Quick Summary: Yes, a perfect 850 credit score is possible, though rare—only 1.76% of Americans achieved it as of March 2025. While this elite status requires years of flawless financial behavior, including on-time payments and low credit utilization, any score above 800 delivers virtually identical benefits from lenders.

The idea of a perfect credit score feels almost mythical. Like getting a hole-in-one or bowling a perfect game, hitting 850 sounds impressive but impossibly rare.

Here’s the reality: perfect credit scores do exist. Real people achieve them. But the question isn’t just whether it’s possible—it’s whether chasing that perfect number makes any practical sense for your financial life.

According to the Consumer Financial Protection Bureau, credit scores predict how likely someone is to pay back loans on time based on credit report information. Companies use these scores to decide whether to extend credit and at what interest rates.

What Exactly Is a Perfect Credit Score?

Both major credit scoring models—FICO and VantageScore—use 850 as their highest possible number. This represents the absolute peak of creditworthiness in the eyes of lenders.

But here’s where it gets interesting. Not all credit scores use the same scale.

The standard FICO Score range runs from 300 to 850. VantageScore operates on the same scale. These are the two primary models lenders actually use when evaluating applications.

According to FICO, people with no debt can—and often do—have credit scores higher than the national average. According to FICO analysis of April 2023 data, the average FICO Score for people with no current debt was 737, which is almost 20 points higher than the national average of 718., debunking the myth that carrying debt improves credit standing.

How Many People Actually Have Perfect Credit?

As of March 2025, 1.76% of U.S. consumers had a FICO Score of 850, according to Experian data. That translates to roughly 3 million Americans.

The percentage has fluctuated slightly over recent years. According to American Express data from 2023, 1.54% of all credit-holding Americans had a FICO score of 850., indicating a small uptick in perfect scores.

These numbers reveal something important: perfect credit is exceptionally rare but not impossible. You’re more likely to meet someone with an 850 score than someone who’s been struck by lightning, but it’s still a remarkably exclusive club.

FICO research points to a trend showing the average credit score in the U.S. has been gradually increasing since the great recession of the mid to late 2000s. Factors contributing to this rise include a decrease in negative information on credit reports in recent periods.

The Profile of Perfect Credit Score Holders

What separates the 850 club from everyone else? Experian’s analysis reveals several consistent patterns among those who’ve achieved perfection.

These consumers maintain an average of 5.7 credit cards, significantly higher than the 3.7 cards held by typical consumers. More available credit means better utilization ratios when managed responsibly.

Their credit card balances tell an interesting story. Perfect scorers carry an average balance of $3,028, compared to $6,618 for all consumers. Retail card balances show an even starker contrast—just $188 versus $1,180.

Payment history remains spotless across the board. According to FICO, payment history comprises 35% of score calculations, making it the single most important factor. For perfect scorers, this means consistently making on-time payments with no late payment history.

| Metric | All Consumers | 850 Score Holders |

|---|---|---|

| Average FICO Score | 714 | 850 |

| Credit Card Balance | $6,618 | $3,028 |

| Retail Card Balance | $1,180 | $188 |

| Number of Credit Cards | 3.7 | 5.7 |

| Credit Utilization | Higher | Lower |

Credit age matters enormously. Those with perfect scores typically have credit histories spanning decades, not years. Newer accounts pull down average age, which explains why young adults almost never achieve 850 scores regardless of financial behavior.

What Actually Determines Your Credit Score

The Federal Reserve has studied credit scoring extensively, noting that payment history cannot be justified solely by business necessity without considering predictive value and less discriminatory alternatives.

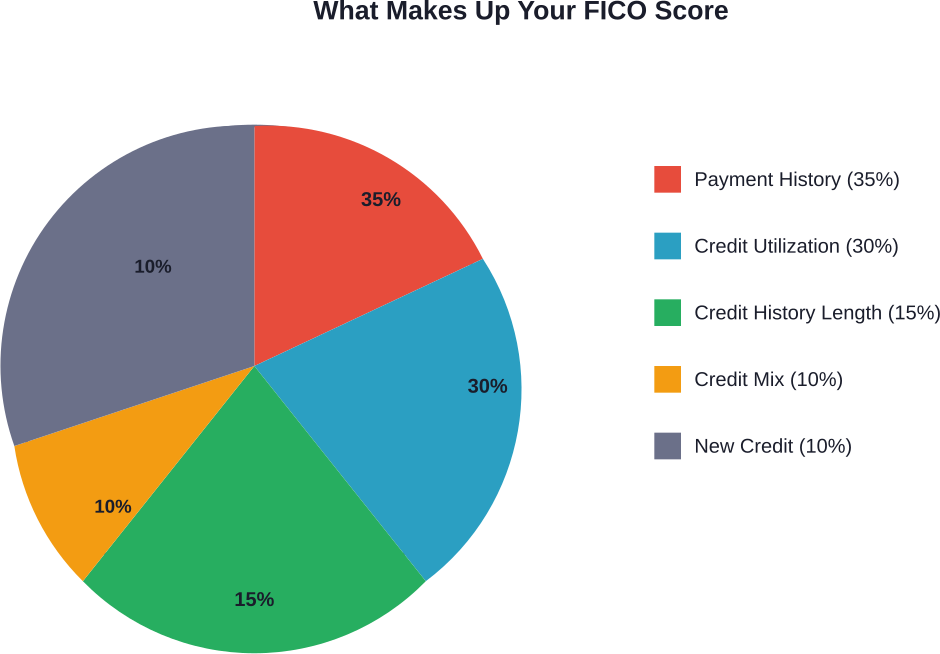

FICO breaks down score calculation into five weighted categories:

Payment History (35%): This single factor carries more weight than anything else. Late payments, collections, bankruptcies, and foreclosures devastate scores. Perfect scorers never miss payments—not once in seven years minimum.

Credit Utilization (30%): This measures how much available credit gets used. Keeping balances below 10% of limits correlates strongly with higher scores. Perfect scorers often maintain utilization in the single digits.

Length of Credit History (15%): Average age of accounts matters. Closing old cards shortens history and can lower scores, contrary to what many assume.

Credit Mix (10%): Having different account types—credit cards, installment loans, mortgages—demonstrates ability to manage various credit forms.

New Credit (10%): Recent applications and newly opened accounts. Multiple hard inquiries in short periods signal risk to lenders.

VantageScore weights factors slightly differently, with payment history at 41% and utilization also playing a major role. Both models prioritize the same behaviors even if their formulas differ.

Does a Perfect Score Actually Matter?

Real talk: probably not as much as you’d think.

Lenders treat scores above 800 essentially identically. Someone with an 805 gets the same loan terms, interest rates, and approval odds as someone with 850. Both fall into the “exceptional” category where risk is minimal.

The benefits of excellent credit kick in well before perfection. Interest rate tiers typically max out around 760-780 for most loan products. Mortgage lenders, auto financiers, and credit card issuers reserve their best rates for this tier and above.

A perfect score offers bragging rights more than tangible financial advantages. It’s an achievement worth feeling proud of, but chasing those final points from 820 to 850 delivers diminishing returns.

That said, maintaining behaviors that lead toward perfection—low utilization, consistent payments, diverse accounts—absolutely matters. The habits create the score; the score just reflects the habits.

How to Build Toward Excellent Credit

Getting to 850 requires decades of perfect behavior. Getting to 800? That’s achievable with disciplined financial management over several years.

Never miss a payment. Set up automatic payments for at least minimums on every account. Payment history comprises 35% of your FICO score.

Keep utilization low. Aim for under 10% on credit cards, even if paying balances in full monthly. High utilization hurts scores even when paid off before interest accrues.

Don’t close old accounts. That dormant card from college? Keep it open with an occasional small charge. Closing it shortens your credit history and reduces available credit.

Limit new credit applications. Each hard inquiry dings scores slightly. Multiple applications in short periods compound the effect.

Diversify credit types. A mix of revolving credit (cards) and installment loans (auto, mortgage, personal loans) demonstrates broader credit management skills.

Monitor credit reports regularly. According to the Consumer Financial Protection Bureau, credit scores affect ability to get loans, jobs, housing, insurance, and more. Errors happen, and disputing inaccuracies early prevents score damage.

Time remains the one factor that can’t be rushed. Building a decade-plus credit history simply requires waiting. Starting young gives a significant advantage.

The Geographic Factor

Interestingly, perfect credit scores cluster geographically. Certain states and metropolitan areas show higher concentrations of 850 achievers.

FICO data analyzing top metropolitan statistical areas showed substantial decreases over a 10-year period in the percentage of population having recent delinquencies. Since payment history comprises 35% of score calculation, this has significant impact on overall score distributions by region.

Economic stability, higher education levels, and regional financial literacy programs likely contribute to these geographic patterns, though correlation doesn’t prove causation.

Common Myths About Perfect Credit

Several misconceptions persist about achieving 850 scores.

Myth: You need to carry credit card balances. False. According to FICO analysis, people with no debt can and do achieve high credit scores. Paying cards in full monthly is financially smarter and doesn’t hurt scores.

Myth: Closing unused cards improves scores. Actually the opposite. FICO’s ‘Score a Better Future’ educational events found that a sizable percentage of participants incorrectly assumed closing inactive cards would increase scores. In reality, this action typically lowers scores.

Myth: Checking your own credit hurts your score. Soft inquiries from self-checks don’t affect scores. Only hard inquiries from lender applications impact scores temporarily.

Myth: Income affects credit scores. Credit scoring models don’t consider income, employment, demographics, or beliefs according to the scoring methodology.

When to Stop Chasing Perfection

If your score sits anywhere above 800, focus energy elsewhere. The marginal benefit of those last points doesn’t justify obsessive monitoring.

Perfect scores can actually fluctuate. FICO data gets updated constantly—payments reported today affect scores immediately. Normal credit activity like opening necessary accounts or temporary utilization spikes will move scores around.

Someone at 850 might drop to 840 next month from normal credit use, then bounce back. This volatility at the top doesn’t matter for practical purposes.

Better to maintain excellent habits and let the score take care of itself than to contort financial decisions solely to chase a number that provides no additional benefit.

Frequently Asked Questions

Achieving 850 requires sustained perfect credit behavior over many years, as credit history length is a significant factor in score calculations. Younger consumers rarely hit 850 simply because credit age weighs into calculations. Building excellent credit scores requires disciplined financial management over several years.

Yes. FICO research confirms that individuals with zero account balances often maintain excellent credit scores. You don’t need to carry debt or pay credit card interest to build credit. Using cards and paying balances in full monthly demonstrates responsible usage without incurring debt.

The average FICO Score sits around 714 for all consumers. Approximately 20% of Americans have scores in the exceptional range (800-850), while 25% fall in the very good category (740-799). About 16% have poor credit below 580.

A single late payment reported to credit bureaus can significantly impact a perfect score, though the exact impact depends on circumstances and payment history context. However, scores above 800 remain in the exceptional category even after moderate drops. The payment will affect scores for seven years, though its impact diminishes over time with continued good behavior.

Not typically. Interest rate tiers typically max out around 760-780 for most loan products. Someone with 850 gets the same loan terms as someone with 800 or even 780 in most cases. Both demonstrate minimal lending risk, so lenders don’t differentiate further.

All three major bureaus—Experian, Equifax, and TransUnion—can report 850 FICO Scores, though your score may differ slightly across bureaus depending on what information each has. Lenders often check just one bureau, so having 850 across all three isn’t necessary for loan approvals.

Eventually, but not immediately. Paid collections remain on credit reports for seven years from the original delinquency date. While paying them helps and newer scoring models treat paid collections more favorably, reaching 850 requires those entries to age off reports entirely. Focus first on reaching 800, which offers identical benefits.

The Bottom Line on Perfect Credit

Perfect 850 credit scores exist—1.76% of Americans prove it’s possible. But chasing perfection misses the point.

Credit scores serve as tools, not goals. They exist to help lenders assess risk and help consumers access favorable loan terms. Any score above 800 accomplishes both objectives completely.

The behaviors that build toward 850—consistent on-time payments, low credit utilization, maintaining old accounts, diversifying credit types—matter far more than the specific number achieved. These habits create financial stability that extends well beyond credit scores.

According to the Consumer Financial Protection Bureau, credit affects ability to get loans, jobs, housing, insurance, and more. Understanding credit fundamentals helps protect creditworthiness over time.

Rather than obsessing over perfection, aim for excellence. Build sustainable financial habits. Monitor credit regularly for errors. Make informed decisions about when to use credit and how to manage it responsibly.

The score will follow. Whether it lands at 820 or 850, the practical benefits remain identical—and the peace of mind from solid financial habits proves far more valuable than any number on a report.