Quick Summary: Yes, buying a house with no money down is possible through several government-backed loan programs. VA loans for veterans and USDA loans for rural properties offer true zero-down-payment mortgages, while other programs like FHA loans require as little as 3.5% down.

Saving for a down payment feels impossible when the median home price in the United States is more than $400,000. A traditional 20% down payment would mean scraping together more than $80,000—a figure that puts homeownership out of reach for countless Americans.

But here’s the thing: that 20% number isn’t actually a requirement.

Several legitimate mortgage programs allow qualified borrowers to purchase homes with zero money down. Others require just 3-5% down, making homeownership significantly more accessible than most people realize.

This guide breaks down every real path to buying a house with no money down, who qualifies, and what trade-offs exist.

True Zero-Down Payment Mortgage Options

Only two loan types genuinely require zero dollars down: VA loans and USDA loans. Both are government-backed programs designed for specific populations.

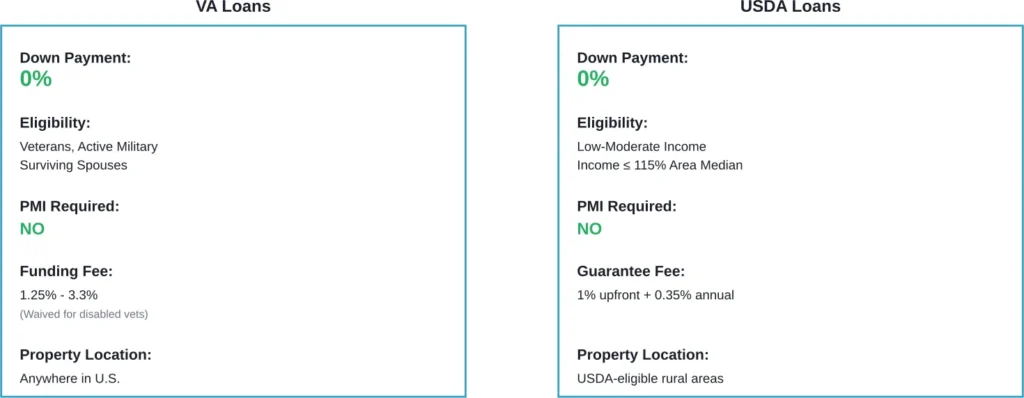

VA Loans: For Military Members and Veterans

According to the Department of Veterans Affairs, VA-backed purchase loans allow eligible borrowers to finance 100% of a home’s purchase price with competitive interest rates.

VA loans represent the most straightforward path to homeownership without a down payment. The program doesn’t require private mortgage insurance (PMI), which typically costs borrowers an additional 0.5-1% of the loan amount annually on conventional loans with less than 20% down.

Eligibility extends to active-duty service members, veterans, National Guard and Reserve members, and certain surviving spouses. The VA doesn’t set minimum credit score requirements, though most lenders typically look for scores around 620 or higher.

There’s one catch: the VA funding fee. This one-time payment ranges from 1.25% to 3.3% of the loan amount, depending on whether it’s a first-time VA loan use and the size of any down payment made. However, veterans with service-connected disabilities are exempt from this fee entirely.

The funding fee can be rolled into the loan amount rather than paid upfront, meaning borrowers don’t need cash on hand at closing for this expense.

USDA Loans: For Rural and Suburban Properties

The USDA Single Family Housing Guaranteed Loan Program assists approved lenders in providing financing to low- and moderate-income households purchasing homes in eligible rural areas.

Despite the “rural” designation, many suburban areas qualify. The USDA defines eligibility based on population density and other factors, meaning properties on the outskirts of many mid-sized cities meet program requirements.

USDA loans require zero down payment and offer competitive interest rates. Borrowers must meet income limits—cannot exceed 115% of median household income—and purchase a home in a USDA-eligible location.

Like VA loans, USDA mortgages come with an additional cost: an upfront guarantee fee of 1% of the loan amount plus an annual fee of 0.35% of the loan balance. These fees ensure the program’s financial sustainability.

Low-Down Payment Alternatives

Don’t qualify for VA or USDA financing? Several mortgage types require minimal down payments—typically 3-5% of the purchase price.

FHA Loans: 3.5% Down Payment

Federal Housing Administration (FHA) loans require just 3.5% down for borrowers with credit scores of 580 or higher. Those with scores between 500-579 may still qualify but need 10% down.

FHA loans are accessible to first-time buyers and repeat purchasers alike. The program doesn’t impose income limits, though borrowers must meet standard debt-to-income ratio requirements (typically below 50%).

The trade-off involves mortgage insurance. FHA loans require both an upfront mortgage insurance premium (1.75% of the loan amount) and annual mortgage insurance premiums that persist for the life of the loan if the down payment is less than 10%.

Conventional 97 Loans: 3% Down Payment

Conventional loans backed by Fannie Mae and Freddie Mac now offer options with just 3% down for qualified first-time homebuyers. These mortgages typically require credit scores of 620 or higher and adherence to standard debt-to-income ratios.

Conventional loans with less than 20% down require private mortgage insurance, but unlike FHA loans, this insurance can be removed once the borrower reaches 20% equity through payments or appreciation.

Down Payment Assistance Programs

Thousands of state and local programs provide down payment assistance to qualified buyers. These programs vary significantly by location but generally fall into several categories.

Some programs offer grants that don’t require repayment. Others provide second mortgages with deferred payment or forgivable loans that convert to grants after the homeowner meets certain residency requirements.

Many down payment assistance programs target first-time homebuyers, though definitions of “first-time” are often generous—sometimes anyone who hasn’t owned a home in the past three years qualifies.

Income limits typically apply, and borrowers often must complete homebuyer education courses. The assistance amounts vary but commonly range from $5,000 to $25,000 or a percentage of the purchase price.

Understanding the True Costs Beyond the Down Payment

Zero-down mortgages don’t mean zero costs at closing. Borrowers still face closing costs—typically 2-5% of the purchase price—covering appraisal fees, title insurance, origination fees, and other transaction expenses.

Some zero-down programs allow these costs to be rolled into the loan amount. Others permit sellers to contribute toward closing costs, and some down payment assistance programs cover both down payment and closing expenses.

Many lenders charge Veterans using VA-backed home loans a 1% flat fee (sometimes called a ‘loan origination fee’). Lenders may also charge additional fees.

| Loan Type | Down Payment | Minimum Credit Score | Mortgage Insurance |

|---|---|---|---|

| VA Loan | 0% | No official minimum (lenders typically 620+) | No PMI; Funding fee 1.25-3.3% |

| USDA Loan | 0% | Typically 640+ | 1% upfront + 0.35% annual |

| FHA Loan | 3.5% | 580+ (500-579 requires 10% down) | 1.75% upfront + annual premium |

| Conventional 97 | 3% | 620+ | PMI until 20% equity |

Pros and Cons of Zero-Down Mortgages

Advantages of No-Money-Down Home Buying

The most obvious benefit is immediate homeownership without years of saving. For renters paying $1,500-2,000 monthly, building equity instead of enriching a landlord offers significant long-term financial advantages.

Zero-down financing also preserves liquidity. Keeping cash reserves for emergencies, home repairs, or other investments provides financial flexibility that disappears when every dollar goes toward a down payment.

In appreciating markets, buying sooner rather than later can mean capturing equity growth that outpaces the modest additional interest costs of higher loan amounts.

Drawbacks to Consider

Higher loan amounts mean higher monthly payments. On a $400,000 home, the difference between zero down and 20% down could mean an extra $300-400 in monthly payments.

Starting with no equity leaves borrowers vulnerable if home values decline. Owing more than a home’s market value complicates selling or refinancing.

Many zero-down and low-down programs require some form of mortgage insurance, adding to monthly costs. This insurance protects lenders, not borrowers, against default risk.

Lenders may charge slightly higher interest rates on zero-down loans to offset increased risk, though government-backed programs often feature competitive rates despite minimal down payments.

Who Should Consider Zero-Down Mortgages?

Zero-down financing makes sense for specific buyer profiles. Military members and veterans with VA loan eligibility gain access to one of the best mortgage products available—competitive rates, no PMI, and zero down payment requirements create an unbeatable combination.

Buyers considering homes in USDA-eligible areas who meet income requirements benefit from similar advantages without military service requirements.

First-time buyers struggling to save while paying rent may find that low-down-payment conventional or FHA loans accelerate the path to homeownership. The opportunity cost of waiting years to save 20% down often exceeds the additional costs of mortgage insurance.

However, buyers with unstable income, minimal emergency savings, or uncertainty about staying in one location should approach cautiously. Homeownership involves ongoing costs—repairs, maintenance, property taxes, insurance—that don’t exist when renting.

Frequently Asked Questions

No. True zero-down mortgages are limited to VA loan-eligible veterans and service members, plus USDA loan-eligible buyers purchasing in designated rural areas. Others need at least 3-3.5% down for FHA or conventional loans.

Not necessarily. VA and USDA loans often feature competitive rates comparable to conventional mortgages despite requiring no down payment. The government backing reduces lender risk, allowing favorable terms. However, individual lender policies vary, so comparing offers remains essential.

VA loans have no official minimum credit score requirement set by the Department of Veterans Affairs, though most lenders prefer scores around 620. USDA loans typically require 640 or higher. FHA loans with 3.5% down accept scores as low as 580.

Generally no. VA loans technically allow eligible borrowers to purchase second homes with zero down, but lenders scrutinize these transactions carefully and usually require demonstration that the purchase serves legitimate relocation or military-related needs. USDA loans explicitly require the property to be a primary residence.

Down payment and closing costs are separate expenses. Zero-down refers only to the down payment. Closing costs—typically 2-5% of the purchase price—still apply. However, some loan programs allow these costs to be rolled into the loan amount, and sellers can sometimes contribute toward buyer closing costs.

Borrowers who finance 100% of a home’s value start with no equity. If property values decline, the mortgage balance can exceed the home’s market value—a situation called being “underwater.” This complicates selling or refinancing but doesn’t affect homeowners planning to stay long-term, as markets typically recover over time.

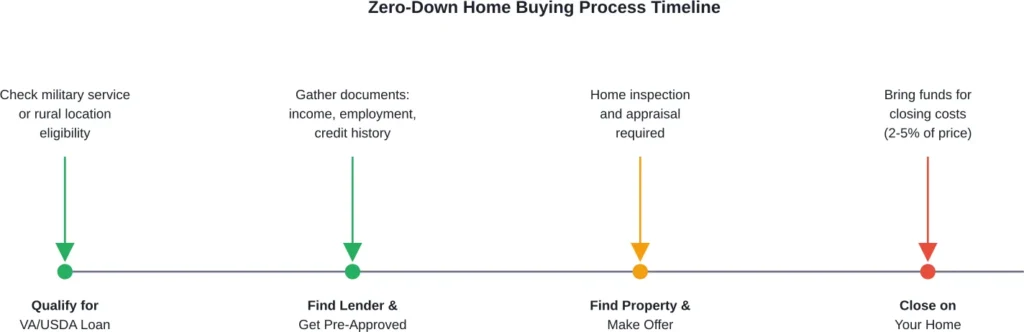

Timeline varies by lender and borrower preparedness. Obtaining a Certificate of Eligibility for VA loans can take several weeks if not already completed. USDA loans involve property eligibility verification. From application to closing, expect 30-60 days with complete documentation, similar to conventional mortgage timelines.

Making the Right Choice for Your Situation

Buying a house with no money down isn’t just possible—it’s a smart financial move for qualified borrowers. The key lies in understanding which program fits specific circumstances and recognizing the trade-offs involved.

VA and USDA loans offer unmatched opportunities for eligible buyers. The combination of zero down payment, competitive rates, and reasonable fees creates accessible paths to homeownership that were explicitly designed to serve military communities and rural America.

For those outside these programs, low-down-payment options through FHA or conventional loans require minimal savings while building equity instead of paying rent. When paired with down payment assistance programs, these mortgages become accessible to a much broader population.

The decision to pursue zero- or low-down financing should account for individual financial stability, long-term housing plans, and comfort with starting homeownership with minimal equity. For many buyers, the benefits of immediate homeownership outweigh the modest additional costs of financing more of the purchase price.

Start by checking eligibility for VA or USDA loans if applicable. Research local down payment assistance programs through state housing finance agencies. Compare multiple lender offers to find the best combination of rates, fees, and terms.

The path to homeownership without a traditional 20% down payment is well-established and thoroughly legitimate. Understanding the options available turns what seems impossible into an achievable goal.