Quick Summary: If you don’t pay medical bills, providers typically send them to collections after 60-180 days, which can trigger collection calls and lawsuits. However, unpaid medical debt under $500 or less than a year old no longer appears on credit reports as of 2023. Patients have multiple options to avoid collection, including payment plans, financial assistance, bill negotiation, and legal protections under the No Surprises Act.

Medical bills arrive when people are already dealing with health crises. Then comes the financial shock.

Millions of Americans face unpaid medical bills every year. One in seven Americans has unpaid medical bills. The question isn’t whether this happens—it’s what comes next when those bills go unpaid.

The answer isn’t as straightforward as other debts. Medical billing works differently than credit cards or student loans. There are protections, timelines, and options that most people don’t know exist.

Here’s what actually happens when medical bills remain unpaid, and what can be done about it.

The Timeline: What Happens After You Miss Payment

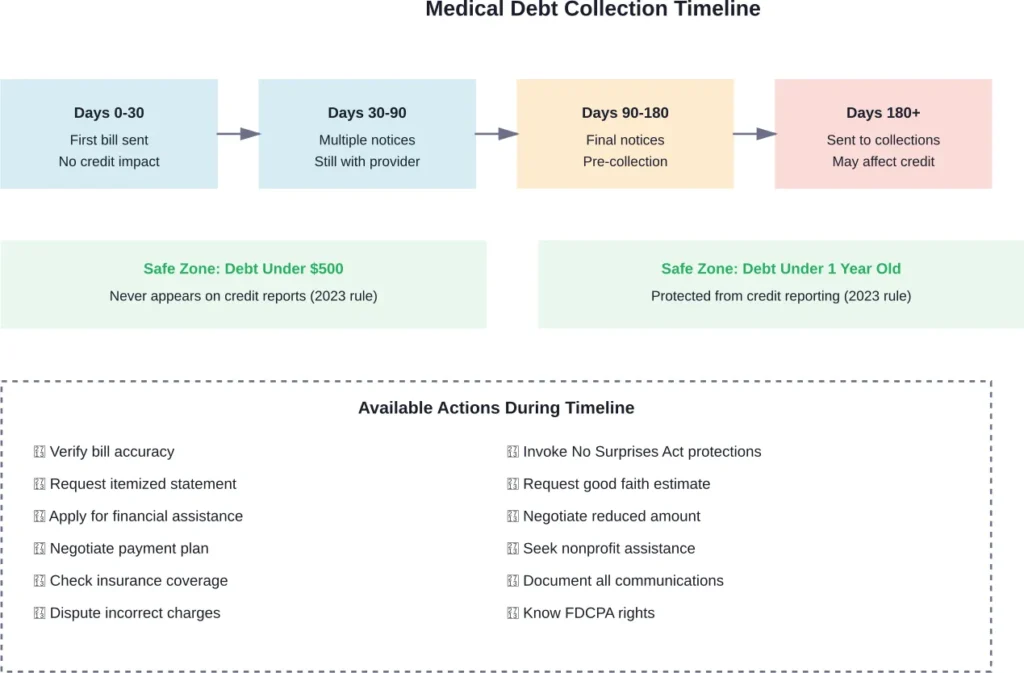

Medical providers don’t immediately send bills to collections. There’s a process.

Most hospitals and medical offices start with billing statements. These arrive 30 to 60 days after treatment. The first bill is just that—a bill. No threats, no collection language.

If that first statement goes unpaid, a second notice follows. Then a third. Providers typically send multiple billing statements over 90 to 180 days before taking further action.

During this window, the bill stays with the original provider. It doesn’t affect credit scores. It’s just debt owed to the hospital or doctor’s office.

But here’s where it changes. After roughly 120 to 180 days of non-payment, many providers sell the debt to a collection agency or hire collectors to pursue payment. According to the Consumer Financial Protection Bureau, this transition to third-party debt collectors marks when federal protections under the Fair Debt Collection Practices Act kick in.

Once a collection agency gets involved, the calls start. Letters arrive. The pressure increases.

How Medical Debt Collection Actually Works

Collection agencies operate under specific rules when pursuing medical debt.

The Fair Debt Collection Practices Act prohibits collectors from using abusive, unfair, or deceptive practices. They cannot call at odd hours, threaten criminal charges, or harass family members. These aren’t suggestions—they’re federal requirements.

When a collector contacts someone about medical debt, they must provide written validation of the debt within five days. This notice must include the amount owed, the name of the creditor, and information about disputing the debt.

Many people assume medical debt is different from other consumer debt. It is, but only in specific ways. Unlike credit card companies, medical providers typically don’t report unpaid bills to credit bureaus directly. That usually only happens after the debt reaches collections.

And even then, new rules have changed the game.

The 2023 Credit Reporting Changes

As of April 2023, Equifax, Experian, and TransUnion implemented significant changes to how medical debt appears on credit reports.

Medical debts under $500 no longer appear on credit reports at all. Debts less than one year old also stay off credit reports, regardless of amount. This gives people time to resolve billing disputes and arrange payment without immediate credit damage.

For someone with an $800 hospital bill that’s 10 months old, their credit report remains clean even if the debt sits in collections. That’s a substantial shift from previous policies where any collection could tank a credit score.

Research from Gies College of Business at the University of Illinois found that eliminating small medical debts from credit reports had minimal impact on credit scores or borrowing behavior. The study examined debts just below versus just above the $500 threshold and found no significant differences in financial outcomes.

Still, larger debts or older debts can appear on credit reports and affect creditworthiness.

Legal Consequences: Can Medical Providers Sue?

Yes. Medical providers and collection agencies can file lawsuits for unpaid bills.

These lawsuits typically happen when debt amounts are substantial—usually over $1,000—and collection efforts have failed. Small bills rarely end up in court because legal fees often exceed the debt value.

If a provider or collector sues and wins, the court issues a judgment. That judgment allows them to garnish wages or levy bank accounts to collect the debt.

According to the Consumer Financial Protection Bureau, state and federal laws limit how much a creditor can garnish from wages. Some income sources have protection from garnishment. Social Security benefits, veterans’ benefits, and certain other federal benefits generally cannot be garnished for medical debt. State laws provide additional protections—check LawHelp.org for specific state exemptions.

But here’s the thing: lawsuits are avoidable. Most providers would rather work out payment arrangements than pursue legal action. Court costs money and time. A payment plan costs neither.

Your Rights Under Federal Law

The No Surprises Act, which took effect in 2022, fundamentally changed medical billing rules.

This law protects people from unexpected out-of-network bills for emergency services. When someone goes to an emergency room, they cannot be balance-billed for out-of-network charges, even if the hospital or specific providers aren’t in their insurance network.

The law also covers non-emergency services at in-network facilities when out-of-network providers deliver care without the patient’s knowledge or consent. That anesthesiologist who wasn’t in-network? Protected. The assistant surgeon? Protected.

According to CMS, providers must give good faith estimates to uninsured patients or those not using insurance for scheduled services. This estimate must include expected charges when services are booked at least three business days in advance.

If actual charges exceed the good faith estimate by more than $400, patients can dispute the bill through a federal resolution process.

The Consumer Financial Protection Bureau has made clear that debt collection or credit reporting on medical bills exceeding amounts permitted under the No Surprises Act may violate federal law. That’s not a minor point—it’s enforceable protection.

Medicare Recipients Have Additional Protections

In October 2024, the CFPB and CMS issued a joint statement specifically protecting low-income Medicare beneficiaries from improper billing.

According to this guidance, certain Medicare recipients should not receive bills for services already covered. When Medicare Advantage plans give providers incorrect payment information, the resulting bills can cascade into collection actions and credit damage—all based on billing errors.

These improper bills create lasting financial harm for people who should never have been billed in the first place.

What to Do When Bills Arrive

The first step isn’t payment. It’s verification.

Medical bills contain errors frequently. Billing codes get mixed up. Services get duplicated. Insurance coverage gets miscalculated. According to a Consumer Reports survey, nearly 40% of people negotiated payment, and 57% succeeded in lowering their bill—and that starts with finding errors.

Request an itemized statement. This detailed breakdown shows every charge, procedure code, and service. Compare it against what actually happened during treatment.

Look for duplicate charges, services that weren’t provided, and incorrect billing codes. Check whether insurance processed claims correctly. Mistakes happen at multiple points in the billing chain.

If the insurance explanation of benefits shows the claim was denied or partially covered, find out why. Sometimes resubmitting with correct information changes everything.

Financial Assistance Programs Most People Don’t Use

Hospitals don’t advertise this, but many are required to offer financial assistance.

Nonprofit hospitals must provide charity care to qualify for tax-exempt status. These programs reduce or eliminate bills for patients below certain income thresholds—often 200% to 400% of the federal poverty level.

That means a family of four earning under $120,000 might qualify for reduced bills at many hospitals. But people have to ask. Applications don’t magically appear.

The application process requires documentation: pay stubs, tax returns, proof of income. It takes time. But for someone facing a $20,000 hospital bill, the effort pays off when the balance drops to $5,000 or disappears entirely.

According to the CFPB, patients should explore financial assistance before putting medical debt on credit cards. Credit card interest compounds the problem. Financial assistance eliminates it.

Negotiating Medical Bills Down

Medical bill negotiation works more often than people expect.

Providers set list prices knowing insurance companies negotiate them down. Uninsured patients often get charged full list prices—rates that insured patients never pay. That’s backwards, and providers know it.

Call the billing department. Explain the situation. Ask about payment plans, discounts for upfront payment, or reduced rates for uninsured patients.

Many hospitals offer prompt-pay discounts that providers sometimes offer. Even without ready cash, mentioning these discounts sometimes leads to other negotiation opportunities.

The Cornell ILR School documented one case where a worker earning $15 per hour faced over $20,000 in medical debt after a life-saving procedure. Despite having insurance, out-of-pocket costs created crushing debt. The person avoided follow-up care because additional bills seemed inevitable.

That avoidance of necessary care—driven by fear of more bills—happens constantly. Negotiating existing bills prevents that spiral.

| Negotiation Strategy | When It Works Best | Typical Reduction |

|---|---|---|

| Prompt payment discount | Bills under $5,000, paid within 30 days | 10-30% off total |

| Uninsured patient rate | No insurance was used for services | 20-50% off list price |

| Financial hardship appeal | Income below 400% federal poverty level | 50-100% reduction |

| Payment plan with reduced total | Bills over $1,000, long-term payment needed | 10-25% off total |

| Billing error correction | Duplicate charges or incorrect codes found | Varies by error |

Setting Up Payment Plans

Payment plans keep bills out of collections. Most providers offer them.

These arrangements spread the debt over months or years with no interest. A $6,000 hospital bill might become $250 monthly for 24 months. That’s manageable for many people who couldn’t pay $6,000 upfront.

The key: set up the plan before the bill goes to collections. Once a collection agency owns the debt, the original provider can’t help anymore.

Get payment plan terms in writing. Confirm the monthly amount, the duration, whether interest applies, and what happens if a payment is missed. Documentation prevents disputes later.

Making even small payments shows good faith. If $250 monthly isn’t feasible, propose $100. Providers often accept lower amounts rather than sending bills to collections where they might recover nothing.

Dealing With Collection Agencies

When debt reaches collections, the dynamic changes.

Collection agencies purchase medical debt often for a fraction of face value. That $5,000 hospital bill? The collection agency might have paid $250 for it.

This creates negotiation leverage. Offering to settle for 30% to 50% of the balance might get accepted because the agency still profits.

But negotiate carefully. Get settlement terms in writing before paying anything. Confirm that the agreed payment will satisfy the debt in full and that the account will be reported as settled to credit bureaus.

Never give collection agencies electronic access to bank accounts. Pay by money order or check where there’s a clear payment trail and no risk of unauthorized withdrawals.

Under the Fair Debt Collection Practices Act, people can request that collectors stop calling. Send a written request via certified mail. After receiving it, collectors can only contact someone once more to confirm they’re ceasing communication or to notify about specific legal action.

Spotting Collection Scams

Fake debt collectors target people with medical bills.

According to Fidelity, scammers posing as collectors ask for personal financial information, refuse to provide their phone number or company details, or threaten criminal charges.

Real collectors can’t threaten arrest. Medical debt isn’t a criminal matter. Anyone making those threats is running a scam.

Legitimate collectors must provide written debt validation within five days of first contact. If someone calls demanding immediate payment without sending written notice, that’s a red flag.

Verify any collection claim by contacting the original healthcare provider directly. Don’t use phone numbers the collector provides—look up the provider independently.

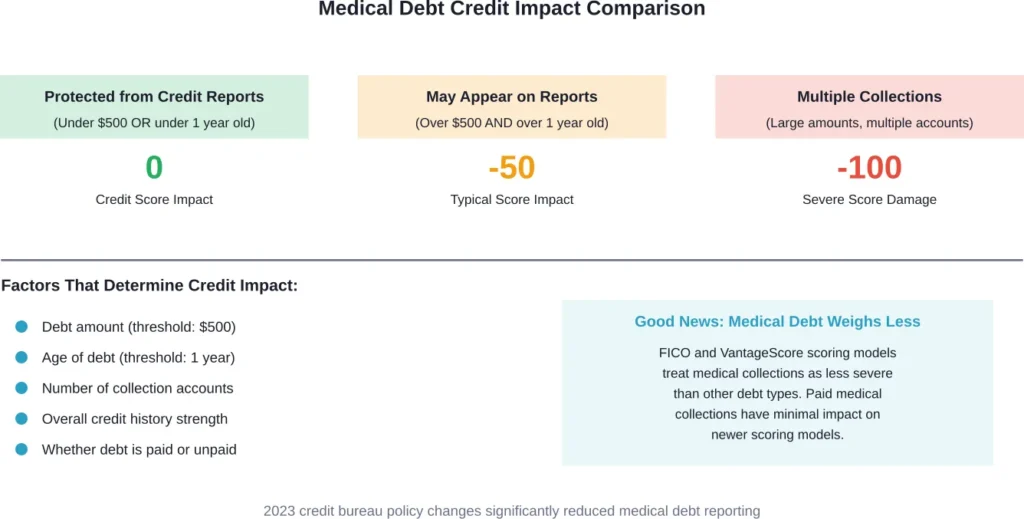

Impact on Credit Scores

Medical debt affects credit differently than it used to.

The 2023 credit reporting changes mean most recent and small medical debts stay off credit reports entirely. But larger, older debts can still appear and damage scores.

When medical collections do appear on credit reports, their impact has lessened. FICO and VantageScore have both reduced how much medical debt affects credit scores compared to other collection types.

Still, a medical collection on a credit report can drop scores, with typical score impact varies depending on overall credit health. For someone with limited credit history, the impact hits harder.

Once medical debt is paid or settled, getting it removed from credit reports takes effort. The account should be updated to show zero balance, but the collection record might remain for up to seven years from the date of first delinquency.

Some people successfully negotiate “pay for delete” agreements where the collection agency removes the tradeline entirely in exchange for payment. Not all agencies agree to this, and credit bureaus discourage it, but it happens.

When Medical Bills Are Actually Wrong

Surprise medical bills used to devastate finances. Someone would go to an in-network hospital and get treated by an out-of-network doctor they never chose. Then came a massive bill.

The No Surprises Act ended most of this. Emergency services cannot generate surprise out-of-network bills anymore. Non-emergency services at in-network facilities have similar protections when out-of-network providers get involved without patient consent.

If someone receives a surprise bill that should be protected under this law, they don’t have to pay it. Instead, file a complaint with CMS and the state insurance commissioner.

Providers and insurers must resolve payment disputes through an independent dispute resolution process—one that doesn’t involve patients paying incorrect bills.

According to the Consumer Financial Protection Bureau, collectors cannot pursue debts that exceed amounts permitted under the No Surprises Act. Doing so violates federal consumer protection laws.

Building Financial Protection Against Future Bills

Medical bills arrive unexpectedly. Planning for them reduces the panic.

Health Savings Accounts and Flexible Spending Accounts let people set aside pre-tax money for medical expenses. An HSA contribution of $200 monthly creates a $2,400 cushion by year’s end.

That won’t cover every possible medical event, but it handles many urgent care visits, specialist copays, and prescription costs without triggering financial crisis.

Emergency savings serve a similar function for people without access to HSAs or FSAs. Even $1,000 in savings prevents small medical bills from becoming collection accounts.

According to Fidelity, setting aside cash specifically for medical expenses helps people avoid putting healthcare costs on high-interest credit cards—a move that compounds financial problems rather than solving them.

State-Specific Protections

Federal laws provide baseline protections. State laws often add more.

Some states prohibit medical debt from appearing on credit reports entirely. Others limit collection practices beyond federal requirements. A few states require extended timelines before debt can be sold to collectors.

Texas, for example, has specific rules about timely billing. Providers must submit bills within reasonable timeframes or lose collection rights. TexasLawHelp.org provides detailed guidance on surprise billing protections and medical debt rights under state law.

Check state-specific resources at LawHelp.org to understand local protections. What applies in California might differ significantly from Florida or New York.

What Happens With Government Healthcare Programs

Medicare and Medicaid recipients face unique situations with unpaid bills.

Medicaid typically covers approved services completely or nearly completely. If someone on Medicaid receives a bill for covered services, that’s often a billing error. Providers should bill Medicaid directly, not patients.

Medicare works differently. It covers 80% of many services after deductibles, leaving beneficiaries responsible for the remaining 20%. Supplemental insurance often covers these gaps, but people without supplements can face substantial bills.

The October 2024 CFPB and CMS joint statement specifically addressed improper billing of low-income Medicare recipients. When Medicare Advantage plans provide incorrect payment information to providers, patients sometimes get billed for amounts they don’t actually owe.

These billing errors create collection nightmares for people who should never have been billed. Anyone on Medicare receiving questionable bills should contact their plan administrator and Medicare directly to verify whether the charges are legitimate.

Bankruptcy and Medical Debt

Medical debt is one of the leading causes of bankruptcy filings in America.

Research from Utah State University (published 2019) found that medical debt threatens the financial stability of vulnerable populations: the sick, elderly, poor, veterans, and middle class. For those facing bankruptcy, medical bills frequently represent the tipping point.

Bankruptcy discharges most medical debt. Chapter 7 bankruptcy eliminates it entirely. Chapter 13 creates a repayment plan that often pays medical creditors pennies on the dollar.

But bankruptcy has serious consequences beyond debt relief. Credit damage lasts seven to ten years. Access to credit becomes limited and expensive. Some employers check credit reports during hiring.

Bankruptcy should be a last resort after exhausting payment plans, financial assistance, and negotiation. It solves the debt problem but creates others.

Real Talk: Community Experiences

Community discussions reveal what official guidance sometimes misses.

People share experiences about medical bills that went unpaid for years with no consequences. Others report aggressive collection efforts for bills under $200. The reality varies wildly based on provider, location, and debt amount.

Some healthcare providers write off small debts rather than pursuing collection. Others immediately send everything to collection agencies regardless of amount. There’s no universal approach.

What remains consistent across experiences: communication matters. People who ignored bills completely faced harsher consequences than those who called providers, explained financial situations, and proposed solutions—even if those solutions fell short of full immediate payment.

Frequently Asked Questions

No. As of April 2023, medical debts under $500 do not appear on credit reports regardless of collection status. This protection applies to all three major credit bureaus—Equifax, Experian, and TransUnion.

Collection timeframes vary by state but typically range from three to ten years. This statute of limitations determines how long creditors can sue for unpaid debt. After the statute expires, debt becomes legally uncollectible, though it may still exist.

Emergency rooms cannot refuse treatment based on unpaid bills or inability to pay. Federal law requires emergency medical screening and stabilization regardless of payment status. For non-emergency care, providers can refuse service for unpaid bills from previous visits.

Hospital billing departments work for the original provider and can arrange payment plans, apply financial assistance, and correct billing errors. Collection agencies purchase debt for pennies on the dollar and focus solely on collection. Once debt moves to collections, the hospital typically can’t help anymore.

Yes. Collection agencies often accept 30% to 50% of the original balance as settlement. They purchased the debt for a fraction of face value, so reduced settlements still generate profit. Always get settlement terms in writing before making any payment.

Medical collections can affect lending decisions, but their impact has decreased. Newer credit scoring models weigh medical debt less heavily than other collections. Paid medical collections have minimal impact. Lenders also manually review credit reports and may disregard medical debt depending on overall creditworthiness.

Request an itemized statement and explanation of benefits from the insurance company. Verify the provider, service dates, and procedures match actual care received. Contact the provider’s billing department directly to confirm the bill’s legitimacy. Never pay a questionable bill without verification—medical billing errors are common.

Taking Action on Unpaid Medical Bills

Medical debt creates stress, but it’s not insurmountable.

The consequences of non-payment range from collection calls to lawsuits and wage garnishment. But between the initial bill and those severe outcomes lies substantial opportunity for resolution.

New federal protections under the No Surprises Act prevent many unexpected bills from occurring in the first place. The 2023 credit reporting changes shield most people from immediate credit damage. Financial assistance programs eliminate or reduce bills for those who qualify.

The key is action. Ignoring medical bills increases the likelihood of worst-case outcomes. Engaging with providers, verifying charges, exploring assistance, and negotiating payment creates pathways to resolution that cost far less than collection fees, interest, and legal judgments.

Medical bills arrive when health is already compromised. Financial crisis shouldn’t compound medical crisis. Know the protections, understand the timeline, and use available tools to manage medical debt before it manages you.

Check bills for accuracy. Apply for financial assistance. Negotiate when appropriate. Set up payment plans before collection starts. Document everything. Know your rights under federal and state law.

Those steps won’t eliminate medical debt entirely, but they prevent unpaid bills from becoming financial catastrophes.