Quick Summary: Not signing up for Medicare at 65 can result in permanent late enrollment penalties that increase monthly premiums for Part B and Part D. However, individuals with qualifying employer coverage or their spouse’s employer plan may delay enrollment without penalties. Understanding enrollment periods and exceptions is crucial to avoid unnecessary costs.

Turning 65 marks a critical milestone in healthcare planning. But is Medicare enrollment mandatory the moment the birthday candles are blown out?

The answer isn’t straightforward. For some, delaying enrollment triggers financial penalties that last a lifetime. For others, waiting makes perfect sense.

The Late Enrollment Penalty Reality

According to Medicare.gov, failing to enroll during the Initial Enrollment Period can result in permanent late enrollment penalties. These aren’t temporary fees—they stick with beneficiaries for as long as they have Medicare coverage.

Here’s what that looks like in practice. The Part B late enrollment penalty adds 10% to the monthly premium for each 12-month period of delayed enrollment. For example, someone who waits three years past their Initial Enrollment Period faces a 30% premium increase that continues for life.

Part D prescription drug coverage carries its own penalty calculation. The penalty equals 1% of the national base beneficiary premium multiplied by the number of months without creditable coverage. As the Centers for Medicare & Medicaid Services notes, this penalty continues for the entire duration of Part D enrollment.

When Delaying Makes Sense

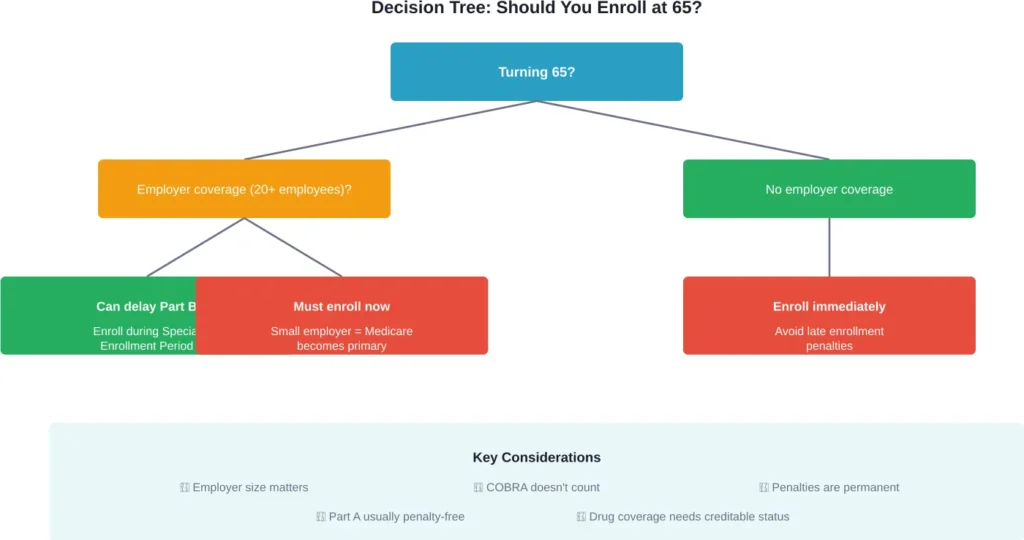

Not everyone faces penalties for skipping enrollment at 65. The key factor? Employer-sponsored health insurance.

According to KFF, individuals covered by employer group health plans—either through their own job or a spouse’s employment—can delay Medicare Part B enrollment without penalty. The employer size requirement (20 or more employees) applies to determining whether Medicare or the employer plan is primary payer.

This exception applies only to active employment coverage. COBRA, retiree health plans, and individual marketplace plans don’t qualify as creditable coverage for delaying Part B.

Part A hospital insurance operates differently. Most people receive premium-free Part A, and there’s typically no penalty for delayed enrollment. But declining Part A while keeping employer coverage requires careful consideration of Health Savings Account eligibility.

| Coverage Type | Can Delay Part B? | Penalty Risk |

|---|---|---|

| Employer plan (20+ employees) | Yes | None if enrolled during Special Enrollment Period |

| Employer plan (under 20 employees) | No | Penalties apply for late enrollment |

| COBRA coverage | No | Penalties apply—COBRA isn’t creditable |

| Retiree health insurance | No | Penalties apply unless specifically creditable |

| Marketplace/ACA plan | No | Penalties apply |

Understanding Enrollment Windows

The Initial Enrollment Period spans seven months: the three months before turning 65, the birth month, and three months after. Missing this window without qualifying for an exception creates problems.

For those with employer coverage, the Special Enrollment Period provides an eight-month window after employment ends or group coverage terminates—whichever comes first. This protection only applies if the employer coverage was creditable.

According to SSA sources, individuals receiving Social Security benefits will be automatically enrolled in Medicare Parts A and B starting the month they turn 65.

Coverage Gaps and Access Issues

Beyond financial penalties, delayed enrollment creates tangible coverage gaps. The General Enrollment Period runs from January 1 to March 31 each year, but coverage doesn’t start until July 1.

That means someone who misses their Initial Enrollment Period and lacks qualifying employer coverage must wait until the next General Enrollment Period (January 1 to March 31) to enroll—with coverage beginning July 1. This can create a significant gap in coverage.

During this gap, healthcare costs fall entirely on the individual. Pre-existing conditions may also complicate access to Medigap supplemental insurance. According to KFF research published in October 2024, beneficiaries in most states can be denied Medigap policies due to pre-existing conditions if they don’t enroll during their initial guaranteed issue period.

The Creditable Coverage Question

Drug coverage deserves special attention. Medicare Part D penalties apply when there’s a gap of 63 days or more without creditable prescription drug coverage after the Initial Enrollment Period ends.

Employer plans must notify employees annually whether their prescription coverage is creditable. Without this documentation, proving coverage status becomes difficult when enrolling in Part D later.

The Centers for Medicare & Medicaid Services requires plan sponsors to provide creditable coverage notices. Keeping these documents prevents disputes about penalty assessments down the road.

Frequently Asked Questions

If the employer has 20 or more employees, delaying Part B enrollment is penalty-free. Sign up during the Special Enrollment Period—eight months after employment or coverage ends. Employers with fewer than 20 employees require immediate Medicare enrollment since Medicare becomes the primary payer.

Generally no. According to Medicare.gov, late enrollment penalties are permanent. However, appeals are possible through Part D Quality Improvement Organizations if enrollment delays resulted from incorrect information from a plan or employer.

Yes. The Social Security Administration automatically enrolls anyone receiving Social Security benefits into Medicare Parts A and B starting the month they turn 65. To decline Part B, beneficiaries must actively opt out—but should carefully consider penalty implications.

Medicare enrollment, including Part A, ends Health Savings Account eligibility. Contributions made after Medicare coverage begins face tax penalties. Existing HSA funds remain accessible tax-free for qualified medical expenses.

No. Medicare enrollment isn’t legally mandatory. However, without qualifying employer coverage, delaying enrollment triggers permanent penalties and creates coverage gaps. Most people benefit from enrolling during their Initial Enrollment Period.

Employers and insurance plans provide annual creditable coverage notices. Keep these documents. They’re essential evidence when enrolling in Medicare later to avoid or appeal late enrollment penalties.

Yes, but it’s rarely advantageous. Most people receive premium-free Part A. Declining it only makes sense for those actively contributing to an HSA and covered by a high-deductible health plan through current employment.

Making the Right Decision

The decision to enroll in Medicare at 65 hinges on current coverage status. Those with qualifying employer coverage through large employers have flexibility. Everyone else faces financial consequences for delays.

Review employer plan size, confirm creditable coverage status for prescription drugs, and understand the enrollment windows. These steps prevent costly mistakes that follow beneficiaries for decades.

The Medicare.gov website provides personalized guidance based on specific situations. When in doubt, consult with the employer’s human resources department and contact Medicare directly at 1-800-MEDICARE before the Initial Enrollment Period closes.