Quick Summary: Suing someone with no money is legally possible and you can win a judgment, but collecting on that judgment may prove difficult or impossible if the defendant is judgment-proof (lacks assets, income, or insurance to pay). Courts evaluate cases on merit, not ability to pay, so financial status doesn’t prevent lawsuits. However, enforcement tools like wage garnishment, bank levies, and asset seizures only work if the defendant has non-exempt property or income.

Someone rear-ended your car. A contractor abandoned your home renovation halfway through. A former business partner violated your agreement.

The legal case is solid. But here’s the problem: the person who wronged you appears to have no money.

Does that mean you’re out of luck? Can you even file a lawsuit against someone who’s broke? And if you win, what happens next?

The short answer? Yes, you can absolutely sue someone with no money. Courts don’t require defendants to pass a financial screening before you can file. But collecting on a judgment against someone who’s genuinely broke presents serious challenges.

Can You Actually Sue Someone With No Money?

The law doesn’t prevent lawsuits based on a defendant’s financial situation. Courts evaluate cases on their legal merit, not on whether the losing party can afford to pay.

This means you can file a lawsuit, proceed through the legal process, present your evidence, and potentially win a judgment—regardless of the defendant’s bank account balance.

The court’s job is determining liability and damages. If the defendant caused you harm through negligence, breach of contract, or intentional wrongdoing, the court can rule in your favor and order them to pay compensation.

But winning a judgment and actually collecting that money are two entirely different things.

Think of it this way: a judgment is essentially a legal IOU. The court has determined the defendant owes you money. But if that person has no assets, no income, and no insurance coverage, that IOU might never convert into actual dollars.

Understanding What “Judgment-Proof” Really Means

The legal term for someone who can’t pay a judgment is “judgment-proof.”

According to Cornell Law School’s Legal Information Institute, judgment-proof describes “persons against whom enforcing a judgment is not feasible, or not worth the costs of pursuing litigation.” These are people who lack the resources or insurance to pay a court judgment against them.

Sound like a get-out-of-jail-free card? It’s not quite that simple.

Being judgment-proof isn’t a legal status someone can claim to avoid lawsuits. It’s a practical reality that affects collection, not liability. The defendant is still legally responsible. They still lost the case. The judgment still exists on their record.

They just don’t have anything you can take to satisfy the debt.

Common Characteristics of Judgment-Proof Defendants

People typically considered judgment-proof share several characteristics:

- Unemployed or earning very low wages below garnishment thresholds

- No significant bank accounts or cash reserves

- No real estate ownership, or property fully protected by homestead exemptions

- No valuable personal property beyond basic exemptions

- Relying entirely on protected income like Social Security or disability benefits

- Already in bankruptcy or deeply insolvent

Here’s what many people don’t realize: judgment-proof status isn’t necessarily permanent. Someone who’s broke today might find employment next year. They might inherit money, win a settlement in another case, or start a business.

Judgments typically last 10-20 years depending on the state, and can often be renewed. That gives you a long window to collect if their circumstances improve.

How Courts Handle Judgment Collection

After winning your case, the court doesn’t automatically hand you a check. The court’s role essentially ends with the judgment itself.

Collection becomes your responsibility.

You’ll need to use various legal enforcement mechanisms to locate assets and compel payment. These tools can be powerful when the defendant has money. Against someone judgment-proof, they’re essentially useless.

Wage Garnishment: The Most Common Collection Tool

If the defendant has a job, wage garnishment is often the most reliable collection method.

According to Nolo, federal law limits garnishment to 25% of disposable earnings or the amount by which wages exceed 30 times the federal minimum wage, whichever is less. Some states impose even stricter limits.

But wage garnishment only works if the person is employed and earning above minimum thresholds. Someone working part-time at minimum wage might have legally protected income that can’t be garnished at all.

For California specifically, one source indicates garnishment may be capped at the lesser of 20% of disposable income or 40% of everything earned beyond 48 times the applicable minimum wage under California Code of Civil Procedure § 706.050.

Bank Levies and Asset Seizures

With a writ of execution, you can direct a sheriff or marshal to seize funds from the defendant’s bank account or take possession of physical assets like vehicles or business equipment.

But this only works if there’s actually money in the account or valuable property to seize.

Many types of funds are exempt from levy, including Social Security benefits, disability payments, unemployment insurance, and veterans benefits. If the defendant’s bank account only contains protected funds, the levy produces nothing.

Property Liens and Real Estate

Placing a lien on real property can be effective—if the defendant owns real estate with sufficient equity.

According to the Ninth Circuit Court of Appeals glossary, equity is “the value of a debtor’s interest in property that remains after liens and other creditors’ interests are considered.” For example, a house valued at $60,000 subject to a $30,000 mortgage has $30,000 of equity.

But here’s the catch: most states have homestead exemptions that protect a certain amount of home equity from creditors.

Nolo provides this example: Jeff lives in a state with a $50,000 homestead exemption. His home has a fair market value of $250,000 with a $175,000 mortgage. That leaves $75,000 in equity, but $50,000 is exempt, leaving only $25,000 potentially available to creditors.

In some states, homestead exemptions are even more generous—or the defendant simply doesn’t own property at all.

What Income and Assets Are Protected From Collection?

Federal and state laws protect certain income sources and property types from judgment creditors. These exemptions exist to ensure people can maintain basic living standards even when they owe money.

| Income/Asset Type | Protection Status | Notes |

|---|---|---|

| Social Security benefits | Fully protected | Cannot be garnished for most judgments |

| Disability benefits | Fully protected | Both SSI and SSDI are exempt |

| Unemployment compensation | Fully protected | Protected under federal law |

| Veterans benefits | Fully protected | Exempt from creditor claims |

| Workers compensation | Fully protected | Cannot be levied or garnished |

| Wages (employed) | Partially protected | Max 25% federal, 20% some states |

| Primary residence | Partially protected | Homestead exemption varies by state |

| Personal vehicle | Partially protected | Often exempt up to certain value |

| Household goods | Mostly protected | Basic furniture, appliances exempt |

| Retirement accounts | Often protected | 401(k), IRA usually exempt |

These exemptions explain why someone can be legally liable for a debt but practically unreachable for collection purposes.

Someone whose only income is Social Security and who rents an apartment rather than owning property has virtually nothing a creditor can touch—even with a valid court judgment.

The Role of Insurance in Collection

Here’s where things get more promising: many defendants might be personally broke, but they could have insurance coverage that applies to your claim.

Auto accidents, slip-and-fall injuries, professional malpractice, and business disputes often involve insurance policies that cover the defendant’s liability.

If insurance applies, you’re not trying to collect from the individual’s personal assets. Instead, the insurance company pays up to the policy limits.

This changes the entire calculation. A defendant with no personal money but a $100,000 auto liability policy is actually a very collectible defendant—up to that $100,000 limit.

But what if the damages exceed policy limits? Or the insurance company denies the claim?

Then you’re back to pursuing the individual’s personal assets. And if those don’t exist, you’re facing the judgment-proof problem again.

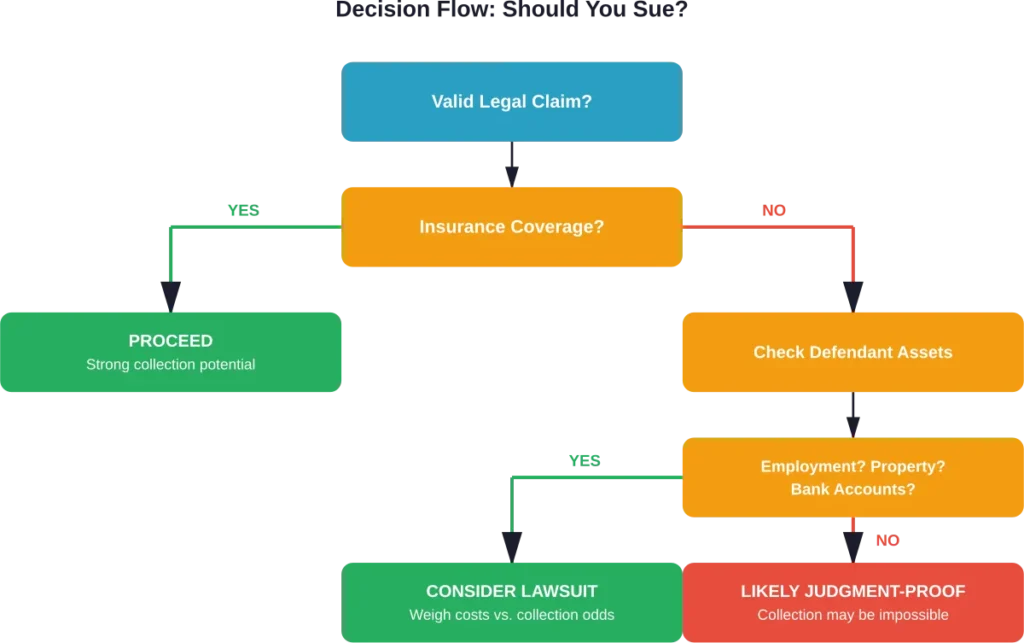

Is It Worth Suing Someone With No Money?

This is the critical question. Just because you can sue doesn’t mean you should.

Filing a lawsuit costs money and time. Court filing fees, service of process, evidence gathering, and potentially attorney fees all add up. If the defendant is judgment-proof, you might spend thousands to win a judgment you can never collect.

That said, there are legitimate reasons to sue even when collection seems unlikely.

Strategic Reasons to Proceed With a Lawsuit

Some situations justify filing despite collectability concerns:

- Insurance coverage exists: Even if the defendant is personally broke, their insurance might pay the full judgment.

- Future earnings potential: A young professional with current debts but strong future earning capacity might be worth pursuing.

- Business assets: Someone operating a business might have business accounts, inventory, or equipment that can be seized even if personal assets are protected.

- Multiple defendants: If you’re suing several parties, one judgment-proof defendant doesn’t doom the entire case.

- Long-term leverage: Judgments can be renewed for decades. Their financial situation might change dramatically over time.

- Preventing statute of limitations: Filing suit preserves your claim even if you wait to pursue collection.

According to community discussions on legal forums, some plaintiffs file lawsuits primarily to establish the legal record, even knowing immediate collection is impossible. The judgment remains enforceable for years, waiting for the defendant’s circumstances to improve.

When You Should Probably Skip the Lawsuit

Other situations suggest walking away might be wiser:

- The defendant’s only income is Social Security or disability benefits

- They’ve recently filed bankruptcy or are deeply insolvent

- They’re elderly with no assets and no likelihood of future income

- The claim amount is small compared to litigation costs

- No insurance coverage applies

- They’ve successfully avoided collection on multiple other judgments

Nolo’s guidance emphasizes investigating collectability before filing suit. Smart plaintiffs research the defendant’s employment, property ownership, business interests, and insurance coverage before spending money on legal fees.

How Long Do Judgments Last?

Here’s some good news: judgments don’t expire quickly.

Most states allow judgments to remain enforceable for 10 to 20 years, and many states permit renewal that extends the enforcement period for another full term.

This creates a long-term collection opportunity. Someone who’s genuinely broke today might graduate from school, get promoted, start a business, receive an inheritance, or otherwise come into money over the next decade or two.

Your judgment sits waiting, accruing interest often at a legal rate of approximately 8% unless the contract specifies a different rate, ready to be enforced whenever collectible assets appear.

Some creditors play the long game intentionally. They obtain judgments knowing collection is currently impossible, then monitor the debtor’s circumstances for years, ready to act when financial improvement occurs.

Alternatives to Traditional Lawsuits

Before committing to a full lawsuit, consider whether alternatives might serve your interests better.

Small Claims Court

For smaller amounts (typically under $5,000-$10,000 depending on the state), small claims court offers a faster, cheaper process with minimal filing fees and no attorney requirement.

Even if you can’t collect immediately, the lower cost of obtaining a small claims judgment makes the long-term collection strategy more economical.

Demand Letters and Settlement Negotiations

Sometimes the threat of a lawsuit motivates payment even when the defendant seems to have no money. They might borrow from family, liquidate small assets you didn’t know about, or agree to a payment plan.

A strongly worded demand letter costs far less than litigation and occasionally produces results.

Reporting to Credit Bureaus

While you can’t report debts directly to credit bureaus, judgments often appear on credit reports through public record monitoring services. This can create pressure for the defendant to settle, especially if they’re trying to rent an apartment, buy a car, or apply for employment.

When Defendants Hide Assets

Some people who claim to be judgment-proof are actually hiding assets through various tactics:

- Transferring property to family members or trusts

- Operating businesses under different names or entities

- Maintaining bank accounts in other people’s names

- Claiming false exemptions

- Working for cash to avoid wage garnishment

If you suspect fraudulent transfers or hidden assets, judgment debtor examinations allow you to question the defendant under oath about their finances. Lying in these proceedings constitutes perjury.

Forensic asset searches conducted by professional investigators can sometimes uncover hidden property, though these services cost money and aren’t guaranteed to find anything.

The Emotional Factor: Principle vs. Practicality

Community discussions reveal that many people want to sue “on principle” even when collection seems unlikely.

The desire for a court to formally declare you were right and they were wrong is understandable. A judgment vindicates your claim and creates a public record of the defendant’s liability.

But principle doesn’t pay legal bills.

Before proceeding on principle alone, calculate the true cost. If you’ll spend $5,000 in fees and lost time to obtain a $3,000 judgment you can’t collect, that’s a $5,000 investment in validation. Can you afford that? Is it worth it to you?

Only you can answer that question. Just make sure you’re answering it honestly, with clear knowledge of the likely financial outcome.

Steps to Take Before Filing Your Lawsuit

If you’re seriously considering suing someone who might not have money to pay, take these investigative steps first:

- Search property records: County assessor websites show real estate ownership and assessed values. Check whether the defendant owns property with equity.

- Verify employment: Employed defendants with steady income are far more collectible than unemployed ones, even if they currently have no savings.

- Check business registrations: Search state business entity databases to see if the defendant owns or operates any businesses.

- Review insurance possibilities: Determine what types of insurance might cover your claim (auto, homeowners, professional liability, general business).

- Search court records: Look for other judgments against this defendant. Multiple unsatisfied judgments suggest they’re successfully avoiding collection.

- Consider debt-to-asset ratios: Someone with $200,000 in equity but $500,000 in existing liens and judgments might have nothing left for you even though they appear wealthy on paper.

- Assess age and earning potential: A 25-year-old recent graduate has decades of earning potential ahead. A 75-year-old retiree living on Social Security probably doesn’t.

Professional skip tracing services and asset search companies can conduct more thorough investigations, though they charge fees. For larger potential judgments, this research investment makes sense.

What Happens After You Win the Judgment

Let’s say you proceed with the lawsuit and win. What actually happens next?

The court enters a judgment in your favor specifying the amount owed. This creates a legal debt, but remember—the court doesn’t collect it for you.

You become a judgment creditor. The defendant becomes a judgment debtor. And you must now use the various enforcement mechanisms to attempt collection.

This process typically involves:

- Obtaining certified copies of the judgment

- Serving interrogatories (written questions) about the debtor’s finances

- Conducting a judgment debtor examination (in-person questioning under oath)

- Applying for writs of execution to levy bank accounts or seize property

- Requesting earnings withholding orders for wage garnishment

- Recording abstracts of judgment to create liens on real property

Each of these steps involves filing fees, service costs, and time. Against a cooperative debtor with assets, the process works smoothly. Against someone judgment-proof, you’re throwing good money after bad.

Bankruptcy: The Nuclear Option for Defendants

Here’s another reality check: if you successfully begin collecting on a judgment, the debtor can file for bankruptcy protection.

According to United States Courts information on Chapter 11 bankruptcy, bankruptcy filings require a $1,167 case filing fee and a $571 miscellaneous administrative fee (fees subject to change), and can discharge many types of debts, including judgments from lawsuits.

Chapter 7 bankruptcy can eliminate the judgment entirely if it qualifies as dischargeable debt. Chapter 11 or Chapter 13 might restructure it into a payment plan at pennies on the dollar.

Certain debts survive bankruptcy—judgments from fraud, willful injury, or drunk driving, for example. But ordinary negligence or breach of contract judgments usually get wiped out.

This creates another layer of collection risk. Even if the defendant isn’t currently judgment-proof, they might choose bankruptcy to avoid paying your judgment.

State-Specific Collection Rules

Collection laws vary significantly by state. Homestead exemptions range from a few thousand dollars to unlimited in states like Florida and Texas. Wage garnishment limits differ. Personal property exemptions vary.

Before proceeding with collection efforts, research your specific state’s exemption laws. What’s collectible in one state might be completely protected in another.

Some states also require judgment creditors to exhaust certain collection remedies before pursuing others, or impose waiting periods between collection attempts.

State-specific rules matter. Don’t assume collection procedures that worked in one state will work the same way elsewhere.

Frequently Asked Questions

Yes, absolutely. Courts determine liability based on the facts and law, not on the defendant’s ability to pay. If the defendant is legally responsible for your damages, you can win a judgment regardless of their financial status. However, winning the case and collecting the money are separate issues. A judgment-proof defendant might lose the case but remain unable to pay.

Judgments typically remain enforceable for 10 to 20 years depending on the state, and can often be renewed for additional periods of equal length. This means you might have decades to collect if the defendant’s financial situation eventually improves. The judgment also usually accrues interest during this time, increasing the total amount owed.

Federal and state laws protect certain income sources from garnishment, including Social Security benefits, disability payments (both SSI and SSDI), unemployment compensation, veterans benefits, and workers compensation. Many states also protect some portion of wages, typically limiting garnishment to 25% of disposable earnings under federal law, or 20% in states like California.

Generally speaking, suing someone whose only income is Social Security or similar protected benefits is not financially worthwhile unless insurance coverage applies to your claim. Social Security income cannot be garnished for most judgments, and people in this situation typically have few other assets to pursue. The cost of litigation would likely exceed any realistic collection potential.

In most cases, yes. Bankruptcy can discharge many types of judgment debts, including those from negligence or breach of contract. However, certain judgments survive bankruptcy, including those arising from fraud, willful and malicious injury, drunk driving accidents, and some other specific circumstances. If you’re concerned about this possibility, consult with an attorney about whether your particular claim would be dischargeable in bankruptcy.

You can research property ownership through county assessor websites, search business entity registrations through state databases, and review court records for other judgments. Professional asset search services can conduct more thorough investigations for a fee. Many attorneys recommend conducting this research before filing suit to avoid wasting money pursuing judgment-proof defendants.

Fraudulent transfers made to avoid creditors can be challenged in court. If you can prove that property was transferred specifically to avoid paying your judgment, courts may reverse the transfer or allow you to pursue the property in the hands of the new owner. However, proving fraudulent intent requires evidence and legal action, adding more time and expense to the collection process.

Making Your Decision

So what happens if you sue someone with no money? You can win your case, obtain a legal judgment, and still walk away with nothing.

But that’s not always the end of the story.

Insurance might cover the claim. The defendant might have hidden assets. Their financial situation might improve over the years. The judgment might create enough pressure to force a settlement.

Or you might spend thousands of dollars and years of effort chasing money that will never materialize.

The key is making this decision with eyes wide open. Investigate first. Understand the collection realities in your state. Calculate the costs honestly. Consider alternatives like small claims court or settlement negotiation.

And if you do proceed, do so with realistic expectations about what that judgment might actually be worth.

Legal vindication has value. A court declaring you were right and they were wrong matters. But it doesn’t pay your bills, repair your property, or compensate you for your injuries.

Only collectible assets do that.

Before you file that lawsuit, make sure you understand the difference between a judgment on paper and money in your bank account. They’re not the same thing—and against a truly judgment-proof defendant, they might never become the same thing no matter how long you wait.

If you’re facing this decision, consider consulting with an attorney who can evaluate your specific situation, research the defendant’s collectability, and provide realistic guidance on whether litigation makes financial sense. That consultation fee might be the best money you spend—especially if it saves you from pursuing an uncollectible judgment.