Quick Summary: Closing a credit card can impact your credit score by increasing your credit utilization ratio and potentially reducing your average account age. According to the Consumer Financial Protection Bureau, you remain obligated to pay any remaining balance plus interest even after closing an account. The impact varies based on your overall credit profile—it may be minor if you have multiple older accounts, or more significant if it’s your oldest card or you carry high balances.

Closing a credit card seems simple enough. Call the issuer, confirm the closure, and move on with your life.

But the aftermath isn’t quite that straightforward. That single action ripples through multiple factors that determine your credit score, and not always in ways people expect.

Here’s what actually happens when you close a credit card account—and how to make the decision that works for your financial situation.

How Closing a Credit Card Affects Your Credit Score

Credit card closures impact your score through two primary mechanisms that interact with how credit scoring models evaluate your financial behavior.

Credit Utilization Ratio Takes the Biggest Hit

Your credit utilization ratio represents the percentage of available credit you’re currently using. It’s one of the most influential factors in credit scoring models.

When you close a card, you eliminate that credit line from your total available credit. Any outstanding balances on other cards suddenly represent a higher percentage of your now-smaller credit pool.

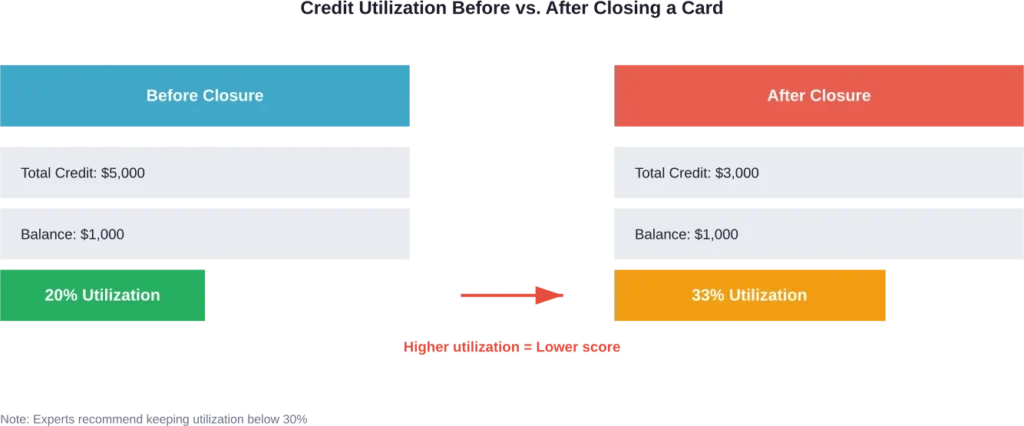

Let’s say you have two cards: one with a $3,000 limit and another with a $2,000 limit. Your total available credit is $5,000. If you’re carrying a $1,000 balance, your utilization is 20%.

Close the card with the $2,000 limit? Your available credit drops to $3,000, and that same $1,000 balance now represents 33% utilization—well above the 30% threshold where scores typically start declining more noticeably.

Average Age of Accounts May Decrease

Credit scoring models consider how long your accounts have been open. Older accounts generally benefit your score because they demonstrate a longer track record of managing credit.

The effect here is more nuanced than many people realize. Closed accounts can remain on your credit report for seven to 10 years, depending on whether the account was in good standing when it was closed.

But once that closed account eventually falls off your report, your average age of accounts can drop—sometimes significantly if it was your oldest card.

Credit Mix Might Be Affected

Credit scoring models favor diverse credit profiles. Having both revolving credit (credit cards) and installment loans (mortgages, auto loans) typically works in your favor.

If you close your only credit card or reduce your card count substantially, you might see a small score impact from reduced credit mix diversity.

What Happens to Your Balance When You Close a Card

This catches people off guard more than anything else.

According to the Consumer Financial Protection Bureau, closing a credit card doesn’t erase your obligation to repay any outstanding balance. You remain required to pay at least the minimum amount until the full balance is paid off.

The card issuer can—and will—continue charging interest on what you owe. Your cardholder agreement remains in effect for the balance repayment terms.

One thing changes though: you can’t make new purchases on the closed account. The card is shut down for future transactions while you pay down the existing debt.

When Closing a Credit Card Actually Makes Sense

Sometimes closing a card is the right financial move, credit score impact notwithstanding.

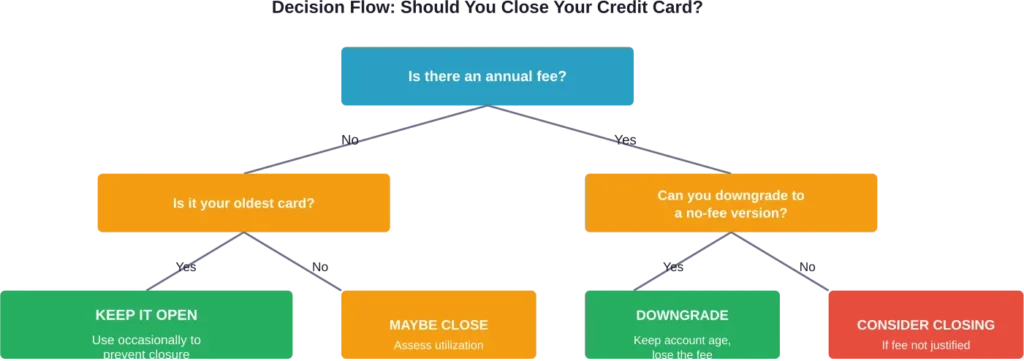

Annual Fees Aren’t Justified

Paying $95, $250, or even $500+ annually for a card you don’t use enough to offset the fee through rewards or benefits doesn’t make financial sense.

If you can’t downgrade to a no-fee version of the card, closing it might be the smart choice.

Temptation to Overspend Is Too Strong

Real talk: if having available credit leads to spending problems, protecting your financial health matters more than optimizing your credit score.

Closing cards to remove temptation is a legitimate debt management strategy.

The Card Has Predatory Terms

High interest rates combined with unfavorable terms sometimes warrant closing an account, especially if better options exist and the problematic card isn’t your oldest account.

Divorce or Financial Separation

Joint accounts or authorized user situations sometimes require clean breaks. Closing shared credit cards prevents future complications.

| Situation | Consider Closing? | Key Factor |

|---|---|---|

| High annual fee, low usage | Yes | Check for no-fee downgrade option first |

| Spending control issues | Yes | Financial health trumps credit score |

| Zero balance, no fees | Usually no | Keeping it helps utilization ratio |

| Oldest credit card | No | Preserve account age even if unused |

| Duplicate rewards cards | Maybe | Consolidate if not your oldest account |

When You Should Keep a Credit Card Open

Most of the time, keeping unused cards open benefits your credit profile more than closing them.

It’s Your Oldest Account

That first credit card you opened in college? Keep it. Even if the rewards are mediocre and you never use it, that account age is valuable for your credit history.

Put a small recurring charge on it every few months—a streaming subscription, for example—and set up autopay. This keeps the account active without requiring active management.

You Have High Balances on Other Cards

If your credit utilization is already elevated, closing additional cards makes the problem worse. Keep those unused credit lines open to maintain a healthier utilization ratio.

The Card Has No Annual Fee

Zero-fee cards cost nothing to keep open. There’s no financial downside to letting them sit in a drawer while they continue benefiting your credit profile.

You’re Planning a Major Credit Application Soon

Applying for a mortgage or auto loan in the next 6-12 months? Now isn’t the time to close credit cards. Keep your credit profile stable until after the application is approved.

Smart Alternatives to Closing a Credit Card

Before you close that account, consider these options.

Product Change to a No-Fee Card

Many issuers let you convert a card to a different product within their lineup. That premium rewards card with the $250 annual fee? Often it can be downgraded to a basic no-fee version.

You keep the account age and credit line. You lose the annual fee. Win-win.

Reduce the Credit Limit

If temptation to overspend is the concern but you want to preserve the account, request a credit limit reduction. This maintains the account while limiting potential damage.

Lock or Freeze the Card

Most card issuers now offer digital locking features through their mobile apps. Lock the card to prevent new purchases while keeping the account technically open.

Set Up a Small Recurring Charge

Worried the issuer will close the card due to inactivity? Put a small monthly subscription on it and enable autopay. The account stays active with zero effort.

How to Close a Credit Card Responsibly

If you’ve decided closing the card is the right move, follow these steps to minimize complications.

First, pay off the balance completely if possible. While you can close a card with a balance, eliminating the debt first simplifies the process and prevents confusion about payment obligations.

Redeem any remaining rewards. Points, cash back, or miles typically disappear when you close the account. Transfer or redeem them before initiating closure.

Contact the card issuer directly. Call the customer service number on the back of your card and request account closure. Some issuers also allow closure through online account portals.

According to the Consumer Financial Protection Bureau, follow up with written notice. Send a letter confirming your closure request and keep a copy for your records.

Wait 30-45 days, then check your credit report to verify the account shows as “closed by cardholder” rather than “closed by creditor.” The distinction matters—the former indicates you initiated the closure, while the latter can signal problems to future lenders.

What About Closing a Credit Card With Zero Balance

A zero balance doesn’t change the credit score impact mechanisms. Your credit utilization ratio still increases when you eliminate that credit line. Your average account age timeline still starts.

The administrative process is simpler though. No balance means no ongoing payment obligations, no interest charges, and no confusion about debt repayment.

But here’s the thing: if the card has no annual fee and carries a zero balance, the strongest argument for closing it evaporates. Keeping it costs nothing and helps your credit profile.

Monitoring the Impact After Closure

Credit scores typically adjust within one to two billing cycles after a card closure as updated information reports to the credit bureaus.

The magnitude of impact varies dramatically based on individual circumstances. Someone with ten credit cards, low balances, and a long credit history might see a minimal score change—perhaps 5-10 points.

The impact could vary significantly based on individual credit profiles and circumstances.

Check your credit report a month after closure to understand the actual effect on your specific credit profile.

Frequently Asked Questions

It can, primarily by increasing your credit utilization ratio. The impact varies based on your overall credit profile, how many cards you have, and whether the closed card is your oldest account. Someone with multiple cards and low balances might see minimal impact, while closing your only card or oldest account typically causes more significant score decreases.

Yes. According to the Consumer Financial Protection Bureau, you remain obligated to pay any balance on schedule after closing an account, and the card issuer can continue charging interest on what you owe. Closing the account only prevents new purchases—it doesn’t eliminate existing debt or stop interest accrual.

Generally no, especially if they have no annual fee. Unused cards with zero fees help your credit utilization ratio and preserve account age. Consider putting a small recurring charge on them with autopay instead to keep them active. Only close unused cards if they carry annual fees you can’t justify or if you’ve unsuccessfully tried to downgrade to a no-fee version.

Closed accounts can remain on your credit report for seven to 10 years, depending on whether the account was in good standing when it was closed. Once the account falls off your report, your average age of accounts may decrease if it was an older card.

Pay off the balance completely if possible, redeem any remaining rewards, then contact the issuer to request closure. Follow up with written notice confirming your request. Wait 30-45 days and check your credit report to verify the account shows as “closed by cardholder” rather than “closed by creditor,” which signals you initiated the closure.

The credit score impact mechanisms remain the same regardless of balance—your utilization ratio increases and account age timeline begins. The process is administratively simpler with no balance since there are no payment obligations, but the effect on your score follows the same patterns based on your overall credit profile.

Possibly, but it’s not guaranteed. Some issuers allow reopening recently closed accounts within 30-90 days, though policies vary. After that window, reopening typically requires a new application, which generates a hard inquiry and creates a new account rather than restoring the old one—meaning you lose the original account’s age benefit.

Making the Right Decision for Your Situation

Closing a credit card isn’t inherently good or bad. The right choice depends entirely on your financial circumstances, credit profile, and goals.

High annual fees with insufficient value? Close it or downgrade. Oldest account with no fees? Keep it open. Struggling with spending control? Your financial health matters more than your credit score.

The credit score impact is real but typically temporary and manageable, especially for people with established credit histories and multiple accounts. What matters most is making an informed decision based on accurate information rather than assumptions about how credit scoring works.

Before closing any credit card, evaluate your complete credit picture. Check your current utilization ratio, identify your oldest accounts, and consider whether alternatives like product changes or credit limit reductions might better serve your needs.

Your credit report is available free from all three bureaus annually. Review it before making account closure decisions so you understand exactly how the change will affect your overall credit profile.