requires a 10% down payment. Credit scores of 580 or higher qualify for FHA loans with just 3.5% down. Keep in mind that individual lenders may set higher minimums than program requirements, so the effective minimum varies by lender.

Yes, a 550 credit score can qualify for an FHA loan with 10% down payment. However, approval depends on additional factors including income stability, debt-to-income ratio, and payment history. Borrowers at this credit level should expect higher interest rates and stricter scrutiny of compensating factors like employment history and savings.

Down payment requirements with bad credit depend on the loan program and specific credit score. FHA loans require 3.5% down with credit scores of 580 or higher, or 10% down with scores between 500-579. Some lenders may require larger down payments for very low credit scores. Generally, larger down payments improve approval odds and may result in better interest rates.

Credit improvement timelines vary based on starting point and specific issues. According to the Consumer Financial Protection Bureau, keeping credit utilization below 30% and making consistent on-time payments represent the most impactful actions. Most borrowers see meaningful score improvements within 6-12 months of consistent positive behavior. Severe issues like bankruptcy or foreclosure require statutory waiting periods of 1-7 years depending on loan type.

Paying off collections can help, but the impact varies. Recent collections hurt scores more than old ones. Paying a collection doesn’t remove it from credit reports, though it changes the status to “paid.” Some scoring models don’t distinguish between paid and unpaid collections, while newer models treat paid collections more favorably. Focus on payment patterns over the past 12-24 months—lenders weigh recent behavior most heavily.

Yes, according to the Consumer Financial Protection Bureau, more than 45 million American adults have no credit score due to limited credit history, but homeownership remains possible. Manual underwriting allows lenders to evaluate alternative credit data like rent payments, utility bills, and insurance payments. FHA loans explicitly accommodate borrowers with limited credit history through manual underwriting. The process requires more documentation but provides a path for those without traditional credit profiles.

Bad credit doesn’t limit which specific houses are available, but it affects how much lenders will approve for financing. Lower credit scores typically result in smaller maximum loan amounts due to higher interest rates increasing monthly payments relative to income. Bad credit also affects down payment requirements and available loan programs, which can limit price range. The property itself must still meet lender requirements for condition and appraisal value regardless of credit score.

Taking Action: Your Next Steps

Buying a house with bad credit requires strategy, not miracles. Start by understanding exactly where you stand.

Pull credit reports from all three bureaus. Calculate current DTI ratio. Research programs and lenders that work with your credit profile. Then create a timeline.

For scores below 580, plan for that 10% FHA down payment and focus on bringing scores above 580 to access the 3.5% option. For scores in the 580-620 range, work on reaching 620 to access conventional loan options with potentially better terms.

Every month of preparation improves outcomes. Pay bills on time. Reduce balances. Build savings. These fundamentals work regardless of where credit stands today.

The path to homeownership with bad credit exists. It’s not always fast, and it’s not always cheap. But it’s real, it’s documented, and thousands of borrowers walk it successfully every year.

Bad credit closed one door. But as the Federal Housing Administration has demonstrated since 1934, other doors remain open for those willing to find them.

Start where you are. Use what you have. Take the first step today—whether that’s pulling credit reports, researching FHA lenders, or setting up an automatic transfer to a down payment savings account. Homeownership with bad credit isn’t about perfect credit. It’s about perfect persistence.