Quick Summary: If you’re audited without receipts, the IRS may disallow deductions and assess additional taxes, penalties, and interest. However, you can reconstruct records using bank statements, credit card statements, calendar entries, and other documentation. The IRS accepts alternative evidence for legitimate expenses, though lack of documentation often triggers a 20% negligence penalty.

An IRS audit notice in the mail triggers immediate panic for most taxpayers. But when that audit arrives and your receipts are missing, incomplete, or nonexistent? That’s a whole different level of stress.

Here’s the thing though—missing receipts don’t automatically mean disaster. Each year, about 6 million taxpayers have their tax return questioned by the IRS, either by audit or by a verification notice from the IRS. Many of them don’t have perfect documentation. The outcome depends entirely on how you respond.

This guide breaks down exactly what happens when you’re audited without receipts, how the IRS evaluates alternative evidence, and concrete steps to reconstruct your records and minimize penalties.

Understanding IRS Audits and Documentation Requirements

The IRS conducts audits to verify that tax returns accurately reflect income and deductions. Not all audits are created equal, and the type you receive significantly impacts what happens next.

Audits generally fall into three categories: correspondence audits handled entirely by mail, office audits requiring a meeting at an IRS office, and field audits where an agent visits your home or business. The complexity of your return and the issues flagged determine which type you’ll face.

According to the IRS, certain red flags increase audit likelihood. Businesses with revenue exceeding $5 million and net income above $1 million face higher scrutiny because the potential tax recovery justifies the IRS resources invested. Excessive business expenses, large variations in income between years, and substantial deductions relative to income all trigger algorithmic reviews.

Real estate professionals claiming unlimited use of rental property loss deductions face particular scrutiny. The IRS has successfully won numerous cases where adequate records weren’t maintained to prove special status.

What Documentation the IRS Expects

The IRS expects taxpayers to maintain records substantiating all income, deductions, and credits claimed. For business expenses, this typically means receipts showing the amount, date, place, and business purpose of each transaction.

But receipts aren’t the only acceptable documentation. Bank statements, credit card statements, canceled checks, invoices, and even calendar entries can serve as supporting evidence when combined strategically.

The key is creating a clear trail connecting the claimed deduction to actual business or tax-deductible activity.

What Actually Happens When You Don’t Have Receipts

So what’s the real-world consequence of missing receipts during an audit? The answer depends on several factors: the type of expenses involved, the alternative documentation available, and how you respond to the audit.

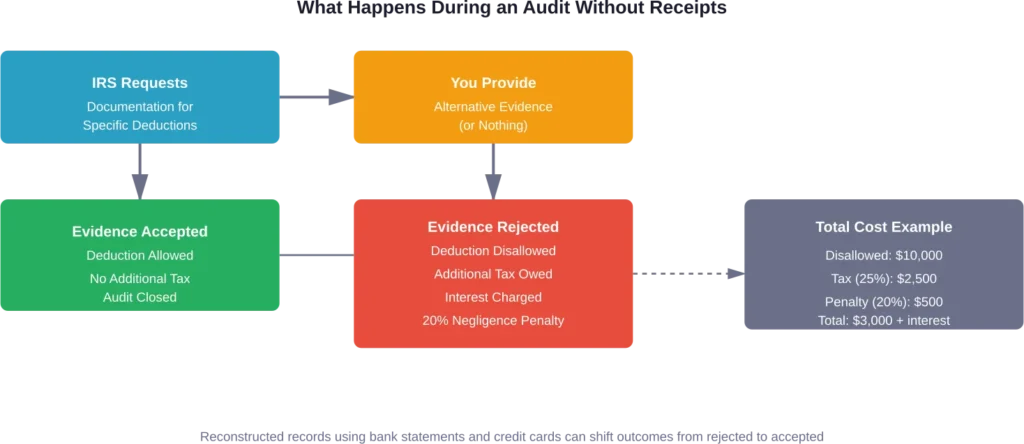

The IRS will request documentation for specific line items on your return. When you can’t produce receipts, the auditor evaluates whatever alternative evidence you provide. If that evidence sufficiently demonstrates the expense was legitimate and properly deductible, the IRS may accept it.

When evidence is insufficient or nonexistent, the IRS disallows the deduction. This creates additional taxable income, which means you owe more tax on that amount. The IRS then calculates interest on the unpaid tax from the original due date of the return.

The Negligence Penalty

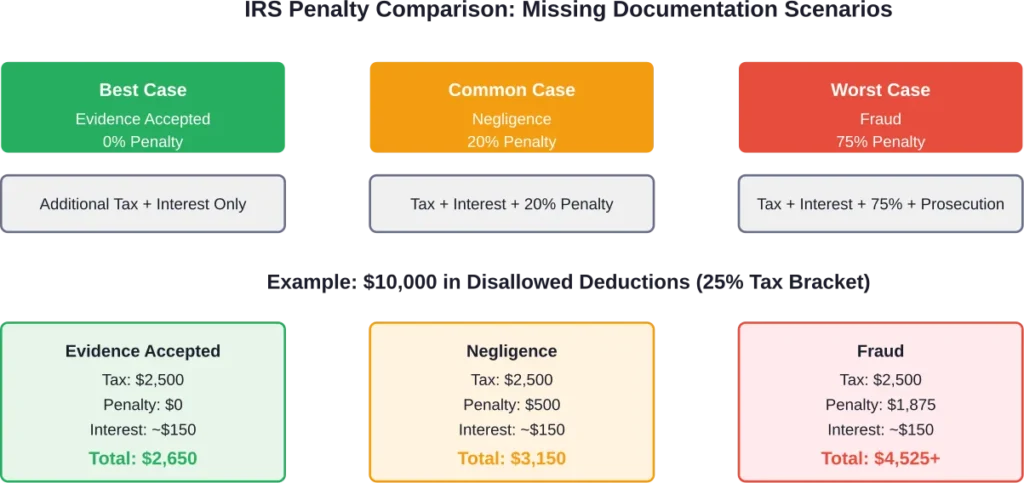

Here’s where it gets expensive. Lack of records often leads to a 20% IRS negligence penalty under accuracy-related penalty provisions. under accuracy-related penalty provisions. According to IRS guidelines, negligence occurs when taxpayers don’t make a reasonable attempt to comply with tax laws or fail to keep adequate records.

This penalty applies to the portion of underpayment attributable to negligence. If disallowed deductions create $10,000 in additional tax liability, the negligence penalty adds another $2,000.

The accuracy-related penalty framework includes several categories beyond negligence: substantial understatement of income tax, substantial valuation misstatements, and substantial overstatement of pension liabilities. For most individual taxpayers facing receipt issues, the negligence provision is what applies.

How to Reconstruct Your Records

The moment you receive an audit notice, start gathering alternative documentation immediately. The reconstruction process takes time, and the IRS typically gives 30 days to respond to audit requests.

Bank statements form the foundation of record reconstruction. Download or request statements covering the audit period. Review every transaction and highlight those related to the questioned deductions.

Credit card statements provide similar value. They show the merchant name, transaction date, and amount—three of the four critical documentation elements. What’s missing is the business purpose, which you’ll need to establish through other means.

Building Your Documentation Package

Calendar entries, emails, and contemporaneous notes help establish business purpose. If you claimed a meal deduction for a client meeting, calendar entries showing the meeting and emails confirming attendance support your case.

For mileage deductions without a log, reconstruct trips using appointment calendars, client addresses, and mapping tools. While not as strong as contemporaneous mileage logs, this approach demonstrates a good-faith effort to substantiate legitimate expenses.

Invoices from vendors serve as excellent supporting documentation. If you claimed equipment purchases, vendor invoices combined with bank statements showing payment create a complete picture.

Here’s what you can likely reconstruct versus what becomes problematic:

| Expense Type | Reconstruction Difficulty | Alternative Documentation Options |

|---|---|---|

| Equipment purchases | Easy | Bank statements, invoices, credit card records |

| Business meals | Moderate | Credit card statements, calendar entries, attendee confirmations |

| Travel expenses | Moderate | Hotel confirmations, flight receipts (request duplicates), credit card records |

| Mileage | Difficult | Calendar reconstruction, appointment records, client addresses |

| Cash expenses | Very Difficult | Contemporaneous notes, patterns in similar documented expenses |

| Small daily expenses | Nearly Impossible | Limited options; IRS may allow de minimis amounts with explanation |

The Cohan Rule

In certain circumstances, courts have allowed estimated deductions when taxpayers clearly incurred deductible expenses but lack precise documentation. This principle, stemming from a 1930 court case involving entertainer George M. Cohan, permits reasonable estimation.

But don’t count on it. The IRS applies Cohan estimates restrictively, and the rule doesn’t apply to certain expense categories that explicitly require documentation, like travel, meals, and listed property.

Responding to the Audit Notice: Step-by-Step

Your response to the audit notice determines the entire trajectory of the process. Here’s how to approach it methodically.

Read the notice completely. The IRS specifies exactly which items they’re questioning and what documentation they want. Don’t provide unrelated documents or volunteer information about items not under review.

Organize your reconstructed records chronologically. Create a clear index showing which documents support which deductions. The easier you make the auditor’s job, the better your outcome.

Write a cover letter explaining your documentation situation. If receipts were destroyed in a fire, flood, or computer failure, state that clearly. Explain what alternative documentation you’re providing and why it substantiates the expense.

What to Say (and Not Say)

Stick to facts. Don’t make excuses or create elaborate stories about why records are missing. Auditors have heard everything, and credibility matters enormously.

If you made an honest mistake, acknowledge it. The IRS distinguishes between negligence and fraud. Negligence carries a 20% penalty; fraud carries a 75% penalty plus potential criminal prosecution.

Never claim you don’t remember or have no idea about an expense. Instead, explain what you do know and provide whatever supporting documentation exists.

Penalties and Consequences You Might Face

Beyond the negligence penalty, several other consequences can arise from audits with missing documentation.

Interest accumulates on unpaid tax from the original return due date. Interest accrues on unpaid tax from the original return due date at rates set by the IRS. This compounds daily, making delays expensive.

According to IRS penalty provisions, substantial understatement penalties apply when the tax understatement exceeds the greater of 10% of the correct tax or $5,000. For taxpayers claiming Section 199A Qualified Business Income Deduction on your tax return, the penalty applies if you understate your tax liability by 5% of the tax required to be shown on your return or $5,000, whichever is greater.

In severe cases involving intentional disregard of rules or fraudulent intent, civil fraud penalties reach 75% of the underpayment attributable to fraud. The IRS must prove fraud by clear and convincing evidence—a high standard, but one they pursue when warranted.

When Professional Help Becomes Critical

Some audit situations demand professional representation. Tax professionals, enrolled agents, and CPAs can represent taxpayers before the IRS, negotiate on their behalf, and often achieve better outcomes than individuals representing themselves.

Consider professional help when the audit involves complex business expenses, substantial amounts of money, or multiple tax years. Professionals understand IRS procedures, know what documentation the IRS accepts, and can argue effectively for reasonable accommodations.

Tax professionals also help argue against penalties by demonstrating reasonable cause. Under IRS penalty relief provisions, penalties can be abated when taxpayers show they made a good-faith effort to comply despite the missing documentation.

The cost of professional representation typically ranges from a few hundred dollars for simple correspondence audits to several thousand for complex field audits. Weigh this against the potential tax, penalties, and interest at stake.

Preventing Future Audit Issues

The best audit strategy is never needing one. Implementing proper record-keeping systems now prevents documentation nightmares later.

Digital receipt capture tools photograph and organize receipts immediately. Apps sync with accounting software, categorize expenses automatically, and create cloud backups immune to physical loss.

For business expenses, note the business purpose on the receipt immediately. Who attended the meal? What business was discussed? This contemporaneous notation proves invaluable during audits.

Maintain separate bank accounts and credit cards for business use. Commingled personal and business expenses complicate audits enormously. Clean separation makes documentation straightforward.

Required Retention Periods

The IRS generally has three years from the return filing date to initiate an audit. For substantial income understatement (more than 25% of gross income), this extends to six years. No statute of limitations exists for fraudulent returns or unfiled returns.

Best practice: retain all tax records for seven years. This covers extended audit periods and provides documentation for amended returns if needed.

Your Rights During an Audit

Taxpayers have specific rights during IRS examinations, outlined in the Taxpayer Bill of Rights. Understanding these protections helps navigate the audit process.

You have the right to professional representation. The IRS cannot require you to appear personally or prohibit representation by authorized practitioners.

You have the right to know why the IRS is requesting information, how they’ll use it, and what happens if you don’t provide it. Auditors must explain their findings and provide time to respond before finalizing assessments.

The Taxpayer Advocate Service provides independent assistance when taxpayers experience significant hardship or cannot resolve issues through normal IRS channels. This free service helps when audits become unreasonably burdensome.

Appealing Audit Findings

Disagreeing with audit findings doesn’t end the process. Multiple appeal levels exist before any final determination.

After the auditor issues findings, you receive a 30-day letter explaining proposed changes and your appeal rights. Responding within 30 days preserves your right to appeal within the IRS before involving the courts.

The IRS Independent Office of Appeals reviews cases with fresh eyes. Appeals officers often settle cases when reasonable documentation exists, even if the original auditor was inflexible.

If the IRS issues a Notice of Deficiency (90-day letter), you can petition the United States Tax Court without first paying the disputed amount. This stops collection activity while the case is litigated.

For amounts already paid, taxpayers can file refund claims and, if denied, sue in federal district court or the Court of Federal Claims.

Special Situations and Edge Cases

Certain circumstances create unique challenges during audits without receipts.

Natural disasters that destroy records qualify for reasonable cause penalty relief. FEMA-declared disaster areas and documented losses support penalty abatement requests. The IRS recognizes that taxpayers cannot maintain records destroyed by circumstances beyond their control.

Digital record loss from computer failures or ransomware attacks receives similar consideration when taxpayers demonstrate they maintained reasonable backup practices. Simply losing files due to poor digital hygiene offers less protection.

For taxpayers who relied on preparers who promised to maintain records, the IRS typically holds the taxpayer responsible. The tax code places recordkeeping obligations on taxpayers, not preparers, regardless of representations made.

Statute of Limitations Considerations

When reconstructing records, the IRS’s assessment statute matters. If the three-year assessment period is approaching expiration, the IRS may accelerate the audit process or request a statute extension.

Agreeing to extend the statute gives more time to gather documentation. Refusing can force the IRS to make assessments based on available information, potentially resulting in larger adjustments than necessary.

Weigh the trade-offs with professional guidance. Extended statutes provide reconstruction time but prolong uncertainty.

Frequently Asked Questions

Yes, the IRS can audit you regardless of whether you have receipts. The audit examines your tax return’s accuracy, and missing receipts don’t prevent the IRS from questioning deductions. However, providing alternative documentation like bank statements, credit card records, and invoices can substantiate expenses even without original receipts.

The IRS typically has three years from the return filing date to initiate an audit, extending to six years if substantial income understatement exceeds 25% of gross income. There’s no statute of limitations for fraudulent returns. Missing receipts don’t change these timeframes, but they may affect the audit outcome.

When the IRS disallows deductions, the amount becomes taxable income. You’ll owe additional tax on that income, plus interest calculated from the original return due date. A 20% negligence penalty typically applies when inadequate records cause the underpayment, substantially increasing the total amount owed.

Bank statements can serve as supporting documentation, especially when combined with other evidence. They prove payment occurred and show the amount and date, but you’ll need to establish the business purpose through calendar entries, emails, invoices, or other contemporaneous records. Bank statements alone rarely suffice, but they form a strong foundation for reconstructed documentation.

In limited circumstances, courts have permitted estimated deductions when taxpayers clearly incurred deductible expenses but lack precise documentation. This Cohan rule applies restrictively, and the IRS excludes certain expense categories that require specific documentation, including travel, meals, entertainment, and listed property. Never rely on estimation as a primary strategy.

Reconstruct mileage using appointment calendars, client addresses, invoice dates, and mapping software to calculate distances. While contemporaneous mileage logs carry more weight, reconstructed logs demonstrating a good-faith effort to substantiate legitimate business travel can be persuasive, especially when corroborated by appointment records and calendar entries.

Read the notice completely to understand which items the IRS is questioning. Immediately begin gathering all available documentation: bank statements, credit card statements, invoices, calendar entries, and emails. Organize records chronologically by expense category. Consider consulting a tax professional, especially if substantial amounts or complex issues are involved. Respond within the specified timeframe, typically 30 days.

Taking Control of the Situation

Facing an audit without receipts feels overwhelming. But the outcome isn’t predetermined.

The IRS wants to determine the correct tax liability. When you can demonstrate expenses were legitimate through alternative documentation, auditors often work with you to reach a fair resolution.

Start reconstruction immediately. Bank statements, credit card records, and contemporaneous notes create a documentation package that, while not perfect, demonstrates good faith and substantiates legitimate business expenses.

Don’t ignore the audit notice. Failure to respond results in automatic assessment of the full proposed adjustment plus penalties. Engagement provides opportunities for explanation, negotiation, and potentially reduced liabilities.

Consider professional representation for complex situations or significant dollar amounts. Tax professionals navigate IRS procedures daily and often achieve better outcomes than individuals handling audits alone.

The 20% negligence penalty isn’t automatic. Demonstrating reasonable cause and good-faith compliance efforts can result in penalty abatement even when some deductions are disallowed.

Looking forward, implement proper record-keeping systems now. Digital tools make receipt capture and organization simple, creating contemporaneous documentation that withstands audit scrutiny. Seven years seems like a long retention period until you need those records—then it seems essential.

An audit without receipts creates challenges, not impossibilities. Methodical reconstruction, professional guidance when needed, and honest engagement with the process provide a clear path through even difficult audit situations.