Quick Summary: Failing to pay student loans triggers severe consequences including damaged credit, wage garnishment up to 15%, tax refund seizures, and potential lawsuits. Federal loans enter default after at least 270 days (roughly 9 months) of non-payment, while private loans can default sooner based on lender terms. However, multiple repayment options exist to avoid default, including income-driven plans, deferment, and loan rehabilitation programs.

Student loan debt has become second only to mortgage debt in the United States, with borrowers owing over $1.7 trillion in student loans. But what actually happens when payments stop?

The answer isn’t simple. Federal and private student loans follow different rules, timelines, and collection processes. And the consequences can range from minor credit dings to serious financial devastation.

Here’s the thing though—defaulting on student loans doesn’t happen overnight. There’s a progression from missed payments to full default, with multiple opportunities to correct course along the way.

Understanding the Timeline: From Missed Payment to Default

Not all missed payments immediately equal disaster. The timeline matters significantly.

Federal Student Loan Default Timeline

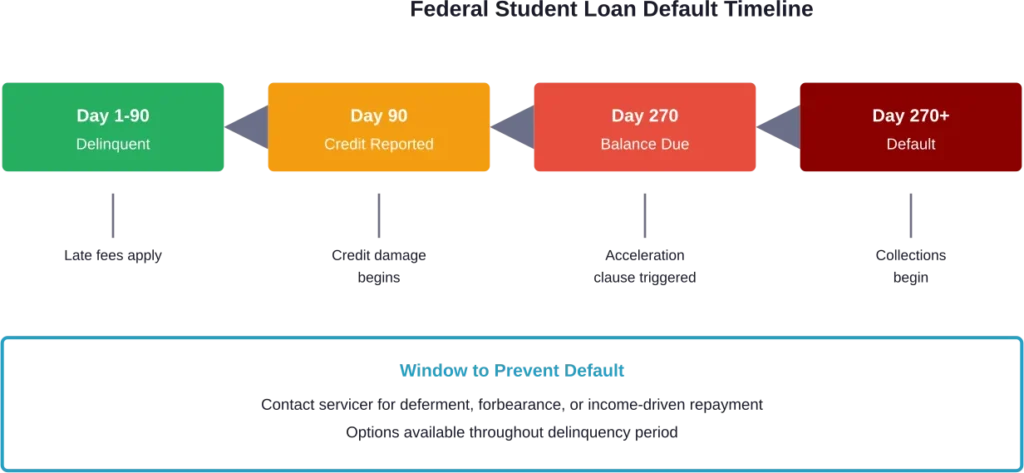

According to the U.S. Department of Education, federal student loans enter default status after at least 270 days of non-payment. That’s roughly 9 months of missed payments before the loan officially defaults.

Before reaching default, the loan goes through delinquency stages:

- Day 1-90: The loan becomes delinquent on day one of a missed payment. Late fees may apply, and servicers begin sending payment reminders.

- Day 90: The loan servicer reports the delinquency to credit bureaus. Credit scores start taking hits.

- Day 270: The entire loan balance may be declared due immediately, though this varies by servicer.

- Day 270+: The loan enters default status. This triggers aggressive collection actions.

Private Student Loan Default Timeline

Private lenders set their own rules. Some private student loans can default after just 120 days of non-payment. Others may declare a loan in default after a single missed payment, depending on the terms in the promissory note.

Check the loan agreement for specific terms. Private lenders aren’t bound by the federal 270-day timeline.

Credit Score Devastation

The credit damage from unpaid student loans is severe and long-lasting.

Once a loan servicer reports delinquency to credit bureaus (typically at 90 days), credit scores can drop 50-100 points or more. Default status brings even worse damage.

This affects far more than just borrowing ability. Bad credit impacts:

- Apartment rental applications (many landlords check credit)

- Employment opportunities (some employers run credit checks)

- Insurance rates (auto and home insurance premiums increase with poor credit)

- Security clearances (delinquent debt can disqualify applicants)

- Cell phone plans (carriers may require larger deposits)

The delinquency remains on credit reports for seven years from the date of the first missed payment. Even after repaying or rehabilitating the loan, the damage persists for years.

Wage Garnishment and Involuntary Collections

Here’s where federal student loans become particularly aggressive.

According to Federal Student Aid, if borrowers haven’t made a payment for more than 360 days and don’t take action to resolve default status, the government can withhold money through involuntary collections such as wage garnishment. The Department of Education can garnish up to 15% of disposable income through Administrative Wage Garnishment (where the government automatically collects up to 15% of your paycheck).

No court order required. The Department of Education notifies employers directly, and paychecks get automatically reduced.

Recent Collections Updates

The U.S. Department of Education announced in April 2025 that it would resume collections of defaulted federal student loan portfolios on May 5, 2025, after pausing collections since March 2020. However, in January 2026, the Department delayed implementation of involuntary collections, including Administrative Wage Garnishment and the Treasury Offset Program, to enable major student loan repayment reforms.

This means collections activity remains in flux. The situation can change as policy evolves.

Treasury Offset Program

Beyond wage garnishment, the government can seize tax refunds through the Treasury Offset Program. Expecting a $3,000 tax refund? The Department of Education can intercept the entire amount and apply it to the defaulted loan balance.

According to the Consumer Financial Protection Bureau, the government can also offset Social Security benefits for defaulted student loans. This has become increasingly common as older borrowers represent a growing share of the student loan portfolio. The number of student loan borrowers ages 62 and older increased by 59 percent from 1.7 million in 2017 to 2.7 million in 2023.

Social Security offsets can push borrowers into poverty, undermining the purpose of the Social Security program itself.

| Collection Method | Federal Loans | Private Loans |

|---|---|---|

| Wage Garnishment | Up to 15% without court order | Requires lawsuit and court judgment |

| Tax Refund Seizure | Yes, through Treasury Offset Program | No |

| Social Security Offset | Yes, for borrowers 62+ | No |

| Professional License Revocation | Varies by state | Varies by state |

| Lawsuit Filing | Less common (other methods available) | Common collection strategy |

Private Student Loan Consequences

Private lenders can’t garnish wages or seize tax refunds without going to court first. But that doesn’t mean they’re harmless.

According to the Consumer Financial Protection Bureau, private lenders can report defaults to consumer reporting agencies, harming credit scores. They may also take different actions to collect the debt.

Lawsuits and Judgments

Private lenders frequently file lawsuits to collect on defaulted student loans. Once they obtain a court judgment, they can:

- Garnish wages (percentage varies by state law)

- Place liens on property

- Freeze bank accounts

- Seize assets

The statute of limitations on private student loans varies by state, typically ranging from three to ten years. But if the lender obtains a judgment before the statute expires, that judgment can last much longer and be renewed.

Collection Agency Harassment

Many private lenders sell defaulted debt to collection agencies. These agencies have gained notoriety for aggressive tactics.

The Consumer Financial Protection Bureau took action in December 2024 against Performant Recovery, Inc. for unlawful student loan debt collection practices. The CFPB found that Performant deliberately delayed borrowers’ loan rehabilitation processes, generating fees for itself while costing individual borrowers thousands of dollars. As a manager explained to agents, “[W]e want them to mail all documents. Remember the whole objective is to DELAY, DELAY, DELAY.”

Collection agencies must follow the Fair Debt Collection Practices Act, which prohibits harassment, false statements, and unfair practices. But violations remain common.

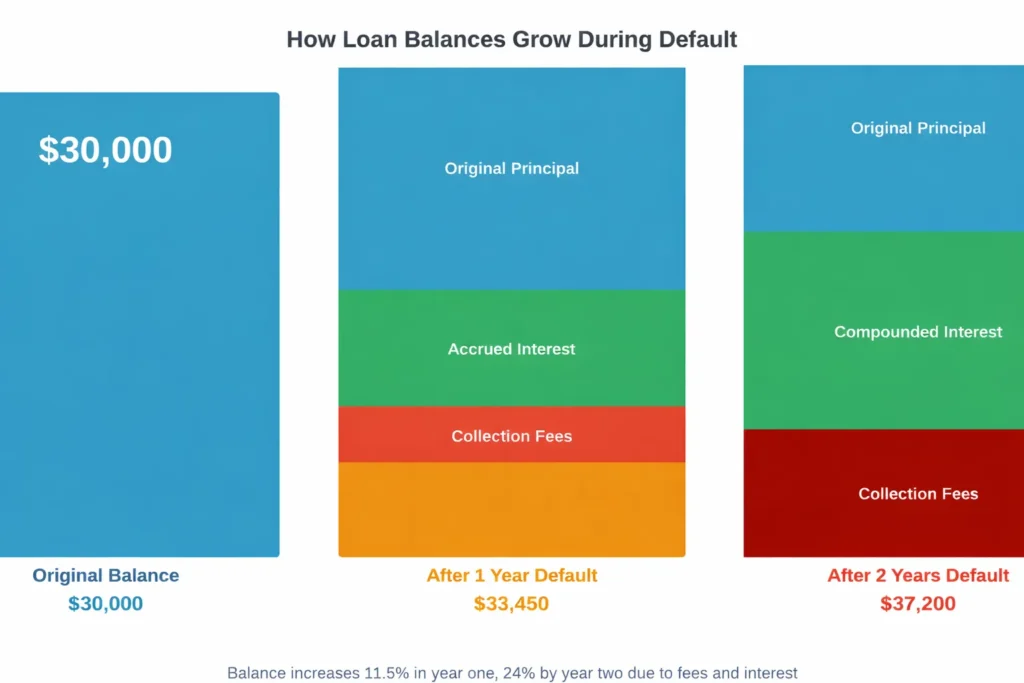

Your Loan Balance Grows Significantly

Non-payment doesn’t freeze the debt. It makes it worse.

Late fees accumulate quickly. Interest continues accruing on both federal and private student loans, compounding on the unpaid balance.

Collection costs get added to the balance. For federal loans, collection fees can be up to 18.5% of the principal and interest owed. A $30,000 defaulted loan can suddenly become $35,550 once collection costs are factored in.

This creates a vicious cycle. The growing balance becomes increasingly unmanageable, making repayment even more difficult.

Impact on Cosigners

Cosigners face identical consequences when the primary borrower defaults.

According to the Consumer Financial Protection Bureau, the student is the primary borrower with responsibility to pay back the loan, but cosigners have equal responsibility for repaying the loan if the student doesn’t. If the primary borrower defaults on the loan, it impacts the cosigner’s credit.

Any late or missed payments are reflected on both credit reports. This means:

- Parents who cosigned can see their credit scores tank

- Cosigners face wage garnishment and lawsuits

- Retirement savings and Social Security benefits become vulnerable

- Family relationships suffer tremendous strain

Some private loans include an auto-default clause triggered by the cosigner’s financial changes (job loss, bankruptcy, or even death). These clauses can force immediate full repayment even if the primary borrower has been making on-time payments.

Professional and Legal Consequences

Some states can revoke or suspend professional licenses for defaulted student loans. This affects healthcare workers, lawyers, teachers, and other licensed professionals.

Security clearances can be denied or revoked. Federal agencies view unresolved debt as a potential security risk, affecting military personnel and government contractors.

In extreme cases, borrowers have faced arrest warrants for failing to appear in court-ordered collection proceedings. These aren’t arrests for owing debt itself (debtors’ prisons are unconstitutional), but for contempt of court when borrowers ignore court summons.

What Student Loans Won’t Do

Despite the serious consequences, some commonly feared outcomes rarely or never happen:

Student loans almost never disappear through bankruptcy. Federal student loans are nearly impossible to discharge in bankruptcy unless borrowers can prove “undue hardship,” an extremely high legal standard. Private student loans face similar barriers.

Lenders can’t seize personal property without a court judgment. For federal loans, the government uses administrative collection powers instead. For private loans, lenders must sue and win before taking assets.

Student loans don’t expire. There’s no statute of limitations on federal student loans. Private loans have statutes that vary by state, but lenders can still attempt collection (they just can’t sue after the statute expires).

Options to Avoid Default

Now, this is where it gets interesting. Despite the grim consequences, multiple solutions exist to avoid default entirely.

Income-Driven Repayment Plans

Federal student loans offer income-driven repayment plans that cap monthly payments at a percentage of discretionary income. These include:

- Income-Based Repayment (IBR)

- Pay As You Earn (PAYE)

- Saving on a Valuable Education (SAVE)

- Income-Contingent Repayment (ICR)

For borrowers with low income relative to debt, payments can drop to $0 per month while still counting as on-time payments. After 20-25 years of qualifying payments, remaining balances may be forgiven.

Deferment and Forbearance

Deferment allows temporary suspension of payments for qualifying circumstances like unemployment, economic hardship, or returning to school. Interest may not accrue on subsidized federal loans during deferment.

Forbearance also pauses payments but interest continues accruing on all loan types. It’s available for financial difficulties, medical expenses, or other qualifying hardships.

Both options provide breathing room without triggering default.

Loan Consolidation

Federal loan consolidation combines multiple federal loans into a single Direct Consolidation Loan. This can:

- Simplify payments by creating a single monthly bill

- Provide access to income-driven repayment plans

- Remove loans from default status when combined with rehabilitation

However, consolidation may increase the total interest paid over the loan’s lifetime by extending the repayment period.

Loan Rehabilitation

For loans already in default, rehabilitation provides a path back to good standing. Borrowers make nine voluntary, reasonable, and affordable payments within ten consecutive months.

Once rehabilitation is complete:

- The default status is removed from credit reports

- Wage garnishment and Treasury offsets stop

- Access to deferment, forbearance, and income-driven plans is restored

The default notation disappears from credit reports, though the prior delinquencies before default remain for seven years.

Private Loan Negotiation

Private lenders may negotiate settlements or modified payment plans. Some borrowers successfully settle defaulted private loans for 40-60% of the balance.

Lenders would rather recover something than nothing. Negotiation works best when borrowers can offer a lump sum payment or demonstrate genuine financial hardship.

When to Contact Your Loan Servicer

The single most important action? Contact the loan servicer before missing payments.

Servicers can explain options, enroll borrowers in appropriate repayment plans, and prevent default before it starts. According to estimates from the Department of Education, only 38% of Direct Loan and Department-held Federal Family Education Loan Program borrowers are in repayment and current on their student loans, with almost 25% of the entire portfolio either in default or late-stage delinquency, indicating widespread challenges.

Ignoring the problem never works. Servicers have more flexibility to help borrowers who proactively reach out than those who disappear.

For federal loans, visit StudentAid.gov or contact the loan servicer directly. For private loans, check the lender’s website or monthly statement for contact information.

The Bottom Line

Not paying student loans triggers a cascade of consequences that can devastate financial health for years or even decades. Credit scores plummet. Wages get garnished. Tax refunds disappear. Cosigners suffer. The loan balance grows relentlessly.

But here’s what matters most: these consequences are largely preventable.

Income-driven repayment plans can reduce federal loan payments to affordable levels or even $0. Deferment and forbearance provide temporary relief during hardship. Rehabilitation can restore defaulted loans to good standing.

The difference between financial disaster and manageable repayment often comes down to taking action early. Borrowers who contact servicers when trouble starts have dramatically better outcomes than those who ignore mounting debt.

Student loan debt is real. The consequences are severe. But solutions exist at every stage—from preventing the first missed payment to recovering from default.

The worst decision? Doing nothing. The best decision? Reaching out for help before missing that first payment.

Frequently Asked Questions

Federal student loans enter default after at least 270 days (roughly 9 months) of non-payment. Private student loans can default much sooner, sometimes after just 120 days or even a single missed payment, depending on the loan agreement terms.

Federal student loans can place a lien on property without a court order, though this is relatively uncommon. Private student loan lenders must sue and obtain a court judgment before placing liens on real estate or other assets.

Yes. The federal government can garnish up to 15% of disposable income for defaulted federal student loans without a court order through Administrative Wage Garnishment. Private lenders must sue and win a court judgment before garnishing wages, with the percentage limited by state law.

No. Student loans do not disappear after seven years. While negative information on credit reports typically falls off after seven years, the debt itself remains. Federal student loans have no statute of limitations and can be collected indefinitely. Private loans have statutes of limitations that vary by state, but the debt still exists even if the lender can no longer sue.

No. Debtors’ prisons are unconstitutional in the United States, and no one can be arrested simply for owing student loan debt. However, borrowers can face arrest for contempt of court if they ignore court summons related to collection lawsuits.

Student loan default causes severe credit damage. Delinquency gets reported to credit bureaus at 90 days, potentially dropping scores by 50-100+ points. Default status causes additional damage. The delinquency remains on credit reports for seven years from the first missed payment, even after repaying or rehabilitating the loan.

Yes, through loan rehabilitation. After making nine voluntary, reasonable, and affordable payments within ten consecutive months, the default status is removed from credit reports. However, delinquencies that occurred before the loan entered default remain on the credit report for seven years.