Quick Summary: In most cases, you can legally keep insurance money without making repairs, unless your mortgage lender holds the funds or your policy requires specific repairs. However, failing to repair covered damage can lead to denied future claims, policy cancellation, and potential loan agreement violations if your property is financed.

Receiving an insurance payout after damage to your home or vehicle feels like a financial win. But what happens if you pocket the money instead of making repairs?

The answer isn’t always straightforward. It depends on who owns your property, what your policy says, and whether you plan to file future claims for the same damage.

Here’s what you need to know about the legal and practical consequences of not using insurance money for its intended purpose.

The Legal Reality: Can You Keep Insurance Money Without Repairs?

Technically, there’s no federal law that requires property owners to use insurance payouts for repairs. If you own your home or vehicle outright — meaning no mortgage or auto loan — the money is generally yours to keep.

Insurance companies compensate for loss, not necessarily repairs. Once they’ve assessed the damage and issued payment, the decision about how to spend those funds falls to the policyholder in many situations.

That said, this freedom comes with important exceptions and risks.

When Your Lender Controls the Money

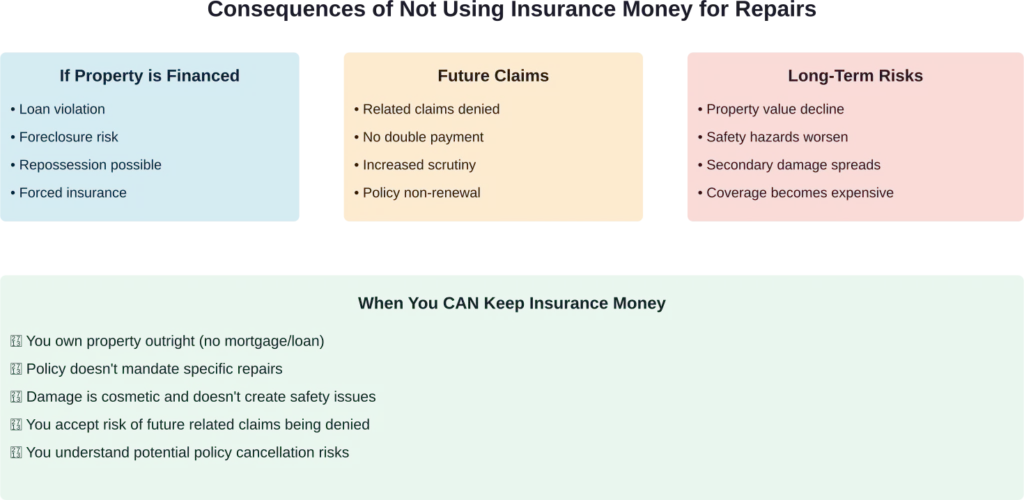

If you’re still paying off a mortgage or car loan, your lender has a financial interest in the property. Most loan agreements require you to maintain the collateral in good condition.

For mortgaged homes, insurance checks are often made out to both you and your mortgage company. The lender typically holds these funds in escrow and releases them incrementally as repairs progress and contractors submit completion documentation.

With financed vehicles, the process works similarly. The insurance check may list both you and the lienholder as payees, requiring both signatures to cash it.

Failing to complete repairs when your lender requires them can violate your loan agreement, potentially triggering:

- Demands for immediate loan repayment

- Foreclosure proceedings on real property

- Vehicle repossession

- Forced-place insurance at higher premiums

What Insurance Companies Can Do If You Don’t Repair Damage

Even when you own property outright, insurance companies have tools to protect themselves from ongoing risk associated with unrepaired damage.

Future Claims May Be Denied

This is where things get tricky. If you keep insurance money without making repairs, any future claims related to that same damage will almost certainly be denied.

For example, imagine you receive a payout for roof damage from a hailstorm but never fix the roof. Six months later, water damage appears in your ceiling. Your insurer can legitimately deny the water damage claim because the root cause — the unrepaired roof — was previously compensated.

Insurers aren’t obligated to pay twice for the same loss or for damage that results from your failure to mitigate initial covered damage.

Policy Cancellation or Non-Renewal

Insurance companies assess risk continuously. A property with known, unrepaired damage presents increased risk.

Your insurer may choose not to renew your policy at the end of the term if significant damage remains unaddressed. In some cases, they might cancel mid-term if the unrepaired damage substantially increases the risk of future losses.

Once cancelled for this reason, finding affordable replacement coverage becomes significantly harder.

When Keeping Insurance Money Makes Sense

There are legitimate situations where not making repairs is reasonable.

Minor Cosmetic Damage

Small dents on a paid-off vehicle or minor aesthetic damage to a home you own outright might not warrant repairs. If the damage doesn’t affect functionality or safety, keeping the money is often acceptable.

Just understand that future claims involving that area may face additional scrutiny.

When Repair Costs Are Lower Than the Payout

Sometimes the insurance estimate exceeds actual repair costs. After completing repairs for less than the payout amount, the remaining funds are typically yours to keep.

This isn’t misuse — it’s simply efficient management of the claim. The damage was addressed; you just found a better price.

Total Loss Situations

If your vehicle is totaled or your home is deemed a total loss, there’s no expectation to rebuild or repair. The payout compensates for your loss, and how you use those funds is your decision (subject to lender requirements if applicable).

The FTC’s Warning About Service Contracts

It’s worth noting that insurance claim issues extend beyond traditional property insurance. According to the Federal Trade Commission, in December 2025, the FTC sent 168,179 checks totaling more than $9.6 million to eligible people who paid CarShield for a vehicle service contract between September 2019 and September 2024 and had their claim denied.

The FTC found that CarShield’s advertising promised customers would “never pay for expensive car repairs again,” but many customers found their claims were denied. This case highlights the importance of understanding exactly what your coverage promises and what circumstances might lead to denied claims.

What to Do If You Can’t Afford Repairs

Sometimes the insurance payout doesn’t fully cover repair costs, or financial hardship makes it impossible to complete repairs immediately.

Here’s what to consider:

Contact your insurance company. Explain the situation. Some insurers offer extended timelines for completing repairs or can reassess the damage for a more accurate payout.

Talk to your lender. If you have a mortgage or loan, communicate proactively about delays. Some lenders may work with you on payment plans or timelines.

Prioritize safety-critical repairs. Even if you can’t fix everything, address structural issues, water intrusion points, or safety hazards first. Partial repairs are better than none when it comes to preventing secondary damage.

Document everything. If you’re making some repairs but not others, keep detailed records of what was fixed and why certain items were deferred.

Potential Legal Consequences

While rare, there are situations where not using insurance money for repairs could create legal problems beyond denied claims.

| Situation | Potential Consequence | Who Can Take Action |

|---|---|---|

| Unrepaired damage violates HOA rules | Fines, liens on property | Homeowners Association |

| Unsafe conditions remain unaddressed | Code violations, condemnation | Local building department |

| Breach of loan agreement terms | Loan acceleration, foreclosure | Mortgage lender or lienholder |

| Damage affects neighboring properties | Liability claims, lawsuits | Neighbors or affected parties |

Does Your Policy Require Repairs?

Some insurance policies include specific language requiring repairs for certain types of damage. Review your policy documents carefully.

According to the Magnuson-Moss Warranty Act and related Federal Trade Commission regulations, warranties and service contracts must clearly disclose their terms. Similarly, insurance policies must specify any obligations you have regarding repairs.

If your policy states that you must repair certain categories of damage to maintain coverage, that contractual obligation is enforceable.

Frequently Asked Questions

Yes, if you own your vehicle outright with no loan, you can generally keep the insurance payout without making repairs. However, any future claims related to that unrepaired damage will likely be denied, and your insurer may choose not to renew your policy.

Your insurer won’t necessarily monitor whether repairs were completed, but they’ll discover unrepaired damage if you file another claim or during policy renewal inspections. This can result in denied claims or policy cancellation.

If you complete repairs for less than the insurance payout, the remaining money is typically yours to keep. This isn’t considered misuse because the damage was actually repaired. Just keep documentation of the completed work.

Yes. Most mortgage agreements require you to maintain the property in good condition. Your lender can hold insurance funds in escrow and release them only as repairs progress, or potentially accelerate your loan if you refuse to make necessary repairs.

Partial repairs create a gray area. If you address the most critical damage but skip cosmetic fixes, this may be acceptable depending on your lender’s requirements and policy terms. Document what repairs were completed and why others were unnecessary or deferred.

Simply not making repairs isn’t fraud. Fraud occurs when you misrepresent facts to obtain payment — such as claiming damage that never occurred or exaggerating losses. If you legitimately had covered damage and received an appropriate payout, choosing not to repair isn’t fraudulent, though it may violate other agreements.

There’s no universal timeline, but lenders typically expect repairs within a reasonable period, often 6-12 months. Your insurance policy or loan agreement may specify timeframes. If you need more time, communicate with your insurer and lender proactively.

The Bottom Line on Insurance Money and Repairs

Whether you can legally keep insurance money without making repairs depends heavily on your specific circumstances. Property owners with no mortgage or lien have the most freedom, but even they face risks of denied future claims and policy cancellation.

The safer approach? Use insurance money for its intended purpose. Repairs protect your property value, maintain your coverage, and keep you in compliance with loan agreements.

If financial constraints or other circumstances make repairs impossible, communication is critical. Talk to your insurer, your lender, and potentially a legal professional who specializes in insurance disputes.

Don’t assume that silence is safe. The consequences of unrepaired damage often emerge months or years later, when you file another claim or face policy cancellation at the worst possible time.