Quick Summary: Filing bankruptcy doesn’t automatically mean losing your house. What happens depends on the bankruptcy chapter you file, how much home equity you have, whether you’re current on mortgage payments, and your state’s homestead exemption. Chapter 7 may require selling assets if equity exceeds exemptions, while Chapter 13 lets you keep the home and catch up on missed payments through a repayment plan.

The fear of losing a home stops thousands of people from filing bankruptcy every year. It’s a legitimate concern. But here’s the reality: bankruptcy doesn’t automatically strip away homeownership rights.

What actually happens to your house depends on several interconnected factors. The bankruptcy chapter matters. So does the amount of equity sitting in the property. Mortgage payment status plays a role. And state exemption laws determine how much protection homeowners receive.

Understanding these variables makes the difference between unnecessary panic and informed decision-making.

How Bankruptcy Treats Your Home: The Fundamentals

Bankruptcy law recognizes that people need shelter. That’s why federal and state laws include homestead exemptions — legal protections that shield a certain amount of home equity from creditors.

When someone files bankruptcy, all their assets technically become part of the bankruptcy estate. A trustee reviews these assets to determine what can be sold to pay creditors. But exemptions exist specifically to prevent debtors from becoming destitute.

The homestead exemption protects equity in a primary residence. If total home equity falls below the exemption threshold, the trustee typically can’t force a sale. The homeowner keeps the property.

What Counts as Home Equity

Home equity represents the difference between current market value and outstanding mortgage debt. Say a house appraises at $300,000 with a $240,000 mortgage balance. The equity equals $60,000.

That $60,000 is what matters for bankruptcy purposes. Not the home’s total value.

Multiple liens reduce equity further. A second mortgage or home equity line of credit decreases the amount available to creditors or protected by exemptions.

Chapter 7 Bankruptcy and Your House

Chapter 7 is often called liquidation bankruptcy. According to the United States Courts, this chapter provides for the sale of a debtor’s nonexempt property and distribution of proceeds to creditors.

Sounds scary for homeowners. But most people who file Chapter 7 keep their homes.

Here’s why: If home equity doesn’t exceed the homestead exemption amount, there’s nothing for the trustee to recover. Forcing a sale wouldn’t generate funds for creditors after paying off the mortgage and exemption amount.

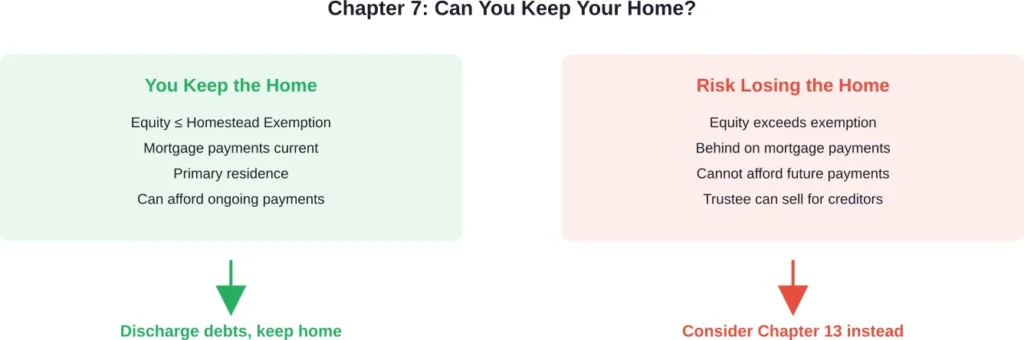

When You Can Keep Your Home in Chapter 7

Homeowners typically retain their property in Chapter 7 when:

- Home equity falls below the state homestead exemption limit

- Mortgage payments are current and can remain current going forward

- The property serves as the debtor’s primary residence

The trustee performs a straightforward calculation. Take the home’s fair market value, subtract all liens and mortgages, then subtract the applicable homestead exemption. If nothing remains, the home provides no value to the bankruptcy estate.

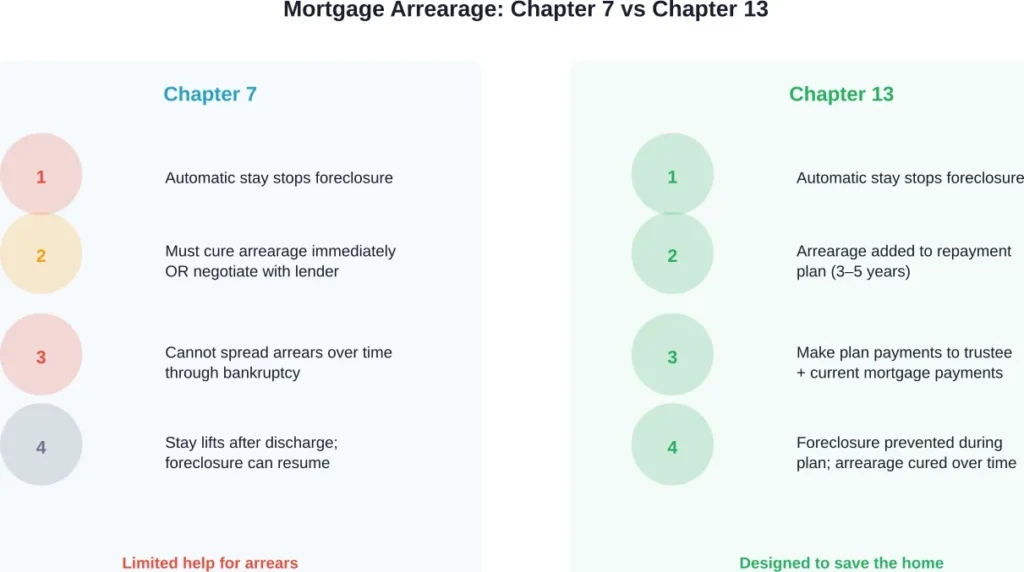

But there’s a critical requirement: mortgage payments must continue. Bankruptcy discharges personal liability for the mortgage debt, but the lender’s lien on the property survives. Stop making payments, and foreclosure remains a possibility even after bankruptcy discharge.

When Chapter 7 Might Cost You the House

Problems arise when equity significantly exceeds exemption limits. In that scenario, the trustee can sell the home, pay off the mortgage, give the homeowner their exemption amount, and distribute the remainder to creditors.

This creates a real risk in states with low homestead exemptions or for homeowners with substantial equity from years of payments or property appreciation.

Some debtors in this situation choose Chapter 13 instead, specifically to avoid losing the home.

Chapter 13 Bankruptcy: The Home-Saver Option

Chapter 13 operates completely differently. According to the United States Courts, Chapter 13 is also called a wage earner’s plan because it enables individuals with regular income to develop a plan to repay all or part of their debts.

The repayment period runs three to five years. Debtors with current monthly income below the state median typically get three-year plans unless the court approves longer “for cause.” Those with income above the median generally must propose five-year plans.

This structure makes Chapter 13 particularly valuable for homeowners behind on mortgage payments.

How Chapter 13 Protects Your Home

Chapter 13 allows debtors to catch up on mortgage arrears through the repayment plan. Someone who’s $15,000 behind on their mortgage can propose spreading that arrearage over 36 or 60 months while maintaining current mortgage payments.

The automatic stay that comes with filing stops foreclosure proceedings immediately. As long as the debtor complies with the repayment plan, the lender cannot foreclose.

According to the United States Courts, Chapter 13 acts like a consolidation loan under which the individual makes plan payments to a Chapter 13 trustee who then distributes payments to creditors. Individuals have no direct contact with creditors while under Chapter 13 protection.

This structure provides breathing room to get finances back on track.

Chapter 13 Requirements for Keeping Your Home

Keeping a home through Chapter 13 requires meeting ongoing obligations. Debtors must:

- Make all plan payments to the trustee on time

- Keep current mortgage payments current going forward

- Maintain property insurance

- Pay property taxes when due

Miss these obligations, and the case can be dismissed. Once dismissed, foreclosure protection disappears.

The advantage? Chapter 13 doesn’t care about equity levels the way Chapter 7 does. High equity doesn’t trigger forced sales. The debtor keeps the property regardless of how much it’s worth, as long as plan payments continue.

Homestead Exemptions: State-by-State Variations

Bankruptcy law allows debtors to choose between federal exemptions and their state’s exemption system. Some states require use of state exemptions.

Homestead exemption amounts vary dramatically. Some states offer unlimited protection. Others cap exemptions at modest amounts that haven’t kept pace with housing costs.

California, for example, recently updated its homestead exemption. According to competitor analysis, According to competitor sources, California’s homestead exemption ranges from $300,000 to $600,000 depending on the county and housing costs.

According to 11 U.S. Code § 522, under federal exemptions, the debtor’s aggregate interest in a residence cannot exceed $15,000 in value, though this amount has been adjusted periodically for inflation.

The variation matters enormously. A homeowner with $100,000 in equity faces completely different outcomes in California versus a state with a $25,000 exemption cap.

| Exemption Level | Protected Equity | What It Means |

|---|---|---|

| Low exemption states | $5,000–$25,000 | Limited equity protection; higher risk in Chapter 7 for homeowners with substantial equity |

| Moderate exemption states | $50,000–$150,000 | Reasonable protection for median-priced homes; most homeowners can file Chapter 7 safely |

| High exemption states | $300,000–$600,000+ | Strong protection even with significant equity; Chapter 7 rarely threatens homeownership |

| Unlimited exemption states | No cap | Full protection regardless of equity amount; home safe in Chapter 7 if payments current |

Choosing Between Federal and State Exemptions

In states that permit the choice, debtors must evaluate which exemption scheme provides better protection. This isn’t always the one with the higher homestead exemption.

Federal exemptions might offer better protection for other property types — vehicles, retirement accounts, personal property. The homestead exemption is just one piece of the puzzle.

Bankruptcy attorneys run these calculations regularly to determine the optimal exemption strategy.

What Happens to Mortgage Payments During Bankruptcy

Filing bankruptcy doesn’t pause mortgage obligations. The automatic stay prevents foreclosure actions, but it doesn’t eliminate the requirement to pay.

In Chapter 7, debtors must stay current on mortgage payments throughout the case and afterward if they want to keep the home. The bankruptcy discharges personal liability — meaning the lender can’t pursue a deficiency judgment after foreclosure — but the mortgage lien remains enforceable against the property.

Stop paying, and the lender can eventually foreclose once the automatic stay lifts.

Reaffirmation Agreements

Some lenders request reaffirmation agreements in Chapter 7 cases. These agreements reinstate personal liability for the mortgage debt in exchange for the debtor keeping the home.

Reaffirmation isn’t required to keep a house. As long as payments continue, most lenders won’t foreclose on a performing loan even without reaffirmation.

But reaffirmation does have a benefit: it allows continued credit reporting of on-time payments, potentially helping rebuild credit faster after bankruptcy.

Chapter 13 and the Mortgage

In Chapter 13, ongoing mortgage payments typically continue outside the plan. The debtor pays the mortgage company directly each month.

Mortgage arrears, however, get incorporated into the Chapter 13 plan. The trustee receives plan payments and distributes the arrearage portion to the lender over the plan’s duration.

This dual-track approach lets debtors catch up on past-due amounts while keeping current going forward.

Behind on Mortgage Payments? Your Options

Homeowners already facing foreclosure often wonder whether bankruptcy can help. The answer depends on timing and circumstances.

The automatic stay stops foreclosure the moment bankruptcy is filed. Even if a foreclosure sale is scheduled for tomorrow, filing today halts the process.

But this protection is temporary in Chapter 7. Unless the debtor can immediately cure the arrearage and resume payments, foreclosure will eventually proceed once the stay lifts or the bankruptcy concludes.

Chapter 13 offers a better solution for those behind on payments. The arrearage becomes part of the repayment plan, and the lender must accept the proposed cure as long as the plan meets legal requirements.

Loss Mitigation Options

The Federal Trade Commission notes that homeowners facing foreclosure have several options beyond bankruptcy, including loan modifications, forbearance agreements, and repayment plans negotiated directly with lenders.

Sometimes combining these approaches with bankruptcy provides the best outcome. A loan modification that reduces monthly payments paired with a Chapter 13 plan to cure arrears can make homeownership sustainable again.

Second Mortgages and Home Equity Lines of Credit

Chapter 13 offers a unique advantage for dealing with second mortgages: lien stripping.

If the home’s value has dropped below the first mortgage balance, the second mortgage becomes completely unsecured. In that situation, Chapter 13 allows “stripping off” the second mortgage lien entirely.

The second mortgage gets treated as unsecured debt in the plan. After completing the repayment plan and receiving discharge, the lien disappears. The homeowner emerges with only the first mortgage.

This option doesn’t exist in Chapter 7. Only Chapter 13 permits stripping wholly unsecured junior liens from a primary residence.

Investment Properties and Vacation Homes

Homestead exemptions protect only primary residences. Investment properties, rental homes, and vacation properties receive no homestead protection.

In Chapter 7, the trustee can sell non-exempt real estate regardless of equity amount. Someone with $50,000 equity in a rental property faces losing that property even if their primary residence is safe under homestead exemption.

Chapter 13 again provides more flexibility. Non-primary residences can be retained through the repayment plan, though the plan must pay unsecured creditors at least as much as they would have received from liquidating the property in Chapter 7.

Timing Considerations: When to File

Timing matters when filing bankruptcy as a homeowner. Filing too early or too late can create problems.

Homeowners who recently purchased a home with little equity have less to protect. Those who’ve owned for decades and built substantial equity need careful exemption planning.

Similarly, someone facing imminent foreclosure needs to file before the sale occurs. Once the foreclosure sale completes, bankruptcy can’t recover the property.

But rushing to file without proper planning can lead to mistakes — choosing the wrong chapter, missing exemptions, or filing when other debt relief options would work better.

The 90-Day Window

Timing also matters for property transfers. Bankruptcy law allows trustees to undo transfers made to defraud creditors. Transferring a home to relatives shortly before filing bankruptcy triggers scrutiny.

Even legitimate transfers — like selling a home and using the proceeds to pay certain debts — can be unwound if done within suspicious timeframes.

This is why planning matters. Working with a bankruptcy attorney helps avoid timing traps that can complicate or derail the case.

Life After Bankruptcy: Keeping Your Home Long-Term

Successfully navigating bankruptcy and keeping the home is just the first step. Maintaining homeownership afterward requires sustainable finances.

Chapter 7 debtors must afford their mortgage payment without the burden of discharged debts. If that’s not realistic, keeping the home might not make sense even if legally possible.

Chapter 13 debtors must complete their three to five-year plan. That means maintaining steady income and avoiding major financial setbacks throughout the plan period.

Post-Bankruptcy Mortgage Modifications

Some homeowners emerge from bankruptcy still struggling with mortgage payments that strain their budget. Post-bankruptcy loan modifications remain an option.

Lenders are sometimes more willing to modify loans after bankruptcy eliminates other debts, since the homeowner’s ability to pay the mortgage improves without credit card payments, medical bills, and other discharged obligations competing for the same income.

Common Mistakes Homeowners Make

Several errors repeatedly trap homeowners in bankruptcy:

Assuming bankruptcy always means losing the house. This misconception keeps people from seeking relief they desperately need. Most homeowners keep their homes through bankruptcy.

Choosing the wrong chapter. Chapter 7 makes sense for some homeowners. Chapter 13 is better for others. Filing the wrong chapter can lead to losing a home that could have been saved, or spending years in an unnecessary repayment plan.

Failing to account for ongoing costs. Property taxes, insurance, maintenance, and HOA fees continue during and after bankruptcy. Homeowners who focus only on the mortgage payment sometimes can’t sustain total housing costs.

Ignoring trustee communications. Bankruptcy trustees request documentation and information. Ignoring these requests can result in case dismissal, lifting the automatic stay, and losing foreclosure protection.

Stopping mortgage payments after filing. Some debtors misunderstand the automatic stay and think it freezes all obligations. It doesn’t. Mortgage payments must continue.

When Surrendering the Home Makes Sense

Sometimes keeping the home isn’t the right choice. Bankruptcy provides an opportunity to surrender an unaffordable property and walk away from the debt.

This makes sense when:

- Monthly payments consume an unsustainable percentage of income

- The home is severely underwater with no realistic path to building equity

- Maintenance costs and needed repairs exceed budget capacity

- Job relocation or life changes make the property impractical

Surrendering through bankruptcy discharges personal liability. The lender can’t pursue a deficiency judgment for the difference between the home’s sale price and the loan balance.

This provides a clean break that foreclosure alone doesn’t offer.

Working With a Bankruptcy Attorney

Homeowners facing bankruptcy benefit enormously from legal guidance. Bankruptcy law is complex, with numerous rules, exemptions, and procedural requirements.

An experienced bankruptcy attorney can:

- Determine which chapter provides optimal protection for the home

- Calculate available exemptions and equity positions

- Develop strategies for dealing with mortgage arrears

- Identify opportunities like lien stripping in Chapter 13

- Prepare accurate paperwork and court filings

- Represent the debtor at hearings and meetings with the trustee

The cost of an attorney is typically modest compared to the home equity being protected. And for Chapter 13 cases, attorney fees can be paid through the repayment plan rather than upfront.

| Situation | Recommended Chapter | Key Consideration |

|---|---|---|

| Current on mortgage, low equity | Chapter 7 | Quick discharge; keep home with minimal disruption |

| Behind on payments, can afford going forward | Chapter 13 | Cure arrears through plan; prevent foreclosure |

| High equity exceeding exemptions | Chapter 13 | Avoid forced sale; retain property regardless of equity |

| Wholly unsecured second mortgage | Chapter 13 | Strip second lien; eliminate that debt entirely |

| Cannot afford payments even after discharge | Either (with surrender) | Discharge liability; walk away cleanly |

Frequently Asked Questions

Yes, in most cases. If mortgage payments are current and home equity doesn’t exceed the homestead exemption, Chapter 7 allows keeping the home while discharging other debts. Payments must continue during and after bankruptcy. High equity situations may require Chapter 13 instead to prevent forced sale by the trustee.

Filing bankruptcy triggers an automatic stay that immediately stops foreclosure proceedings, even if a sale is scheduled. Chapter 7 provides temporary relief but doesn’t cure mortgage arrears. Chapter 13 allows spreading the arrearage over three to five years through a repayment plan, making it the better option for homeowners behind on payments who want to keep the property.

This depends on state law. Homestead exemptions range from a few thousand dollars in some states to $600,000 or more in others. Some states offer unlimited homestead protection. Debtors in states allowing the choice can select between state and federal exemptions. Consulting a local bankruptcy attorney provides specific exemption amounts for your situation.

Yes, temporarily. The automatic stay prevents all collection actions, including foreclosure, from the moment of filing. In Chapter 7, this protection lasts only during the bankruptcy case, typically a few months. In Chapter 13, the stay continues throughout the three to five-year repayment plan as long as plan payments and current mortgage payments continue.

Chapter 13 allows lien stripping when a second mortgage is wholly unsecured — meaning the home’s value is less than the first mortgage balance. In that situation, the second mortgage gets reclassified as unsecured debt in the Chapter 13 plan. After completing the plan and receiving discharge, the second mortgage lien is eliminated entirely. This option does not exist in Chapter 7.

Not necessarily. In Chapter 7, equity exceeding homestead exemptions creates risk of the trustee selling the property. Chapter 13 provides an alternative that allows keeping the home regardless of equity amount. The Chapter 13 plan must pay unsecured creditors at least what they would have received from liquidating the equity, but the home itself isn’t sold.

Bankruptcy itself doesn’t reduce mortgage payments. Chapter 13 can spread arrears over time, making payments more manageable, but the regular monthly payment continues. If the mortgage is fundamentally unaffordable, surrendering the home through bankruptcy and discharging the liability might be the wisest choice. Post-bankruptcy loan modifications are also possible once other debts are eliminated.

Final Thoughts: Making the Right Choice for Your Home

Bankruptcy and homeownership aren’t mutually exclusive. Thousands of people file bankruptcy each year and successfully retain their homes.

The key is understanding how different bankruptcy chapters treat real estate, knowing your state’s exemption laws, and realistically assessing whether keeping the home makes financial sense.

Chapter 7 works well for homeowners current on payments with modest equity. Chapter 13 is designed specifically to help people catch up on arrears and prevent foreclosure.

Neither chapter automatically strips away homeownership. But both require ongoing mortgage payments and meeting specific obligations.

For anyone considering bankruptcy while worried about their house, the first step is gathering information. Calculate your home equity. Research your state’s homestead exemption. Evaluate whether mortgage payments are sustainable without other debts.

Then consult with a bankruptcy attorney who can analyze your specific situation and recommend the best path forward. The consultation alone often provides clarity about options and outcomes.

Bankruptcy exists to provide a fresh start. For many homeowners, that fresh start includes keeping the roof over their head.