Quick Summary: If you lack insurance but the other driver caused the accident, you can still pursue compensation by filing a claim against their insurance or suing them directly. However, driving uninsured exposes you to penalties including fines, license suspension, and potential counterclaims that may limit your recovery. Your options depend heavily on your state’s laws and whether the at-fault driver carries adequate coverage.

Getting into a car accident is stressful enough. But when you’re driving without insurance and someone else causes the crash? That’s a whole different level of complicated.

Here’s the thing though—not having insurance doesn’t automatically mean you forfeit your right to compensation. The situation depends on where you live, the specifics of the accident, and whether the at-fault driver has coverage.

This guide breaks down exactly what happens when you’re uninsured but not at fault, the legal consequences you might face, and your options for recovering damages.

The Legal Reality of Driving Without Insurance

Most states require drivers to carry minimum liability insurance. According to the National Association of Insurance Commissioners, auto insurance typically covers two basic areas: liability and property damage. These requirements exist to protect everyone on the road.

When you drive without meeting these requirements, you’re violating financial responsibility laws. And those violations come with consequences, regardless of who caused the accident.

Typical State Requirements

California laws, for example, require all drivers to have at least $15,000 in bodily injury liability for a single person injured in an accident and $30,000 for all parties involved. Property damage liability coverage minimum is $15,000 according to California law.

Other states have similar minimums. The specifics vary, but the principle remains constant: insurance isn’t optional.

| Coverage Type | California Minimum | Purpose |

|---|---|---|

| Bodily Injury (per person) | $15,000 | Covers medical costs for one injured person |

| Bodily Injury (per accident) | $30,000 | Total coverage for all injuries in one accident |

| Property Damage | $5,000 | Covers damage to vehicles and property |

Penalties for Driving Uninsured

The consequences of driving without insurance stack up quickly. Expect fines ranging from several hundred to thousands of dollars, depending on your state and whether this is a repeat offense.

License suspension is common. Your vehicle registration might be suspended too. Some states require SR-22 certificates—proof of financial responsibility—before you can drive legally again.

But wait. These penalties apply even if the accident wasn’t your fault.

Can You Still Recover Compensation?

Real talk: yes, you can still pursue compensation when another driver causes an accident. Your lack of insurance doesn’t erase their liability.

The at-fault driver’s insurance company is responsible for covering damages their policyholder caused. That includes your medical bills, vehicle repairs, lost wages, and pain and suffering.

Filing a Claim Against the At-Fault Driver

Start by filing a third-party claim with the at-fault driver’s insurance company. Document everything: the accident scene, injuries, property damage, witness statements, and police reports.

The insurance company will investigate the claim. They’ll review evidence, assess fault, and determine the value of damages. This process takes time—sometimes weeks or months.

Here’s where it gets tricky. Insurance companies know you’re driving illegally. They might use that against you, arguing you contributed to the accident or shouldn’t receive full compensation.

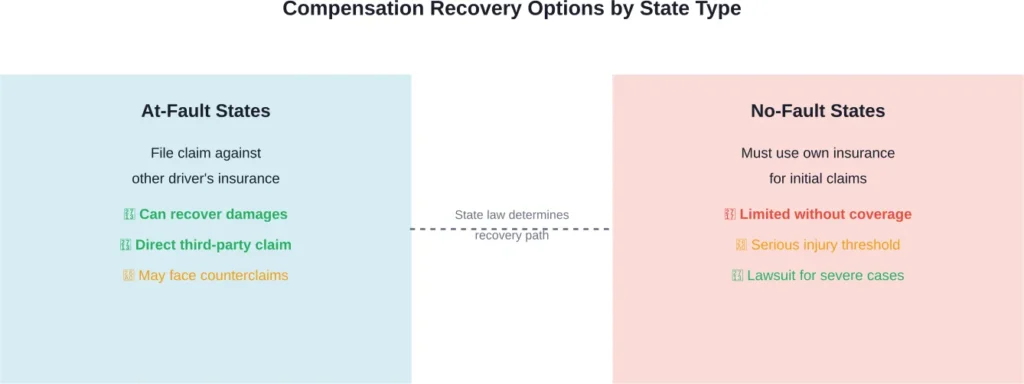

State Fault Systems Matter

Your recovery options depend heavily on whether you live in an at-fault or no-fault state.

In at-fault states, the driver who caused the accident pays for damages. Even without insurance, you can pursue the at-fault driver’s coverage.

Some states follow comparative negligence rules. In some states with comparative negligence rules, every driver is liable only for the portion of damages that matches their share of fault. If you’re found 10% responsible and the other driver is 90% at fault, you can still recover 90% of damages.

No-fault states complicate things. These states require drivers to file claims through their own insurance first, regardless of who caused the accident. Without insurance, you might be barred from recovering anything except in cases of serious injury.

When the At-Fault Driver Is Also Uninsured

Sound familiar? Two uninsured drivers in one accident creates a financial nightmare.

Without the at-fault driver’s insurance to tap into, your options narrow dramatically. You can sue the other driver directly for damages, but collecting on a judgment is another story. Many uninsured drivers lack the assets to pay substantial damages.

If both drivers lack insurance and the injured party has no household member with coverage, some states provide victim assistance programs or indemnification funds.

Uninsured Motorist Coverage—When Others Have It

Here’s an ironic twist: if a family member you live with carries uninsured motorist coverage on their policy, you might be covered even though you don’t have your own insurance.

Uninsured motorist coverage protects policyholders when they’re hit by drivers without insurance. Some policies extend this protection to household members, even when they’re driving a different vehicle or are pedestrians.

Check with family members about their coverage. This could be your best path to compensation.

Steps to Take After an Accident Without Insurance

Okay, so what about the immediate aftermath? The actions taken right after the crash significantly impact your ability to recover damages.

At the Scene

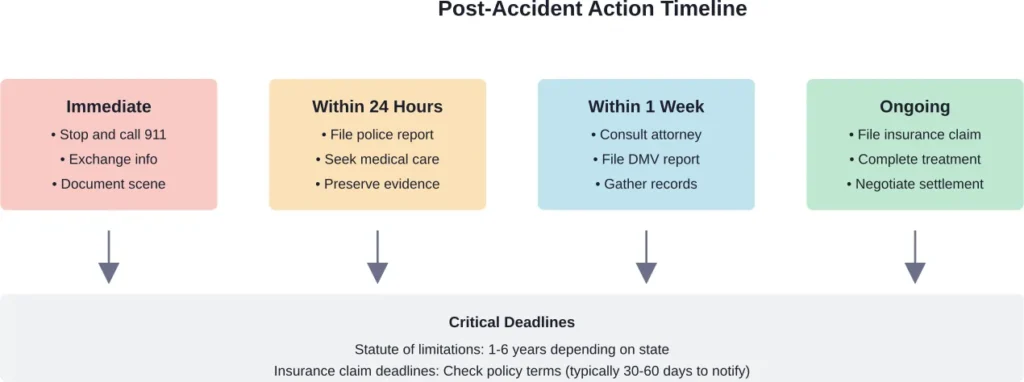

Stop immediately. Leaving the scene compounds your legal troubles exponentially. Call 911 if anyone is injured. Even minor injuries deserve medical attention—and documentation.

Exchange information with the other driver: names, contact details, vehicle information, and insurance details. Take photos of the accident scene, vehicle damage, road conditions, traffic signs, and visible injuries.

Get witness contact information. Their statements can be crucial when determining fault.

Report the Accident

File a police report. Many states require this when damage exceeds a certain threshold—often $1,000—or when anyone is injured. The police report becomes key evidence in your claim.

Notify the Department of Motor Vehicles if required by your state. California, for instance, requires filing form MV-104 when damage exceeds $1,000 or anyone sustains injury.

Document Everything

Keep detailed records of all accident-related expenses: medical bills, repair estimates, towing fees, rental car costs, and lost wages. These documents support your damage claim.

Photograph your injuries as they heal. Medical records should document treatment, diagnosis, prognosis, and recommended future care.

Consult a Lawyer

Navigating an accident claim without insurance gets complicated quickly. Insurance companies have legal teams protecting their interests. Having an experienced attorney levels the playing field.

Many car accident lawyers work on contingency—they only get paid if you recover compensation. Initial consultations are often free.

Potential Legal Challenges You’ll Face

That said, not having insurance doesn’t just limit your options—it opens you up to counterclaims and legal defenses that can reduce or eliminate your recovery.

The At-Fault Driver Might Countersue

Even when the other driver caused the accident, they might file a counterclaim against you. They’ll argue you contributed to the accident through negligent driving, and that your lack of insurance violated the law.

In states with comparative negligence rules, any percentage of fault assigned to you reduces your recovery proportionally. If you’re found 20% at fault, your compensation drops by 20%.

Some states follow contributory negligence rules—even harsher. In these jurisdictions, any fault on your part, even 1%, can bar you from recovering anything.

Insurance Companies Will Use Your Uninsured Status

Insurance adjusters know you’re vulnerable. They’ll use your lack of insurance as leverage during settlement negotiations, suggesting you don’t deserve full compensation because you broke the law.

This is a negotiation tactic. Your legal violation doesn’t erase the other driver’s liability. But it does make the negotiation more difficult.

Limited Damage Recovery in Some States

Certain states restrict what uninsured drivers can recover. Some bar uninsured motorists from claiming non-economic damages like pain and suffering, limiting recovery to medical expenses and lost wages only.

These restrictions vary by state. An attorney familiar with local laws can explain exactly what applies in your jurisdiction.

Options Beyond Insurance Claims

When the at-fault driver’s insurance doesn’t provide adequate compensation—or when they don’t have insurance either—consider these alternatives.

Filing a Personal Injury Lawsuit

Taking the at-fault driver to court is always an option. A lawsuit allows you to pursue full compensation for all damages: medical costs, property damage, lost income, and pain and suffering.

The challenge? Lawsuits take time and money. You’ll need an attorney, and the case might take months or years to resolve. Plus, winning a judgment doesn’t guarantee payment if the defendant lacks assets.

Payment Plans and Settlements

Many cases settle before trial. Structured settlements or payment plans can work when the at-fault driver has limited resources. Getting some compensation over time beats getting nothing.

Health Insurance and Medical Payments

Use your health insurance to cover immediate medical expenses. Some health plans have subrogation clauses—they’ll seek reimbursement from any settlement you receive later.

If you have medical payments coverage on another insurance policy—homeowners or renters insurance, for example—check whether it applies to accident injuries.

Getting Insurance After an Accident

Look, driving without insurance is illegal and financially risky. After an accident—especially when you’re at fault—getting coverage becomes even more important and more expensive.

Insurance companies consider uninsured drivers high-risk. Expect higher premiums, possibly in the high-risk insurance pool. Some insurers won’t cover drivers with recent uninsured accidents at all.

You might need to file an SR-22 certificate—proof of financial responsibility—before your license is reinstated. This certificate must stay on file for several years, and any lapse triggers immediate license suspension.

| Consequence | Typical Duration | Financial Impact |

|---|---|---|

| License Suspension | 30 days to 1 year | Reinstatement fees $100-$500 |

| SR-22 Requirement | 3-5 years | Increased premiums 50-100% |

| Fines | One-time | $500-$5,000+ depending on state |

| Vehicle Impound | Until proof of insurance | $200-$1,000+ storage fees |

Prevention: Why Insurance Matters

The National Association of Insurance Commissioners emphasizes that auto insurance requirements exist to protect all road users. According to their guidance, insurance typically includes comprehensive coverage for damages from fire, theft, weather, or animal collisions, plus collision coverage for repair costs.

If you’re struggling to afford insurance, look into low-cost state programs. Many states offer reduced-premium insurance for low-income drivers. It’s still cheaper than the fines, legal fees, and financial risk of driving uninsured.

Frequently Asked Questions

You won’t typically be arrested solely for lacking insurance, but you’ll face citations and fines. Penalties include possible license suspension, vehicle impound, and mandatory SR-22 filing. The accident fault doesn’t change these consequences—they apply to any uninsured driver involved in a reported accident.

Yes, in most states. The at-fault driver’s liability coverage should pay for damages they caused, regardless of your insurance status. However, their insurance company may aggressively fight the claim or offer low settlements, knowing you’re in a legally vulnerable position. Having an attorney significantly improves your chances of fair compensation.

Absolutely. You can file a personal injury lawsuit against the at-fault driver in civil court. This is often the best option when the driver lacks insurance or carries minimal coverage. The challenge is collecting on any judgment if the defendant doesn’t have assets or income to garnish.

Hit-and-run accidents complicate recovery significantly. Without identifying the at-fault driver, you can’t file a claim against their insurance. Some states have uninsured motorist funds or victim compensation programs that may help. If a family member has uninsured motorist coverage, check whether it extends to hit-and-run situations.

Statutes of limitations vary by state, ranging from one to six years for personal injury claims. Insurance policies often require notification within 30-60 days of the accident. Don’t wait—evidence deteriorates, witnesses disappear, and missing deadlines can forfeit your right to compensation entirely.

It depends on state laws. Some states allow uninsured drivers to recover all damages, while others restrict recovery to economic damages only, excluding pain and suffering. Your uninsured status might be used to argue comparative fault, reducing your total recovery proportionally. State-specific rules make consulting a local attorney essential.

Yes, but it’s significantly harder. You can sue the at-fault driver directly, but collecting payment depends on their assets and income. Some states have victim compensation funds that may provide limited assistance. Check whether any household members have uninsured motorist coverage that might extend to you.

Moving Forward After an Uninsured Accident

Driving without insurance creates serious legal and financial risks—even when someone else causes the accident. But it doesn’t automatically eliminate your right to fair compensation.

The key is acting quickly and strategically. Document everything, understand your state’s specific laws, and don’t try to navigate this alone. Insurance companies have legal teams working to minimize payouts. Having experienced legal representation levels the odds.

Get insurance as soon as possible. The temporary cost savings of going uninsured pale compared to the financial devastation one accident can cause. Shop around for affordable coverage, investigate state low-cost programs, and make insurance a non-negotiable part of vehicle ownership.

If you’re currently dealing with an accident where you lacked insurance but the other driver was at fault, consult with a personal injury attorney immediately. Many offer free consultations and work on contingency, meaning you pay nothing unless they recover compensation for you.

Your uninsured status complicates things, but it doesn’t make your case hopeless. With the right legal guidance and a thorough understanding of your options, recovering fair compensation remains possible.