Quick Summary: When someone dies with debt, the debt is typically paid from the estate’s assets before distributing to heirs. If the estate lacks sufficient funds, most debts go unpaid and are forgiven—family members aren’t automatically responsible unless they co-signed, live in a community property state, or are legally obligated under specific circumstances.

Death doesn’t make debt disappear. But here’s what most people don’t realize—it also doesn’t automatically transfer to family members.

When someone passes away owing money, confusion often follows. Debt collectors start calling. Surviving relatives panic, wondering if they’re now on the hook for credit cards, medical bills, or loans they never signed for.

According to the Consumer Financial Protection Bureau, when someone dies with debt, that debt should be paid from any money or property left behind in the estate. If there’s nothing left? The debt generally goes unpaid.

Understanding this process matters. Especially when grief already makes everything harder.

How Debt Is Handled When Someone Dies

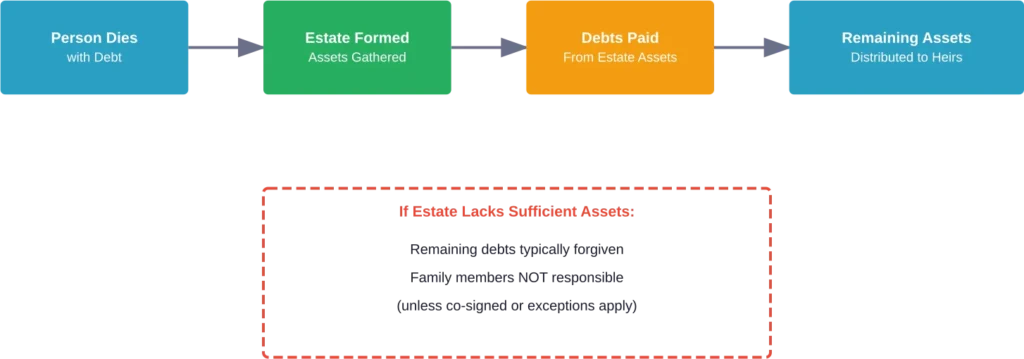

The estate—everything the deceased person owned—becomes responsible for settling debts. Not the children. Not the siblings. The estate itself.

Here’s how it works: When someone dies, their assets (bank accounts, property, investments, vehicles) form what’s legally called an estate. A personal representative or executor manages this estate, identifying all debts and assets.

Debts get paid in a specific order, determined by state law. Funeral expenses and estate administration costs typically come first. Then secured debts like mortgages. Credit cards and medical bills usually fall lower in the priority list.

Once all debts are settled from the estate’s assets, whatever remains goes to the heirs. But if the estate runs out of money before all debts are paid? The remaining debts typically vanish.

When Family Members Are Responsible for Debt

Most of the time, relatives don’t inherit debt. But exceptions exist.

The Consumer Financial Protection Bureau identifies several situations where someone else might be responsible for a deceased person’s debt:

Co-Signed Debts

If someone co-signed a loan or credit card, they’re equally responsible. Death doesn’t change that obligation. The lender can pursue the co-signer for the full amount, regardless of who actually made purchases or benefited from the loan.

Community Property States

Nine states follow community property laws: Arizona, California, Idaho, Louisiana, Nevada, New Mexico, Texas, Washington, and Wisconsin. In these states, surviving spouses may be responsible for debts incurred during the marriage, even if only one spouse’s name appears on the account.

Alaska allows couples to opt into community property agreements. This creates different rules than in common law states, where debt typically belongs only to the person who signed for it.

Joint Account Holders

Joint account holders—different from authorized users—share equal responsibility for the debt. If two people hold a credit card jointly, the survivor owes the full balance when one dies.

Authorized users, however, don’t owe anything. They had permission to use the card but never agreed to pay the debt.

State-Specific Obligations

Some states have filial responsibility laws or require spouses to pay certain medical debts. These laws vary significantly by location, creating a patchwork of obligations across the country.

| Situation | Family Responsible? | Notes |

|---|---|---|

| Co-signed loan or credit card | Yes | Co-signer remains fully liable |

| Joint account holder | Yes | Shares equal responsibility for debt |

| Community property state spouse | Maybe | Depends on when debt was incurred |

| Authorized user on credit card | No | Had permission but no payment obligation |

| Adult child of deceased | Generally no | Unless co-signed or state law requires |

| Surviving spouse in common law state | Generally no | Unless joint account or co-signed |

What Debts Are Forgiven at Death

Not all debts are created equal when someone passes away.

Unsecured debts—credit cards, medical bills, personal loans without collateral—are typically forgiven if the estate can’t pay them. Creditors can file claims against the estate, but once estate assets are exhausted, these debts vanish. They don’t transfer to family members.

Federal student loans get discharged when the borrower dies. Private student loans sometimes do, but policies vary by lender. Some private lenders discharge the debt, while others pursue the estate or any co-signers.

Credit card debt falls into the unsecured category. If the deceased person was the sole account holder and left no estate, credit card companies typically write off the balance. They can’t legally pursue family members who didn’t co-sign.

Secured Debts Work Differently

Mortgages and car loans don’t disappear. These secured debts are tied to specific property. The debt stays with the property.

If heirs want to keep the house, they’ll need to keep making mortgage payments. The Consumer Financial Protection Bureau issued an interpretive rule in 2024 clarifying that when a borrower dies, an heir’s name can generally be added to the mortgage without triggering ability-to-repay requirements.

If nobody wants the property or can’t afford payments, the lender can foreclose or repossess. But the heirs themselves don’t owe the difference if the property sells for less than the debt amount—unless they co-signed.

Dealing With Debt Collectors After a Death

Debt collectors can contact certain people about a deceased person’s debt, but strict rules govern these communications.

According to the Consumer Financial Protection Bureau, collectors can contact the spouse, personal representative, executor, or administrator handling the estate. They can also contact parents of a deceased minor child.

But here’s what they can’t do: They can’t mislead family members into thinking they’re responsible for debt they don’t actually owe. They can’t harass. They can’t discuss the debt with unauthorized parties.

If someone receives calls about a deceased relative’s debt and they’re not the spouse, executor, or co-signer, they have rights. They can send a written request telling the collector to stop contacting them. The collector must comply, with limited exceptions.

Protecting Yourself From Collector Tricks

Some debt collectors use misleading tactics to make grieving family members pay debts they don’t legally owe.

Common tricks include suggesting that not paying would be disrespectful to the deceased, implying that small payments are required “as a courtesy,” or deliberately confusing people about their legal obligations.

Making even a single small payment on someone else’s debt can sometimes be interpreted as accepting responsibility for it. Don’t pay anything without verifying the legal obligation first.

Estate Settlement and Probate Process

The probate process handles estate settlement legally. Not all estates go through probate—it depends on how assets were titled and the total estate value.

During probate, a court-appointed executor or administrator inventories all assets, notifies creditors, pays valid debts from estate funds, and distributes remaining assets to heirs according to the will or state intestacy laws.

Creditors typically have a limited window to file claims against the estate. This period varies by state but often ranges from three to six months after being notified of the death.

If creditors miss this deadline, they lose their right to collect from the estate. This protects heirs from claims appearing years later.

Assets That Bypass the Estate

Some assets never become part of the probate estate, which means they’re generally protected from creditors.

Life insurance proceeds paid to a named beneficiary don’t go through probate. They transfer directly to that beneficiary and typically can’t be claimed by the deceased person’s creditors.

Retirement accounts with designated beneficiaries work similarly. 401(k)s, IRAs, and pensions with named beneficiaries pass directly to those individuals, bypassing the estate and its debts.

Property held in joint tenancy with right of survivorship automatically transfers to the surviving owner. Bank accounts with payable-on-death designations go directly to the named person.

This is why estate planning matters. Properly structured, assets can pass to loved ones rather than being consumed by debt settlement.

How Estate Planning Reduces Debt Problems

Strategic planning before death can minimize debt complications for survivors.

Life insurance provides funds to pay debts without depleting assets intended for heirs. A policy with sufficient coverage ensures the mortgage gets paid, credit cards get settled, and heirs still receive their inheritance.

Trusts can protect certain assets from creditors, depending on the trust type and state laws. Irrevocable trusts, in particular, may shield assets since the deceased no longer technically owns them.

Beneficiary designations on financial accounts create automatic transfers that avoid probate and creditor claims. Reviewing and updating these designations regularly prevents assets from unintentionally falling into the probate estate.

Understanding estate tax implications matters too. According to the IRS, estate tax filing requirements depend on the gross estate value. The One, Big, Beautiful Bill was signed into law on July 4, 2025, as Public Law 119-21 and increases the basic exclusion amount to $15,000,000 for gifts for calendar year 2026, affecting how estates are taxed.

Special Cases: Medical Debt and Student Loans

Medical debt creates particular confusion because it’s often substantial and appears suddenly.

Like other unsecured debts, medical bills get paid from the estate if funds exist. If the estate lacks sufficient assets, medical debt generally goes unpaid. Hospitals and medical providers can’t pursue family members who didn’t sign treatment agreements or guarantees.

Some states have “filial responsibility” laws theoretically requiring adult children to pay parents’ medical costs, but these laws are rarely enforced and apply only in specific circumstances.

Student Loan Specifics

Federal student loans receive automatic discharge when the borrower dies. The loan servicer requires a death certificate, then cancels the remaining balance. Parent PLUS loans are also discharged if the parent borrower dies.

Private student loans vary by lender. Some discharge the debt upon death, others don’t. Co-signers on private student loans typically remain liable for the full amount unless the lender offers death discharge provisions.

This creates a critical distinction—federal loans disappear, private loans might not.

Protecting Yourself as a Survivor

When someone close passes away, certain steps protect survivors from improper debt collection.

First, notify creditors of the death promptly. Send copies of the death certificate. This stops interest and fees from accumulating and starts the clock on creditor claim periods.

Don’t make payments from personal funds before understanding the legal obligations. Well-meaning family members often pay bills they’re not required to pay, using their own money to settle someone else’s debt.

Request written validation of any debt a collector claims is owed. Collectors must provide documentation proving the debt exists and the amount is accurate.

If a collector violates rules or harasses you, file a complaint with the Consumer Financial Protection Bureau. They track complaints and can take action against problematic collectors.

Consider consulting an estate attorney, especially if the estate is complex or creditors are aggressive. The cost of legal advice often saves more money than it costs.

Frequently Asked Questions

No. According to the Consumer Financial Protection Bureau, debt doesn’t automatically transfer to family members when someone dies. Debt gets paid from the deceased person’s estate. If the estate lacks sufficient assets, most debts go unpaid and are forgiven. Family members are only responsible if they co-signed, are joint account holders, or live in community property states with certain debt types.

If someone dies with no assets or estate, credit card debt typically goes unpaid and is eventually written off by the creditor. Credit card companies cannot pursue family members, children, or friends for payment unless those individuals co-signed the account or were joint holders. Authorized users are not responsible for the debt.

Generally, no. Adult children are not responsible for their parents’ debt unless they co-signed loans or credit accounts. Some states have filial responsibility laws that theoretically could require adult children to pay parents’ medical or long-term care costs, but these laws are rarely enforced. Children should not pay their parents’ debts from personal funds without legal obligation to do so.

Estate debts get paid in priority order determined by state law before heirs receive anything. Typically, funeral expenses and estate administration costs come first, followed by secured debts like mortgages and car loans, then taxes, and finally unsecured debts like credit cards and medical bills. If estate assets are exhausted before all debts are paid, remaining low-priority debts go unpaid.

Life insurance proceeds paid directly to a named beneficiary generally cannot be claimed by the deceased person’s creditors. These funds bypass the probate estate and transfer directly to the beneficiary. However, if the estate itself is named as beneficiary, those proceeds become part of the estate and can be used to pay debts before distribution to heirs.

The time limit varies by state but typically ranges from three to six months after creditors are notified of the death. Executors must notify known creditors and often publish notice in newspapers. Creditors who fail to file claims within the statutory period generally lose their right to collect from the estate, protecting heirs from old debts appearing later.

In common law states, surviving spouses typically aren’t responsible for debts solely in the deceased spouse’s name unless they co-signed or benefited from the debt under state law. In community property states, surviving spouses may be responsible for debts incurred during the marriage even if only one spouse’s name was on the account. State law determines specific obligations.

The Bottom Line on Debt and Death

Death doesn’t erase debt, but it also doesn’t automatically make that debt someone else’s problem.

Estates settle debts before heirs receive assets. When estates can’t cover everything, most debts get written off. Family members rarely inherit debt unless they specifically signed for it or fall under state-specific exceptions.

Understanding these rules protects grieving families from paying obligations they don’t legally owe. It also highlights why estate planning matters—proper planning ensures assets reach loved ones rather than creditors.

If debt collectors contact you about a deceased relative’s debt and you’re unsure of your obligations, don’t guess. Consult an estate attorney or contact the Consumer Financial Protection Bureau for guidance. Knowledge protects you from paying debts that aren’t yours and helps navigate an already difficult time with greater confidence.