Quick Summary: Yes, refinancing a car loan is not only possible but often beneficial. Car loan refinancing involves replacing your existing auto loan with a new one, typically to secure a lower interest rate, reduce monthly payments, or adjust the loan term. According to the Consumer Financial Protection Bureau, contacting your lender or servicer about available options—which may include affordable payment plans, changing your due date, or pausing payments through forbearance—should be a priority when facing payment challenges.

The question of whether refinancing a car loan is possible comes up frequently among vehicle owners looking to improve their financial situation. The short answer? Absolutely. Auto loan refinancing has become a standard financial tool that millions of drivers use to optimize their car payments.

But here’s what matters more than whether it’s possible—understanding when it makes sense, how the process works, and what benefits it can deliver. Some drivers refinance immediately after purchasing a vehicle, while others wait until their credit score improves or interest rates drop.

Real talk: refinancing isn’t always the right move for everyone. The process involves taking out a new loan to pay off your existing one, and while this can lead to significant savings, it requires careful consideration of your current financial situation, loan terms, and long-term goals.

What Is Auto Loan Refinancing?

Auto loan refinancing means replacing your current car loan with a new one, typically from a different lender. The new lender pays off your existing loan, and from that point forward, payments go to the new lender under the new terms.

Think of it as hitting the reset button on your car financing. The vehicle remains yours throughout the process—you’re simply changing who holds the loan and under what conditions.

Most refinancing applications work similarly across lenders. Capital One reports a 4.8 rating based on 26,361 reviews, with 87% receiving 5-star ratings. This suggests that when done properly, refinancing typically delivers positive results for borrowers.

How Refinancing Differs From Your Original Loan

The original auto loan happens at purchase time, often through a dealership’s financing arm. Refinancing occurs later, when circumstances have changed or better options become available.

Your original loan might have been secured quickly to complete the car purchase, possibly with less-than-ideal terms. Refinancing gives a second chance to negotiate better conditions with the benefit of time and potentially improved creditworthiness.

Why Refinance a Car Loan?

Several compelling reasons drive people toward auto refinancing. Understanding these motivations helps determine whether refinancing aligns with specific financial goals.

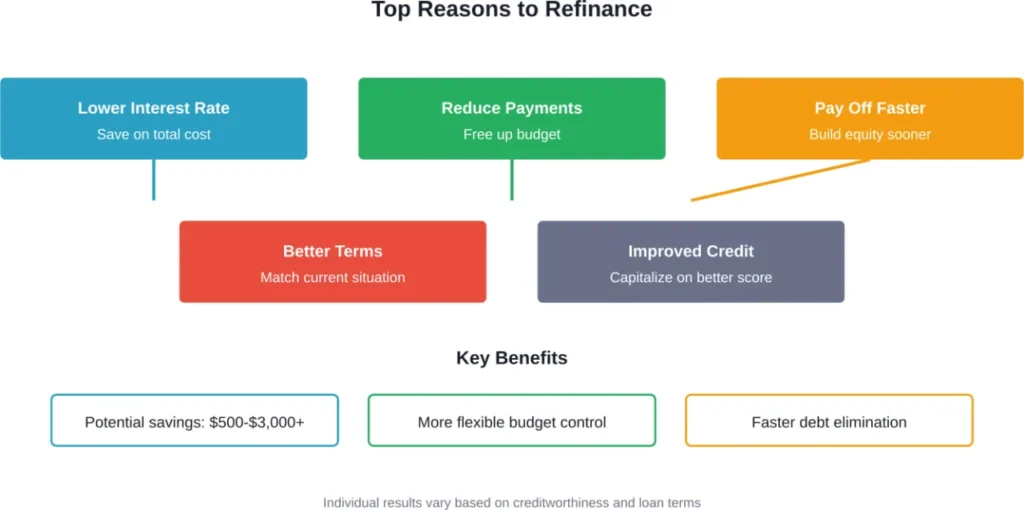

Lower Your Interest Rate

A lower APR reduces the total cost of borrowing over the life of the loan. Even a difference of 1-2 percentage points can translate to hundreds or thousands of dollars in savings, depending on the loan balance and remaining term.

Interest rates fluctuate based on market conditions and individual creditworthiness. If rates have dropped since the original loan or if credit scores have improved, refinancing becomes particularly attractive.

Reduce Monthly Payments

Lower payments free up monthly budget space for other financial goals or necessities. This can be achieved through either a lower interest rate or by extending the loan term.

According to the Consumer Financial Protection Bureau, contacting lenders about payment options should be a priority when experiencing financial difficulties. Refinancing represents one legitimate avenue for reducing payment burdens.

Pay Off Your Loan Faster

Some borrowers refinance to shorten their loan term. While this typically increases monthly payments, it reduces total interest paid and builds equity faster.

A shorter term means reaching that final payment sooner and owning the vehicle outright. For those with improved income or reduced expenses, this strategy accelerates debt elimination.

Adjust Loan Terms to Match Financial Changes

Life circumstances evolve. A job promotion, career change, or shift in family finances might make different loan terms more suitable than when originally financed.

Refinancing provides flexibility to align loan obligations with current financial realities rather than remaining locked into outdated terms.

When Should You Consider Refinancing?

Timing matters significantly when refinancing an auto loan. Certain situations present better opportunities than others.

Your Credit Score Has Improved

Credit scores directly impact interest rates offered by lenders. A higher score typically qualifies borrowers for better rates.

If credit scores have increased since the original financing, refinancing opportunities become more favorable. Building credit takes time—according to financial counseling organizations like the NFCC, establishing good credit requires consistent payment history and maintaining utilization ratios of 30% or less.

Interest Rates Have Dropped

Market interest rates fluctuate based on economic conditions. When rates fall significantly below what was secured originally, refinancing becomes financially sensible.

Even without personal credit improvements, broader rate decreases can open doors to better terms. Monitoring rate trends helps identify optimal refinancing windows.

Your Financial Situation Has Changed

Income increases, job stability improvements, or reduced debt loads all strengthen refinancing applications. Lenders view these factors positively when evaluating new loan requests.

Conversely, if facing financial hardship, the Consumer Financial Protection Bureau advises contacting lenders early to discuss available options, which may include refinancing to more manageable terms.

You Originally Financed Through a Dealership

Dealership financing, while convenient at purchase time, doesn’t always offer the most competitive rates. Many buyers accept dealer terms to expedite the buying process without shopping extensively for financing.

Refinancing later with banks, credit unions, or online lenders often reveals better rate options that weren’t considered during the initial purchase excitement.

You’re Not Too Late in the Loan Term

Refinancing makes most financial sense earlier in the loan term when more interest remains to be saved. As loans mature, more of each payment goes toward principal rather than interest.

Generally speaking, refinancing works best within the first two-thirds of the loan term. Beyond that point, the effort and costs associated with refinancing may outweigh potential savings.

How to Refinance a Car Loan: Step-by-Step Process

The refinancing process follows a structured path that most lenders handle similarly. Understanding these steps removes uncertainty from the experience.

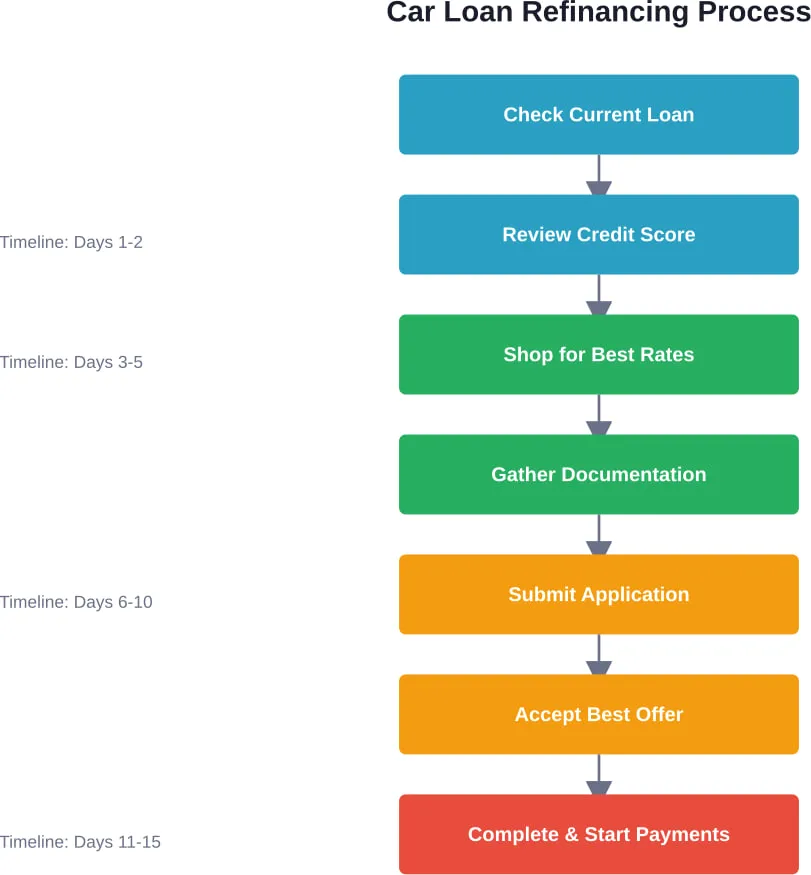

Step 1: Check Your Current Loan Details

Start by gathering information about the existing loan. Key details include the current interest rate, remaining balance, monthly payment amount, and payoff date.

Contact the current lender to obtain the exact payoff amount, which may differ from the remaining balance shown on statements due to accrued interest and potential fees.

According to the Consumer Financial Protection Bureau, understanding contract terms is essential before making changes. Review whether prepayment penalties exist—some states prohibit these for auto loans, but checking the specific contract prevents surprises.

Step 2: Review Your Credit Score

Credit scores determine available interest rates. Checking scores before applying provides realistic expectations about likely offers.

Free credit reports can be obtained through federally authorized sources. Review reports for errors that might artificially lower scores and dispute inaccuracies before applying for refinancing.

Step 3: Shop Around for the Best Rates

Different lenders offer varying rates and terms. Banks, credit unions, and online lenders each bring different advantages to the table.

Many lenders provide pre-qualification options that use soft credit inquiries, which don’t impact credit scores. Capital One emphasizes that checking pre-qualified offers involves no impact to credit scores and no commitment.

Compare at least three to five lenders to identify the most competitive options. Look beyond interest rates to fees, term options, and customer service quality.

Step 4: Gather Required Documentation

Lenders require documentation to process refinancing applications. Common requirements include proof of income, proof of residence, vehicle information, insurance verification, and identification.

Having documents ready accelerates the application process. Digital copies stored securely allow quick submission through online applications.

Step 5: Submit Your Application

Complete the formal application with chosen lenders. This triggers a hard credit inquiry, which may temporarily lower credit scores by a few points.

Multiple applications within a short window typically count as a single inquiry for credit scoring purposes, allowing rate shopping without excessive score damage.

Step 6: Review and Accept an Offer

Compare approved offers carefully. Look at the interest rate, monthly payment, loan term, total amount to be repaid, and any fees involved.

A lower monthly payment isn’t always the best deal if it comes with an extended term that increases total interest paid. Calculate the full cost of each option.

Step 7: Complete the Paperwork

Once an offer is accepted, final paperwork must be completed. Many lenders handle this process digitally through electronic signatures.

The new lender will pay off the existing loan directly. This typically takes several days to process completely.

Step 8: Continue Making Payments to Your Old Lender

Until the payoff processes completely, continue making scheduled payments to the existing lender. Missing payments during the transition period can damage credit and incur late fees.

After the old loan is paid off, confirm closure and begin making payments to the new lender according to the new schedule.

Eligibility Requirements for Refinancing

Not all vehicles or borrowers qualify for refinancing. Lenders impose requirements to manage their risk.

Vehicle Requirements

Chase Auto Finance specifies that vehicles must meet certain criteria for refinancing eligibility. The estimated payoff must be between $4,000 and $99,999.

Most lenders have restrictions on vehicle age, mileage, and condition. Older vehicles or those with high mileage may not qualify, as they present greater risk due to depreciation.

Vehicles currently financed with certain lenders may also be ineligible. Chase notes that cars financed through their own system or specific manufacturers like Aston Martin Financial Services, Jaguar Financial Group, Land Rover Financial Group, Maserati Capital USA, McLaren Financial Services, or Rivian Financial Services cannot be refinanced through them.

Borrower Requirements

Credit scores represent a primary qualification factor. While minimum scores vary by lender, most prefer scores above 600 for competitive rates.

Income verification demonstrates the ability to repay the new loan. Stable employment history strengthens applications.

Debt-to-income ratios also matter. Lenders assess whether existing obligations leave sufficient income to comfortably handle the refinanced payment.

Loan Requirements

Some lenders won’t refinance loans below certain amounts or with very short remaining terms. The administrative costs of refinancing small balances may outweigh benefits for both lender and borrower.

Current loan standing also affects eligibility. Late payments or delinquent status can disqualify applicants or result in unfavorable terms.

Potential Downsides of Refinancing

While refinancing offers benefits, potential drawbacks deserve consideration before proceeding.

Prepayment Penalties

Some auto loans include prepayment penalties that charge fees for paying off the loan early. According to the Consumer Financial Protection Bureau, contract terms and state law determine whether these penalties apply.

Certain states prohibit prepayment penalties for auto loans, but not all do. Reviewing the existing loan contract reveals whether penalties would offset refinancing savings.

Extended Loan Terms

Extending the loan term to lower monthly payments means paying interest for a longer period. This increases the total amount paid over the life of the loan.

A vehicle might be worth less than what’s owed for a longer period, creating negative equity situations that complicate future selling or trading.

Fees and Costs

Refinancing may involve application fees, title transfer fees, or other administrative costs. These expenses reduce net savings from better rates.

Some lenders charge no fees, while others do. Comparing the total cost of refinancing, including all fees, against projected savings reveals whether the move makes financial sense.

Impact on Credit Score

Refinancing applications trigger hard credit inquiries that can temporarily lower scores. The impact is typically minor—a few points—and temporary, but it matters for those planning other credit applications soon.

Opening a new loan and closing an old one also affects credit mix and account age, though these impacts are usually minimal for auto loans.

Loss of Original Loan Benefits

According to Chase, purchasing other products, warranties, or insurance like GAP coverage through the original loan may complicate refinancing. These products might not transfer to the new loan.

Some borrowers may have special benefits tied to their original financing, such as loyalty discounts or promotional terms, that would be lost through refinancing.

| Aspect | Potential Benefit | Potential Drawback |

|---|---|---|

| Interest Rate | Lower rate saves money | Rate reduction may be minimal |

| Monthly Payment | Reduced payments improve cash flow | May require extending loan term |

| Loan Term | Shorten term to pay off faster | Extend term, paying more total interest |

| Credit Score | Can improve with on-time payments | Hard inquiry temporarily lowers score |

| Total Cost | Significant savings over loan life | Fees may reduce or eliminate savings |

| Flexibility | Adjust terms to current needs | May lose benefits from original loan |

How Much Can You Save by Refinancing?

Savings from refinancing vary dramatically based on individual circumstances. The interest rate difference, remaining loan balance, and loan term all influence total savings.

Potential monthly payment reductions vary significantly depending on individual circumstances such as rate reduction achieved and loan balance.

Here’s what drives savings calculations:

- The interest rate reduction achieved through refinancing

- The amount still owed on the vehicle

- The time remaining on the original loan

- Whether the new loan term is shorter, longer, or the same

- Any fees associated with the refinancing process

Rate reductions through refinancing improve financial outcomes, with the benefit depending on loan balance and remaining term.

Refinancing vs. Other Options

Refinancing isn’t the only solution when facing auto loan challenges or seeking better terms.

Loan Modification

The Consumer Financial Protection Bureau advises that borrowers experiencing payment difficulties should contact their lender to discuss available options. Some lenders offer loan modifications that adjust terms without requiring full refinancing.

Modifications might include temporary payment reductions, deferments, or term extensions. These options typically work best for short-term financial hardships.

Making Extra Payments

Instead of refinancing, making additional principal payments on the existing loan reduces interest costs and shortens the loan term without the hassle of refinancing.

The Consumer Financial Protection Bureau notes that contract terms and state law determine whether prepayment is allowed without penalty. Most auto loans permit extra payments, but verification prevents surprises.

Trading In or Selling the Vehicle

For those struggling with payments or dealing with an unsuitable vehicle, selling or trading might solve the problem more directly than refinancing.

This works best when the vehicle’s value exceeds the loan balance. Negative equity situations make this approach more complicated.

Common Refinancing Mistakes to Avoid

Several pitfalls can undermine refinancing benefits or lead to worse outcomes than before.

Not Shopping Around

Accepting the first refinancing offer without comparing alternatives potentially leaves money on the table. Rate differences between lenders can be substantial.

Using pre-qualification tools from multiple lenders identifies the best available terms without impacting credit scores.

Focusing Only on Monthly Payment

Lower monthly payments look attractive, but they don’t tell the whole story. Extended loan terms achieve lower payments while increasing total interest paid.

Calculate the total amount to be repaid under each option, not just the monthly figure.

Ignoring Fees

Overlooking application fees, title fees, or early payoff penalties on the existing loan can turn an apparently good deal into a financial wash.

Request detailed fee schedules from potential lenders before committing.

Refinancing Too Late

Waiting until most of the loan is paid creates minimal opportunity for savings. The bulk of interest is paid in the early years of most loans.

Refinancing works best earlier in the loan term when more interest remains to be saved.

Not Checking Credit First

Applying for refinancing without knowing credit scores can lead to disappointment when offers don’t meet expectations.

Reviewing credit reports beforehand allows time to correct errors and understand likely rate ranges.

Frequently Asked Questions

Technically, refinancing can happen at any time after the original loan is established. Some drivers refinance immediately after purchase if they secured unfavorable dealer financing. Waiting a period after loan origination to establish a payment history may be advisable before refinancing. Some lenders may have minimum waiting periods before they’ll consider refinancing applications.

Refinancing causes a temporary, minor impact to credit scores due to the hard inquiry performed during application. This typically results in a drop of a few points that recovers within months. The long-term impact depends on payment behavior with the new loan. Consistent on-time payments can improve scores over time, while missed payments damage credit significantly. The short-term inquiry impact is usually far less important than the potential financial benefits of better loan terms.

Some lenders allow refinancing of their own loans, but many do not. Chase explicitly states that they cannot refinance existing Chase auto financing. Policies vary by institution, so checking with the current lender reveals whether internal refinancing is possible. Even when allowed, comparing offers from other lenders ensures the best available terms are secured.

Minimum credit scores for refinancing vary by lender and desired rates. Generally speaking, scores above 600 make refinancing possible, though the most favorable rates typically require scores of 700 or higher. Lenders consider credit scores alongside other factors like income, debt-to-income ratio, and vehicle value. Those with lower scores may still qualify but should expect higher interest rates than those with excellent credit.

According to information from various lenders, the refinancing timeline typically spans 1-2 weeks from application to completion. Pre-qualification happens within minutes. Formal approval usually takes 1-3 business days. Processing the paperwork and paying off the existing loan adds another 5-10 days. Some lenders offer expedited processing that completes everything within a few days. The exact timeline depends on how quickly borrowers provide required documentation and how efficiently lenders process applications.

Fee structures vary significantly between lenders. Chase notes in their FAQ that fee information is specific to individual situations and applications. Some lenders charge application fees, while others don’t. State-specific title transfer fees often apply when changing lenders. Prepayment penalties on the existing loan might also factor in, depending on the original loan contract. Always request a complete breakdown of all potential fees before committing to refinancing.

Refinancing when owing more than the vehicle’s worth—being upside-down or having negative equity—is challenging but sometimes possible. Lenders typically limit loans to the vehicle’s actual value, making refinancing the full balance difficult. Some lenders offer programs specifically for negative equity situations, though rates may not be as favorable. In these cases, paying down principal to reach neutral or positive equity before refinancing often produces better results.

Choosing the Right Refinancing Lender

The lender selected for refinancing significantly impacts the experience and outcomes.

Banks vs. Credit Unions vs. Online Lenders

Traditional banks offer stability and established processes but may not provide the most competitive rates. Credit unions often deliver excellent rates to members but require membership eligibility.

Online lenders have grown rapidly in the refinancing space. Capital One’s high customer satisfaction ratings—4.8 out of 5 based on over 26,000 reviews—demonstrate that digital refinancing experiences can be quite positive.

Each lender type brings different advantages. Comparing all three categories usually identifies the best combination of rates, terms, and service.

What to Look for in a Refinancing Lender

Beyond interest rates, several factors distinguish quality lenders:

- Transparent fee structures with no hidden costs

- Flexible term options that allow customization

- Efficient application and approval processes

- Responsive customer service for questions and issues

- Positive customer reviews and ratings

- Digital account management tools

Reading reviews from actual customers provides insight into lender reliability and service quality beyond marketing promises.

Special Considerations

Refinancing With a Co-Signer

Original loans may have included co-signers to qualify. Refinancing offers opportunities to remove co-signers if credit has improved sufficiently to qualify independently.

According to the National Foundation for Credit Counseling, being released as a co-signer removes legal liability for the debt and can benefit both parties’ financial profiles.

Alternatively, refinancing could add a co-signer if needed to secure better terms.

Refinancing After Bankruptcy or Repossession

Past financial difficulties complicate but don’t necessarily prevent refinancing. Lenders view recent bankruptcies or repossessions as significant risk factors.

Waiting periods after bankruptcy and demonstrating improved financial management may increase approval chances. Rates may be higher than for those with clean credit histories.

State-Specific Considerations

Auto loan regulations vary by state. Some states prohibit prepayment penalties, while others allow them. Title transfer processes and associated fees differ across jurisdictions.

Chase notes that auto refinancing may not be available in all states. Checking state-specific rules and lender availability prevents wasted effort on applications that can’t be completed.

Conclusion

Refinancing a car loan is not only possible but often beneficial for those seeking better financial terms. The process replaces an existing auto loan with a new one, potentially delivering lower interest rates, reduced monthly payments, or shortened loan terms.

But here’s what really matters: refinancing works best when approached strategically. Shopping around for the best rates, understanding all associated costs, and timing the refinance appropriately maximize benefits while avoiding common pitfalls.

The Consumer Financial Protection Bureau emphasizes contacting lenders to explore options when facing payment challenges or seeking better terms. Whether motivated by improved credit, falling interest rates, or changing financial circumstances, refinancing provides a legitimate path to optimizing auto loan costs.

Not every situation calls for refinancing. Those late in their loan term, facing substantial fees, or dealing with minimal rate improvements may find limited benefits. Calculating total costs and savings rather than focusing solely on monthly payments reveals whether refinancing makes financial sense.

For those who do refinance, the potential savings can be substantial—hundreds or thousands of dollars over the loan life. The key lies in careful research, honest assessment of personal financial situations, and selecting lenders offering truly competitive terms rather than settling for the first available option.

Ready to explore refinancing your car loan? Start by checking your current loan details and credit score, then compare offers from multiple lenders to find the best fit for your financial goals. The time invested in proper comparison shopping typically pays dividends through better terms and significant long-term savings.