Quick Summary: If you mobile deposit a fake check, your bank will reverse the funds once the check bounces—typically within days or weeks. You’re legally responsible for repaying the full amount plus overdraft fees, even if you were scammed. Knowingly depositing fake checks is bank fraud punishable by fines and prison time, while unknowing victims face financial losses and potential account closure.

Mobile deposit technology has made banking remarkably convenient. Snap a photo, upload it, and funds appear in your account within minutes.

But here’s the thing—that convenience has created massive vulnerabilities. Scammers exploit the delay between when funds become available and when banks actually verify the check’s legitimacy.

According to research from the Center for Problem-Oriented Policing, financial institutions reported a 400% increase in check fraud through remote deposit capture (RDC) from 2012 to 2014.[3] This trend was documented through 2014, though current rates should be verified with recent financial institution data.

The Immediate Aftermath: What Banks Do When They Detect Fraud

When you mobile deposit a check, your bank doesn’t instantly verify its authenticity. The Federal Reserve’s Check 21 Act allows banks to process digital images of checks, but verification takes time.

Initially, the funds might appear available in your account. This is where things get dangerous.

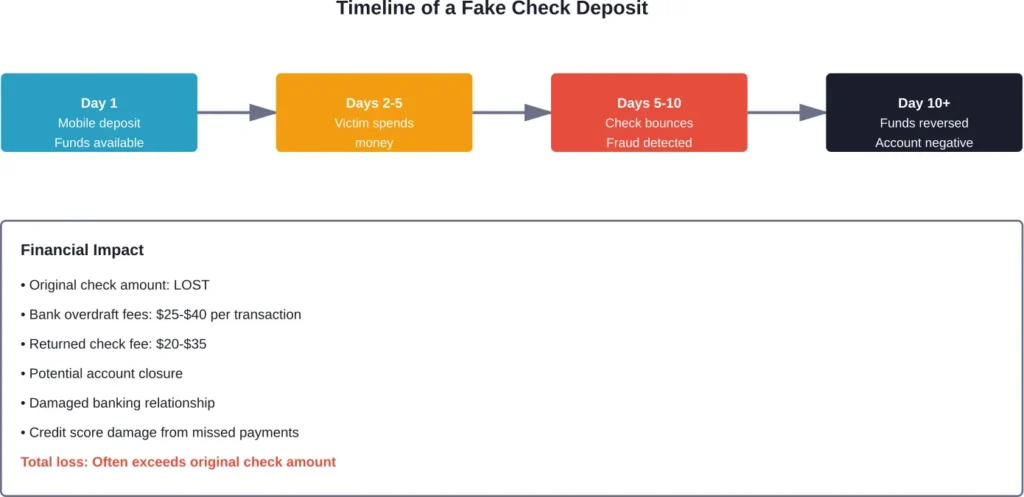

Banks typically make a portion of deposited funds available quickly—sometimes within one business day. But the actual clearing process can take several days or even weeks. During this window, the issuing bank examines the check for fraud indicators.

Once fraud is detected, the consequences are swift and unforgiving.

Fund Reversal and Account Holds

The bank will immediately reverse the deposited amount from your account. If you’ve already spent the money, your account goes negative—potentially by thousands of dollars.

According to the Federal Reserve Board, if a bank finds it incorrectly charged your account, it must refund the amount within one business day. But when fraud is confirmed? That protection doesn’t apply. The responsibility falls entirely on the depositor.

Your account will likely be frozen or placed under restriction while the bank investigates. This can prevent you from accessing legitimate funds and making routine transactions.

Financial Consequences: The Real Cost of Fake Checks

The financial damage extends far beyond the check amount itself.

First, there’s the original deposit amount that gets reversed. If the fake check was for $1,900 (a common amount in employment scams), that entire sum disappears from your account.

But wait. The fees compound quickly:

| Fee Type | Typical Amount | When It Applies |

|---|---|---|

| Returned deposit fee | $20-$35 | Per fake check deposited |

| Overdraft fees | $25-$40 | Each transaction after account goes negative |

| Extended overdraft fee | $15-$40 | If account stays negative 5+ days |

| Account closure fee | $0-$50 | If bank terminates your account |

According to user experiences in banking forums, victims often send money to scammers via wire transfer or payment apps before the check bounces. That money is gone permanently—banks won’t reimburse you for willingly sending funds to criminals.

Credit Score Damage

If you relied on the fake check funds to pay bills, you’ll miss payment deadlines when the money vanishes. Payment history is a major factor in credit scoring models, affecting your score significantly.

One missed payment can drop your score 50-100 points. Multiple missed payments? The damage multiplies.

Legal Consequences: Criminal Charges and Prosecution

This is where things get serious. Real talk: depositing fake checks can result in federal criminal charges.

The Department of Justice prosecutes check fraud under 18 U.S.C. § 1344 (bank fraud) and § 1343 (wire fraud). These aren’t minor offenses.

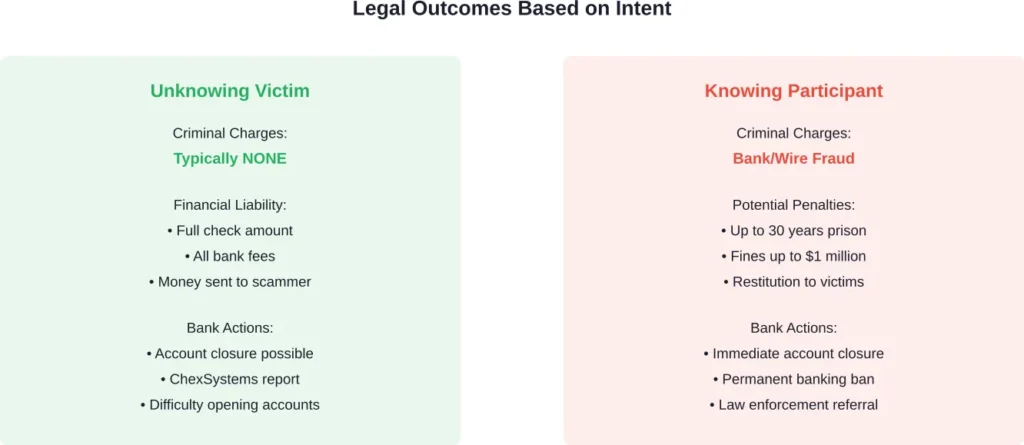

Knowingly vs. Unknowingly Depositing Fake Checks

The critical factor is intent. Did you know the check was fake?

If you knowingly deposited counterfeit checks, you’re facing serious federal charges. Bank fraud under 18 U.S.C. § 1344 carries serious federal penalties. The Department of Justice has prosecuted cases resulting in significant prison sentences and fines.

The Department of Justice reported sentencing a New York man to 10 years in prison for a check fraud scheme. These cases aren’t hypothetical—prosecutors actively pursue them.

But what if you genuinely didn’t know?

Unknowing victims typically don’t face criminal charges, but they’re not off the hook financially. Banks hold depositors responsible regardless of intent. The account holder bears the loss.

How Mobile Deposit Scams Actually Work

Understanding the mechanics helps you spot the red flags. These scams follow predictable patterns.

The Federal Trade Commission identifies several common scenarios where fake checks appear legitimate initially.

Employment and Mystery Shopper Scams

Scammers pose as employers offering remote work. They send a check for equipment purchases or evaluation assignments. The victim deposits the check, buys items or evaluates money transfer services, then discovers the check was counterfeit days later.

In one documented case, a job applicant received a check for equipment purchase as part of a fake employment offer. The applicant deposited it, sent money via Zelle, and when the check bounced, the funds were lost.

Overpayment Scams

Someone “accidentally” sends you a check for more than owed. They ask you to deposit it and return the excess. The original check bounces, but the money you sent is gone.

This happens frequently with online marketplace sales and rental agreements.

Prize and Lottery Scams

Congratulations, you’ve won! But there’s a processing fee or taxes to pay first. The scammer sends a check to cover these costs, asking you to forward a portion to claim your prize.

Spoiler: there’s no prize. Just a fake check and your missing money.

Warning Signs of Fake Check Scams

Certain patterns should immediately trigger suspicion.

According to the U.S. Postal Inspection Service, scammers use sophisticated software and commercial printers to create convincing counterfeits. Visual inspection alone isn’t reliable.

Instead, watch for these behavioral red flags:

- Someone you don’t know sends you a check and asks you to send money elsewhere

- A check amount exceeds what’s owed, with instructions to return the difference

- Pressure to act immediately before the check clears

- Employment offers requiring you to purchase equipment or evaluate money transfers

- Prize notifications requiring upfront payment of fees or taxes

- Requests to use wire transfers, gift cards, or cryptocurrency for refunds

- Communication only through email or text, never phone or in-person meetings

The common thread? Someone sends you money then asks for some back. That’s the scam signature.

What to Do If You’ve Already Deposited a Fake Check

Speed matters. The faster you act, the better your chances of limiting damage.

Contact your bank immediately. Explain the situation before the check bounces. Some banks may work with you if you report the fraud proactively rather than waiting for discovery.

Don’t spend the deposited funds, even if they show as available. That money isn’t real until the check fully clears—which can take weeks.

If you’ve already sent money to the scammer:

- Contact the payment service immediately (Zelle, Venmo, wire transfer company)

- Request a reversal or freeze on the transaction

- File a fraud report with your bank

- Report the scam to the FTC at ReportFraud.ftc.gov

- File a complaint with the U.S. Postal Inspection Service if mail was involved

- Contact local law enforcement to file a police report

Document everything: emails, text messages, check images, receipts, and correspondence with the scammer.

Protecting Yourself from Mobile Deposit Fraud

Prevention beats recovery every time.

Never deposit checks from people you don’t know personally. Period. Legitimate businesses and employers don’t operate this way.

If someone needs to pay you, insist on verified payment methods: direct deposit to your account using official payroll systems, or payment apps where you can verify the sender’s identity.

For online sales, use platform-integrated payment systems that offer buyer and seller protection. Avoid accepting personal or cashier’s checks from strangers.

Wait for checks to fully clear before assuming funds are available. Ask your bank about their specific clearing timeline for mobile deposits.

Many experts suggest treating any check-plus-refund scenario as fraudulent by default. No legitimate transaction requires this structure.

Frequently Asked Questions

Eventually, yes. Banks verify checks with the issuing institution during the clearing process. However, this verification can take several days to weeks, which is why funds may appear available before fraud is detected. Advanced counterfeit checks often pass initial automated screening.

Unknowing victims typically don’t face criminal prosecution. However, depositors remain financially liable for the full amount plus fees regardless of intent. Banks and law enforcement distinguish between victims and knowing participants based on evidence and circumstances.

Generally, fake checks bounce within 5-10 business days, though some take several weeks. Banks may make funds available in 1-2 days, but full verification occurs later during the clearing process when the issuing bank identifies the fraud.

Recovery is difficult but not impossible. Contact the payment service immediately and file fraud reports with your bank, the FTC, and law enforcement. Wire transfers and cryptocurrency are rarely recoverable, while some payment apps may reverse recent transactions if reported quickly.

The bank reverses the deposited funds, potentially putting your account into negative balance. Repeated incidents may result in account closure and reporting to ChexSystems, making it difficult to open accounts at other banks for several years.

The risk of accepting a fake check is identical regardless of deposit method. However, mobile deposit makes it easier for scammers to operate remotely without face-to-face interaction, and the speed of fund availability can create false confidence before verification completes.

Contact the issuing bank directly using a phone number you find independently (not one provided by the check sender) and verify the check with the account holder’s permission. Better yet, refuse checks from unknown parties entirely and insist on verified electronic payment methods.

The Bottom Line on Fake Check Mobile Deposits

Mobile depositing a fake check creates immediate financial liability and potential legal exposure. Banks will reverse fraudulent deposits, hold you responsible for the full amount, and may close your account.

The convenience of mobile banking doesn’t change fundamental fraud risks. Scammers exploit the gap between fund availability and verification completion.

Protection requires skepticism and strict personal policies: never accept checks from strangers, never send money based on unverified deposits, and always verify payment sources through independent channels.

If you’ve been targeted, report it immediately to your bank, the FTC, and law enforcement. Speed matters in limiting damage and potentially recovering funds.

Stay informed about common scam patterns and remember—if someone sends you money then asks for some back, it’s fraud. No exceptions.