Quick Summary: Banks are not obligated to accept checks older than six months—called stale checks—but they may still choose to process them at their discretion. If a stale check is deposited and accepted, it typically clears normally, but it can also be rejected, potentially resulting in fees. The safest approach is contacting the check issuer for a replacement rather than attempting to deposit an expired check.

You’ve just discovered an old check buried in a drawer, behind the couch cushions, or tucked inside a book you haven’t opened in ages. The date? Eight months ago. Maybe longer.

Before you rush to deposit it, here’s what you need to know. That check might be what banks call “stale,” and trying to deposit it could lead to complications you’d rather avoid.

Understanding what happens when you deposit an expired check isn’t just about curiosity—it’s about protecting your account from fees and avoiding awkward conversations with both your bank and whoever wrote the check.

Do Checks Actually Expire?

The short answer? Sort of.

According to the Uniform Commercial Code § 4-404, a bank is under no obligation to a customer having a checking account to pay a check, other than a certified check, which is presented more than six months after its date. But here’s where it gets interesting—that doesn’t mean your bank won’t accept the check anyway.

Personal checks are typically considered valid for six months (180 days) from the date written. After that threshold, they become “stale-dated” checks.

However, this isn’t a hard expiration like milk going bad. According to the Consumer Financial Protection Bureau, banks and credit unions may choose to honor stale checks, and different states have varying requirements around this practice.

The legal framework gives banks discretion. They can accept your eight-month-old check if they want to—or they can refuse it outright.

What Happens When You Try to Deposit a Stale Check

Real talk: the outcome isn’t predictable.

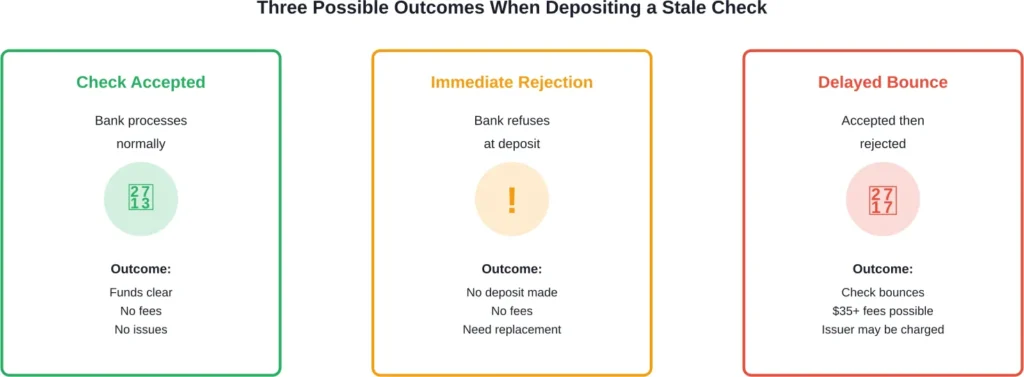

When you deposit a check that’s more than six months old, one of three things typically happens.

Scenario One: The Bank Accepts It

Sometimes banks process stale checks without blinking. Some banks have accepted checks older than six months, and various sources report successful deposits of older checks.

The check goes through normal processing. Funds appear in your account within the standard timeframe. Everything works just like a fresh check.

This happens more often than you might expect, particularly with personal checks from established accounts with sufficient funds.

Scenario Two: The Bank Rejects It Immediately

Your bank might refuse the deposit right at the counter or through mobile deposit. The teller (or the app) notices the date and declines to process it.

No harm, no foul—you just need to find another solution.

Scenario Three: The Check Bounces After Deposit

Here’s where things get expensive.

Your bank accepts the deposit initially. The check enters the clearing process. But then the paying bank (the one the check is drawn on) refuses to honor it due to the stale date.

The check bounces back. You’ll likely face a returned check fee—and these aren’t cheap. According to Bankrate, bounced check fees vary by institution. At Bank of America, the fee is $35 for returned items.

Plus, the person who originally wrote the check might get hit with a nonsufficient funds fee on their end, even though they had money in their account. That makes for an awkward conversation.

How Different Types of Checks Handle Expiration

Not all checks follow the same six-month guideline.

| Check Type | Typical Validity Period | Key Considerations |

|---|---|---|

| Personal Checks | 6 months (180 days) | Most common type; banks have discretion to accept or refuse after expiration |

| Business Checks | 6 months (180 days) | Often include “void after 90 days” or similar language printed on the check |

| Cashier’s Checks | No expiration (varies by state) | Generally don’t expire, but may be subject to unclaimed property laws after 3-5 years |

| Government Checks | 12 months | Typically valid for one year; must contact issuing agency for replacement after expiration |

| U.S. Treasury Checks | 12 months | Valid for one year from issue date; Treasury will reissue if expired |

| Money Orders | No expiration (fees may apply) | Don’t expire but may incur dormancy fees after 1-3 years depending on issuer |

Business Checks Often Have Stricter Rules

Many businesses print expiration language directly on their checks. You’ll see phrases like “void after 90 days” or “not valid after 6 months.”

These printed restrictions carry weight. Even if the standard six-month rule might give some wiggle room, explicitly stated terms make the check invalid once that period passes.

Cashier’s Checks and Money Orders

These instruments generally don’t expire in the traditional sense. But they’re not immune to complications.

After several years of inactivity, these checks may be turned over to the state as unclaimed property. The timeframe varies by state—typically between three and five years.

According to guidance from the Office of the Comptroller of the Currency, the bank must make nonlocal cashier’s checks available within five business days. However, if more than $5,000 is deposited in one day, banks may place holds on amounts exceeding that threshold.

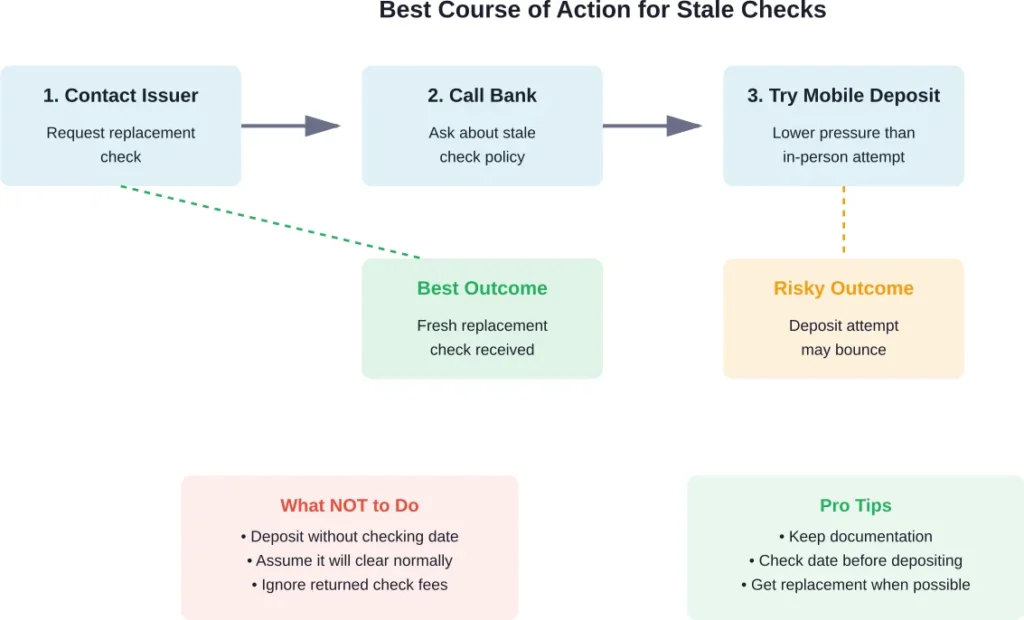

What Should You Do With a Stale Check?

Don’t just deposit it and hope for the best.

Here’s the smart approach.

Step One: Contact the Issuer

Reach out to whoever wrote the check—whether that’s a person, business, or government agency. Explain the situation and request a replacement check.

Most issuers will void the old check and send a new one without hassle. This eliminates all risk of fees or bounced deposits.

Step Two: Call Your Bank First

Before attempting any deposit, call your bank and ask about their policy on stale checks. Some banks are more flexible than others.

The representative might tell you to just try the deposit, or they might warn you it’ll definitely be rejected. Either way, you’ll know what to expect.

Step Three: Consider Mobile Deposit

If you decide to attempt the deposit anyway, mobile deposit offers a lower-pressure option than standing at a teller window.

The app might reject the check automatically when it reads the date. Or it might accept it into the queue. Either way, it’s less awkward than an in-person conversation.

Step Four: Document Everything

Keep records of your attempts to contact the issuer, any communications with your bank, and copies of the original check.

If disputes arise about whether the check was cashed or voided, documentation protects everyone involved.

Common Fees and Costs to Watch For

The financial consequences of depositing a stale check vary depending on how things play out.

If the check bounces after your bank initially accepts it, returned check fees kick in. These fees aren’t standardized across the industry.

Some institutions, like Santander Bank, don’t charge a fee for returned checks. At Bank of America, the fee is $35 for returned items.

But that’s just your side of the equation. The person who wrote the check might face nonsufficient funds fees from their bank, even though their account had plenty of money. The check wasn’t rejected due to insufficient funds—it was rejected due to the stale date.

This creates awkward situations where both parties end up paying fees through no real fault of either person.

Special Situations and Exceptions

Some scenarios create unique complications with stale checks.

Payroll Checks

Uncashed payroll checks don’t just disappear. After a certain period (usually 1-3 years depending on state law), employers must turn these funds over to the state as unclaimed property.

If you find an old payroll check, contact your former employer’s HR or payroll department. They can reissue payment and ensure you’re not dealing with unclaimed property complications.

Insurance Settlement Checks

Insurance companies often print explicit expiration dates on settlement checks—commonly 90 or 180 days. These printed terms override the standard six-month guideline.

Contact the insurance company directly for a reissued check rather than attempting to deposit an expired settlement.

Tax Refund Checks

U.S. Treasury checks, including tax refunds, are valid for one year from the issue date. After that, the Treasury won’t honor them.

The IRS will reissue expired refund checks. Contact them directly or use the “Where’s My Refund” tool to start the reissue process.

Frequently Asked Questions

Banks are not required to accept checks older than six months, though some will process them anyway. The Consumer Financial Protection Bureau notes that state laws vary and banks have discretion in these situations. The safest approach is contacting the check issuer for a replacement rather than risking rejection and potential fees.

If your bank initially accepts the deposit but the check later bounces due to the stale date, you may face returned check fees. According to Bankrate, these fees can reach $35 at institutions like Bank of America, though some banks like Santander don’t charge for returned items. Check your bank’s fee schedule for specific amounts.

Cashier’s checks generally don’t have the same six-month limitation as personal checks. However, they can become subject to state unclaimed property laws after 3-5 years of inactivity, depending on jurisdiction. The funds don’t disappear but may be turned over to the state, requiring a claim process to recover them.

Many business checks include printed language like “void after 90 days” that establishes an explicit expiration date shorter than the standard six-month period. These printed terms carry legal weight and make the check invalid after that timeframe. Contact the issuing business for a replacement check.

You can attempt mobile deposit of a stale check, and the app may either reject it automatically when scanning the date or accept it into the processing queue. Mobile deposit carries the same risks as in-person deposits—potential rejection and fees—but offers a more convenient, lower-pressure way to attempt the transaction.

Most government-issued checks, including U.S. Treasury checks and federal tax refunds, are valid for 12 months from the issue date. After expiration, you’ll need to contact the issuing agency to request a replacement check. State and local government checks may have different validity periods.

If the paying bank rejects the check due to the stale date, the person who wrote the check might be charged a nonsufficient funds fee even though money was available in their account. This creates frustration for both parties and is another reason to request a replacement check rather than attempting to deposit an expired one.

The Bottom Line on Depositing Expired Checks

Depositing a check that’s more than six months old is a gamble with outcomes ranging from perfectly fine to financially frustrating.

Banks aren’t obligated to honor stale checks, but they’re not prohibited from doing so either. That discretion means unpredictability—and unpredictability in banking usually means potential fees.

The smartest move? Contact whoever issued the check and request a replacement. It takes a phone call or email, but it eliminates all risk of bounced deposits, returned check fees, and awkward conversations about money.

Check the date on every check before depositing it. Keep track of when checks arrive. And if you do find yourself with a stale check, resist the temptation to just deposit it and hope for the best.

Your checking account balance—and your relationship with the check issuer—will thank you for taking the careful approach.