Quick Summary: Overpaying your credit card creates a negative balance, meaning the card issuer owes you money. This won’t harm your credit score or incur penalties. You can use the credit toward future purchases, request a refund (which issuers must send within seven business days of receiving your request), or wait for the issuer to automatically refund you if the negative balance persists for more than six months.

Paying credit card bills can sometimes feel like juggling—especially when you’re managing autopay, manual payments, and occasional refunds. One moment you’re staying on top of your finances, the next you’ve accidentally sent $500 when you only owed $50.

Sound familiar?

Credit card overpayment happens more often than most people realize. Whether it’s a double payment through autopay confusion, a manual error when entering the amount, or a refund that posted after you’d already paid your balance in full, the result is the same: your account shows a negative balance.

But here’s the thing—that negative number isn’t a problem. It’s actually money the credit card company owes you.

Understanding Negative Credit Card Balances

When you overpay your credit card, your account balance goes negative. If you owed $100 but paid $200, your statement will show -$100. This negative balance represents a credit on your account—essentially, the card issuer is holding your money.

According to the Consumer Financial Protection Bureau’s Regulation Z (specifically § 1026.11), when a credit balance exceeds $1, creditors have specific obligations to handle that overpayment. They can’t just keep your money indefinitely.

The negative balance won’t accrue interest because interest only applies to money you owe, not money you’re owed. You’re not borrowing anything when your balance is negative—quite the opposite.

Common Reasons for Credit Card Overpayment

Several scenarios can create a negative balance on your credit card:

- Autopay and manual payment overlap: You set up automatic payments but forgot and paid manually too

- Refunds after payment: You paid your full balance, then returned a purchase and received a refund to that card

- Incorrect payment amount: Typing errors when entering payment amounts (adding an extra zero is surprisingly common)

- Duplicate payments: Technical glitches or accidentally clicking “submit” twice

- Rewards redemptions: Statement credits from rewards posting after you’ve already paid

None of these situations will hurt your credit score or financial standing. They’re simply accounting adjustments that get resolved through one of several methods.

What Happens to Your Overpayment

When you overpay your credit card balance, you have three primary options for handling that negative balance. Understanding each helps you make the best choice for your situation.

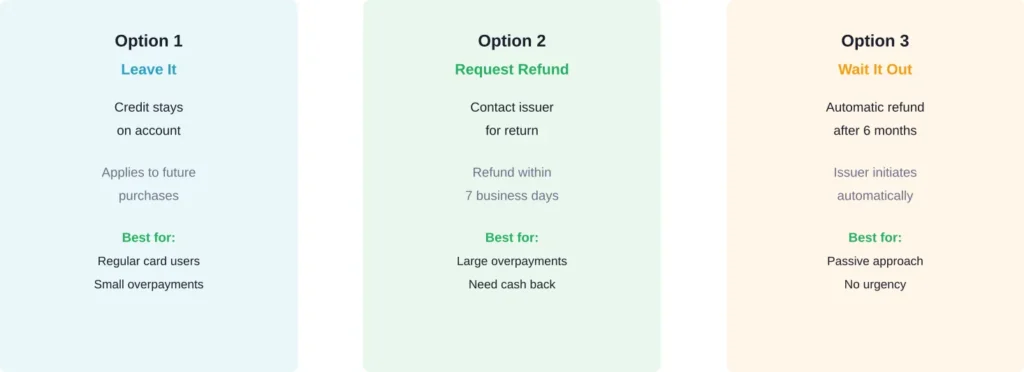

Leave the Credit on Your Account

The simplest option is doing nothing. The negative balance will automatically apply to your next purchases. If you overpaid by $50 and then spend $30 on groceries, your new balance will be -$20.

This approach works well if you regularly use the card and the overpayment amount is relatively small. The credit will naturally disappear as you make purchases.

Request a Refund From Your Issuer

Federal regulations require credit card issuers to refund overpayments upon request. According to Regulation Z § 1026.11, when you request a refund of a credit balance exceeding $1, the issuer must send the funds within seven business days of receiving your request.

Most issuers make this process straightforward. You can typically request a refund by:

- Calling the customer service number on your card

- Using the issuer’s mobile app or online account portal

- Sending a written request to the address on your statement

The refund usually arrives as a check mailed to your billing address or as a direct deposit to your linked bank account, depending on the issuer’s policies and your preferences.

Wait for Automatic Refund

If a negative balance remains on your account for more than six months, the card issuer will attempt to refund the amount automatically. Even if you don’t request it, they’re required to make a good faith effort to return your money.

That said, waiting six months isn’t ideal if you need the cash sooner. But it’s good to know the money won’t just vanish if you forget about it.

Does Overpaying Affect Your Credit Score

Here’s some good news: overpaying your credit card won’t hurt your credit score. In fact, it won’t have any negative impact on your credit profile at all.

Credit reporting agencies calculate your credit utilization ratio by dividing your total credit card balances by your total credit limits. When you have a negative balance, most issuers report your balance as $0 to the credit bureaus—not as a negative number.

Some people wonder whether overpaying could somehow boost their credit score by showing “extra” responsibility. It doesn’t work that way. A $0 balance and a negative balance are treated identically for credit scoring purposes.

| Scenario | Reported Balance | Credit Impact |

|---|---|---|

| Owe $500 on $1,000 limit | $500 | 50% utilization |

| Owe $0 on $1,000 limit | $0 | 0% utilization |

| Negative $100 on $1,000 limit | $0 | 0% utilization |

Your credit utilization will show 0% whether you paid exactly what you owed or overpaid by $100. Both scenarios are excellent for your credit score, but overpaying provides no additional benefit.

How to Avoid Credit Card Overpayment

While overpaying isn’t harmful, it does tie up your cash unnecessarily. A few simple practices can help prevent accidental overpayments.

First, review your current balance before making manual payments. Credit card balances can change daily with new purchases, refunds, and interest charges. Always check your current balance rather than relying on memory or an old statement.

Second, be cautious with autopay settings. Autopay is convenient, but it can create problems if you’re also making manual payments. If you use autopay, consider setting it to pay only the minimum due rather than the full balance, then make manual payments for the remaining amount. Alternatively, pick one method and stick with it.

Third, keep track of pending refunds. If you returned a purchase and expect a refund, wait for it to post before paying your balance in full. Otherwise, you might pay the full amount shown on your statement, then receive the refund afterward, creating a negative balance.

Finally, double-check payment amounts before submitting. It takes only a few seconds to verify you’re paying the correct amount, but fixing an overpayment takes considerably longer.

Special Situations and Considerations

Certain scenarios create unique overpayment situations worth understanding.

Refunds After Paying Your Balance

This is one of the most common ways negative balances occur. You make a purchase for $200, pay off your full statement balance including that purchase, then return the item. The $200 refund posts to your card, creating a -$200 balance.

Federal regulations treat this exactly like any other overpayment. You can request a refund, use the credit for future purchases, or wait for the automatic refund after six months.

Closing an Account With a Negative Balance

If you’re closing a credit card account that has a negative balance, the issuer must refund the amount to you. They can’t close the account and keep your money.

According to Regulation Z, the issuer must make a good faith effort to refund any remaining credit balance when an account closes. This typically happens automatically as part of the account closure process.

Large Overpayments

Accidentally overpaying by thousands of dollars—perhaps by adding extra zeros—creates more urgency than a $20 overpayment. In these cases, contact your card issuer immediately to request a refund rather than waiting for the credit to apply to future purchases.

Most issuers will expedite refunds for large overpayments, understanding that the money represents a significant amount of your available cash.

Your Rights Under Federal Law

The Federal Trade Commission and Consumer Financial Protection Bureau provide clear protections regarding credit card overpayments and credit balances.

Under Regulation Z § 1026.11, creditors must handle credit balances exceeding $1 according to specific rules. When you request a refund, the creditor has seven business days of receiving your request to send the money. If you don’t request a refund and the negative balance persists for more than six months, the creditor must attempt to refund the amount.

These regulations ensure that credit card issuers can’t simply pocket overpayments or make it difficult to recover your money. The process should be straightforward and quick.

If a card issuer refuses to refund an overpayment or makes the process unreasonably difficult, you can file a complaint with the Consumer Financial Protection Bureau through their website. The CFPB takes these complaints seriously and works to resolve disputes between consumers and financial institutions.

Frequently Asked Questions

No, you won’t lose the money. The overpayment creates a negative balance that either applies to future purchases or gets refunded to you. Federal regulations require issuers to refund overpayments upon request within seven business days of receiving your request, or automatically after six months if the negative balance remains.

Overpaying won’t improve your credit score beyond what paying your balance in full already accomplishes. Credit bureaus typically receive reports showing a $0 balance whether you paid exactly what you owed or overpaid. Both scenarios give you 0% credit utilization, which is excellent for your score.

According to Regulation Z, credit card issuers must send refunds within seven business days of receiving your request. The actual time for the money to reach your account depends on the refund method—direct deposits typically arrive faster than mailed checks.

The card issuer must refund any negative balance when closing your account. They cannot close the account and retain your overpayment. This refund typically happens automatically as part of the account closure process, though you can request it specifically to ensure prompt processing.

Technically yes, but it’s not recommended. Some people overpay their cards before making large purchases to avoid hitting their credit limit. However, this ties up your cash unnecessarily. If you need more spending power, requesting a credit limit increase is a better approach than prepaying your account.

No, negative balances don’t earn interest. The credit card company isn’t paying you to hold your money—they’re simply holding an overpayment that belongs to you. Interest only applies to balances you owe, not balances owed to you.

If an issuer refuses to refund an overpayment or makes the process unreasonably difficult, you can file a complaint with the Consumer Financial Protection Bureau. Federal regulations clearly require issuers to refund overpayments, so refusing to do so violates consumer protection rules.

Moving Forward With Confidence

Credit card overpayment might feel like a mistake, but it’s a harmless one that happens to many cardholders. The negative balance won’t hurt your credit, won’t result in penalties, and the money remains yours to use or recover.

Whether you choose to leave the credit on your account for future purchases, request an immediate refund, or simply wait for the automatic refund, you’re protected by federal regulations that ensure you get your money back.

The key is understanding your options and choosing the approach that works best for your situation. Regular card users with small overpayments might prefer letting the credit apply to upcoming purchases. Those who overpaid larger amounts or need the cash back should request a refund right away.

Most importantly, don’t stress about an overpayment. It’s one of the easiest credit card mistakes to fix, and it won’t cause any lasting problems with your account or credit standing. Just contact your issuer, decide how you want to handle the negative balance, and move on with your financial life.