Quick Summary: Filing taxes late triggers financial penalties that escalate monthly, but the consequences vary dramatically based on whether you owe money or expect a refund. According to the IRS, the failure-to-file penalty reaches 5% of unpaid taxes per month up to 25%, while those expecting refunds face no penalties—though delayed refunds and potential loss of credits create their own problems.

Tax season doesn’t wait for anyone. The April 15 deadline arrives whether you’re ready or not.

But life happens. Documents go missing. Accountants get backed up. Health emergencies derail plans. And suddenly, the filing deadline passes without a submitted return.

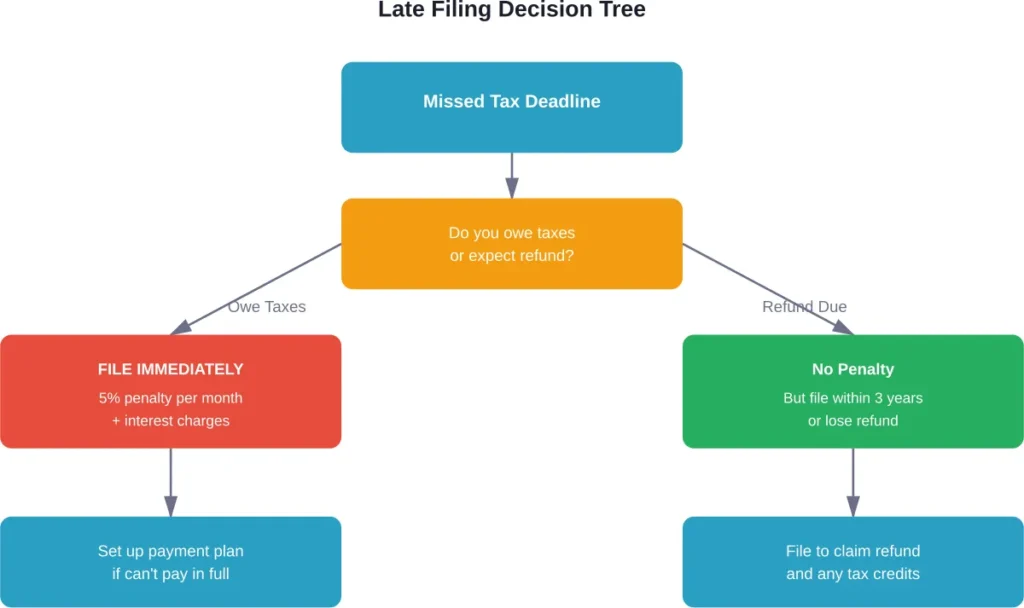

Here’s the thing though—the consequences of filing late depend entirely on one critical factor: whether you owe money or expect a refund. The difference between these two scenarios means the gap between crippling penalties and minor inconvenience.

The Two-Penalty System: How the IRS Punishes Late Filers

The IRS doesn’t mess around with a single penalty structure. Instead, they’ve created a two-pronged system that can stack penalties on top of each other.

According to the Internal Revenue Service, late filers potentially face two separate penalties: the failure-to-file penalty and the failure-to-pay penalty. Both can apply simultaneously, compounding the financial damage.

Failure-to-File Penalty: The Bigger Threat

This penalty kicks in the moment your return becomes late—even one day past the deadline without an approved extension.

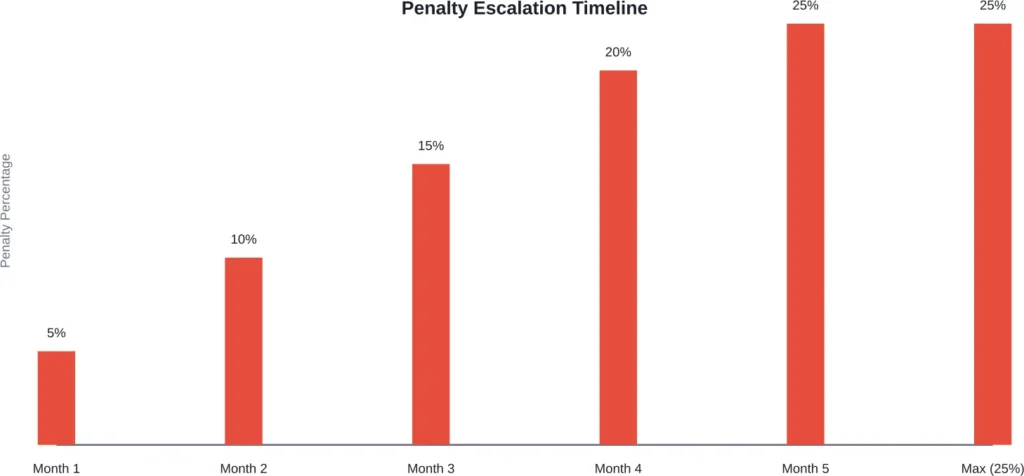

The calculation works like this: 5% of the unpaid tax balance for each month (or partial month) the return remains unfiled. That percentage applies to the tax required to be shown on the return, minus any tax paid on time (including withholding credits and estimated payments) and available refundable credits.

The penalty maxes out at 25% of the unpaid tax. So if you owe $10,000 and file five months late, you’re looking at a $2,500 penalty just for missing the deadline.

But there’s a twist. For returns filed more than 60 days late, the IRS imposes a minimum penalty. For returns due after December 31, 2025, that minimum stands at $525—even if the calculated percentage would be lower.

| Return Due Date | Minimum Penalty (60+ Days Late) |

|---|---|

| After 12/31/2025 | $525 |

| 01/01/2025 to 12/31/2025 | $510 |

| 01/01/2024 to 12/31/2024 | $485 |

| 01/01/2023 to 12/31/2023 | $450 |

Failure-to-Pay Penalty: The Smaller (But Still Painful) Hit

This penalty applies when you don’t pay the tax owed by the deadline, even if you filed on time.

The rate? Just 0.5% of the unpaid tax per month, capping at 25%. Seems modest compared to the failure-to-file penalty, right?

That’s exactly why the IRS reduces the failure-to-file penalty when both apply simultaneously. When both penalties run concurrently, the failure-to-file drops to 4.5% per month (from 5%), and the failure-to-pay adds its 0.5%. The combined rate stays at 5% monthly until the failure-to-file maxes out at 25%.

After that point, only the failure-to-pay penalty continues accruing at 0.5% monthly until it reaches its own 25% cap.

Interest Charges: The Hidden Cost That Never Stops

Penalties represent just part of the financial damage. Interest accrues separately on both the unpaid tax and the penalties themselves.

According to the IRS, interest accrues on any unpaid tax from the due date of the return (without any extensions) until the date of payment in full. The interest rate is determined quarterly and is the federal short-term rate plus 3 percent.

Unlike penalties, interest doesn’t cap. Interest compounds daily and continues until the balance is paid in full.

So even if you’ve maxed out the 25% failure-to-file penalty and the 25% failure-to-pay penalty, interest keeps adding to the balance. Over years, this can substantially inflate the total amount owed.

What Happens When You’re Owed a Refund

Here’s where things get interesting. If the IRS owes you money instead of the other way around, the penalty calculation changes completely.

No failure-to-file penalty applies when a refund is due. None. The IRS doesn’t penalize taxpayers for being late to claim money the government already owes them.

But that doesn’t mean filing late comes without consequences. Refunds only remain claimable for three years from the original due date. File after that window closes, and the money becomes property of the U.S. Treasury—permanently.

Additionally, delayed filing postpones the refund payment. That money could have been earning interest in a savings account or invested. The opportunity cost adds up, especially with larger refunds.

Some taxpayers also miss out on refundable credits like the Earned Income Tax Credit or Additional Child Tax Credit by filing late. These credits can be worth thousands of dollars, making timely filing financially critical even when no penalties apply.

Filing Extensions: The Free Pass Most People Ignore

The IRS provides a straightforward mechanism to avoid failure-to-file penalties: request an extension.

Filing Form 4868 before the April 15 deadline grants an automatic six-month extension to October 15. No explanation required. The IRS approves virtually every extension request.

But here’s the catch—extensions delay the filing deadline, not the payment deadline. Any tax owed still needs to be paid by the original due date (April 15) to avoid failure-to-pay penalties and interest.

That said, the failure-to-pay penalty (0.5% monthly) inflicts far less damage than the failure-to-file penalty (5% monthly). Requesting an extension and paying what you can by the original deadline minimizes penalties even if the full balance remains unpaid.

How to Request an Extension

Filing electronically through tax software or the IRS Free File system represents the fastest method. Paper Form 4868 works too, but processing takes longer.

Extensions must be filed by the original deadline to be valid. Filing for an extension on April 16 doesn’t help—the failure-to-file penalty already started accruing.

Past Due Returns: What to Do When You’ve Already Missed the Deadline

So the deadline passed. No extension was filed. The return remains incomplete.

Now what?

File immediately. According to the Taxpayer Advocate Service, filing late remains infinitely better than not filing at all. Every day that passes adds more penalties and interest to the balance.

Past due returns get filed the same way and to the same location as on-time returns. If the IRS has already sent a notice about the late filing, send the return to the address specified on that notice instead.

When You Can’t Pay the Full Amount

Inability to pay shouldn’t prevent filing. File the return even if the bank account sits at zero.

The IRS offers several payment options for taxpayers who can’t pay in full:

- Installment agreements: Monthly payment plans spread the balance over time, making large tax bills manageable

- Offers in compromise: Settle the debt for less than the full amount in specific circumstances

- Currently not collectible status: Temporarily pause collection efforts due to financial hardship

- Temporary payment delay: Short-term postponement while gathering funds

All these options require a filed return. The IRS won’t negotiate payment terms for unfiled returns.

Plus, filing stops the failure-to-file penalty immediately. The failure-to-pay penalty continues at its lower 0.5% monthly rate, but that’s far preferable to both penalties running simultaneously.

How the IRS Discovers Unfiled Returns

Some taxpayers wonder whether they can simply skip filing and hope the IRS doesn’t notice.

That strategy fails spectacularly.

Employers, banks, investment firms, and other institutions send income documents (W-2s, 1099s, etc.) to the IRS. The IRS computer systems match these against filed returns to identify discrepancies.

When income documents exist but no return appears, the IRS eventually sends notices demanding the return. Ignore those notices long enough, and the IRS files a substitute return on the taxpayer’s behalf—typically with minimal deductions and without claiming most credits, resulting in a higher tax bill than necessary.

The IRS can also levy bank accounts, garnish wages, and place liens on property to collect unpaid taxes from unfiled returns. The longer the delay, the more aggressive the collection efforts become.

Penalty Relief: When the IRS Might Waive Charges

Not all penalties are set in stone. The IRS provides several mechanisms for penalty reduction or elimination.

First-Time Penalty Abatement

Taxpayers with a clean compliance history may qualify for administrative penalty waiver. This applies to the failure-to-file and failure-to-pay penalties if the taxpayer has filed and paid on time for the previous three years and has no prior penalties.

Call the IRS and request first-time abatement once the return has been filed and any balance paid (or a payment plan established).

Reasonable Cause Relief

Extraordinary circumstances beyond a taxpayer’s control may justify penalty relief. Accepted reasons include:

- Death or serious illness of the taxpayer or immediate family member

- Natural disasters or civil disturbances

- Inability to obtain necessary records

- Incorrect written advice from the IRS

Documentation proving the reasonable cause strengthens the request. Medical records, death certificates, insurance claims, and dated correspondence all help establish the claim.

Statutory Exceptions

Combat zone service members may receive automatic extensions and penalty relief. Specific disaster declarations also trigger automatic relief for affected taxpayers.

The IRS publishes lists of qualified disasters and the associated relief provisions.

State Tax Consequences

Most states impose their own late filing penalties separate from federal penalties. State penalty structures vary widely.

Some states mirror federal penalty calculations. Others use flat fees or different percentage rates. A few states impose criminal penalties for willful failure to file.

State returns generally can’t be filed until after the federal return is complete, since many state tax calculations depend on federal adjusted gross income. Delay in filing the federal return automatically delays the state return, triggering state penalties even if the federal deadline was the cause of delay.

Check with the specific state tax authority to understand applicable penalties and available relief options.

Multiple Years of Unfiled Returns

Taxpayers sometimes fall behind on multiple years of returns. The situation feels overwhelming, leading to further avoidance.

But here’s the approach that works: file all missing returns as quickly as possible, starting with the most recent year.

The IRS typically focuses on the most recent six years of returns for compliance purposes. Filing older returns may also be necessary to claim refunds (within the three-year window) or to establish eligibility for payment plans.

Tax professionals can help reconstruct missing documentation using IRS transcripts, which show income reported by third parties even if the taxpayer lost the original documents.

When Professional Help Makes Sense

Complex tax situations benefit from professional assistance, especially when dealing with late filings and mounting penalties.

Enrolled agents, CPAs, and tax attorneys can:

- Prepare accurate returns using reconstructed records

- Negotiate penalty abatement and payment plans

- Represent taxpayers in IRS communications

- Identify deductions and credits to minimize tax owed

- Navigate offers in compromise and hardship status applications

The cost of professional help often pays for itself through penalty reduction and optimized tax positions.

| Scenario | Failure-to-File Penalty | Failure-to-Pay Penalty | Total Monthly Rate |

|---|---|---|---|

| Filed on time, didn’t pay | 0% | 0.5% | 0.5% |

| Filed late, paid on time | 5% | 0% | 5% |

| Filed late, didn’t pay | 4.5% | 0.5% | 5% |

| Owed refund, filed late | 0% | 0% | 0% |

| After failure-to-file maxes out | 0% (capped) | 0.5% | 0.5% |

Frequently Asked Questions

Criminal prosecution for late filing is extremely rare and typically reserved for cases involving fraud, tax evasion, or willful refusal to file over many years. According to the IRS, simple late filing due to disorganization or financial hardship results in civil penalties (fines), not criminal charges. However, deliberately evading taxes or filing false returns can lead to criminal prosecution.

No penalties apply when a refund is due, regardless of how late the return is filed. The IRS doesn’t penalize taxpayers for delaying their own refund. However, refunds can only be claimed within three years of the original due date. File after that window closes and the refund becomes uncollectible, permanently forfeited to the Treasury.

Filing Form 4868 before the April deadline provides an automatic six-month extension to October 15, completely eliminating the failure-to-file penalty if the return is submitted by the extended deadline. However, extensions don’t delay the payment deadline—any tax owed must still be paid by April 15 to avoid failure-to-pay penalties and interest charges.

Returns filed more than 60 days late face a minimum penalty of either $525 (for returns due after December 31, 2025) or 100% of the tax owed, whichever is less. This minimum applies even if the calculated monthly penalty (5% per month) would result in a lower amount. The minimum penalty increases annually based on inflation adjustments.

Yes, several penalty relief options exist. First-time penalty abatement is available for taxpayers with clean filing histories for the previous three years. Reasonable cause relief applies when circumstances beyond your control (serious illness, natural disaster, etc.) prevented timely filing. Documentation supporting the reasonable cause strengthens the request. Statutory exceptions provide automatic relief for combat zone service members and certain disaster victims.

File the return anyway. The IRS offers installment agreements (monthly payment plans), offers in compromise (settling for less than owed), currently not collectible status (temporary collection pause), and short-term payment delays. All options require a filed return. Filing immediately stops the failure-to-file penalty, leaving only the smaller failure-to-pay penalty accruing at 0.5% monthly instead of the combined 5% rate.

No statute of limitations exists for unfiled returns. The IRS can pursue unfiled returns indefinitely and assess taxes, penalties, and interest whenever they discover the missing returns. However, the IRS typically focuses on the most recent six years of returns for compliance purposes. For refund claims, taxpayers must file within three years of the original due date or lose the refund permanently.

Taking Action: What to Do Right Now

The worst response to a missed deadline? Continued avoidance.

Every day of delay adds penalties and interest. The balance grows. The IRS becomes less flexible. Collection efforts intensify.

Start by gathering all available tax documents. W-2s, 1099s, receipts for deductible expenses, records of estimated payments made. Request wage and income transcripts from the IRS if documents are missing using Form 4506-T or Get Transcript—these show what income the IRS has on file.

File the return as soon as possible using the standard filing process. If the tax bill seems insurmountable, file anyway and immediately contact the IRS to discuss payment options. Filing stops the failure-to-file penalty instantly.

For multiple years of unfiled returns, tackle them systematically. Start with the most recent year and work backward. Most taxpayers find that once they break through the initial psychological barrier, filing subsequent years becomes easier.

The tax system imposes harsh penalties for late filing, but it also provides multiple pathways to resolution. Extensions prevent penalties before they start. Payment plans make large balances manageable. Penalty relief mechanisms exist for qualifying circumstances.

The key? Action. File the return. Contact the IRS. Explore options. The penalties are real, but they’re far more manageable when addressed head-on rather than avoided.

Don’t let another day pass. The cost of delay compounds daily.