Quick Summary: Failing to pay HOA fees can lead to escalating consequences including late fees, collection costs, payment plans, liens on your property, and ultimately foreclosure. Most HOAs are legally empowered to enforce payment through statutory liens that take priority over many other claims. Understanding these consequences and communicating with your HOA early can help avoid severe financial and legal outcomes.

Homeowners associations rely on regular fee payments to maintain common areas, provide services, and keep communities functioning smoothly. When residents purchase property in an HOA community, they enter a legally binding agreement to pay these assessments.

But what happens when those payments stop?

The consequences aren’t just administrative inconveniences. HOAs wield substantial legal power to collect unpaid dues, and the penalties can escalate quickly from minor annoyances to serious financial threats.

Understanding HOA Fees and Why They’re Mandatory

HOA fees fund essential community operations. These assessments cover maintenance of common areas, landscaping services, amenities like pools or clubhouses, insurance for shared structures, and administrative costs.

Here’s the thing though—these fees aren’t optional suggestions. When purchasing a home in an HOA community, buyers sign governing documents that create a contractual and legal obligation to pay assessments. This isn’t like a voluntary membership.

The association operates as a legal entity with enforcement powers granted by state law and the community’s governing documents. Refusing to pay doesn’t exempt anyone from their obligations.

The Escalating Consequences of Unpaid HOA Dues

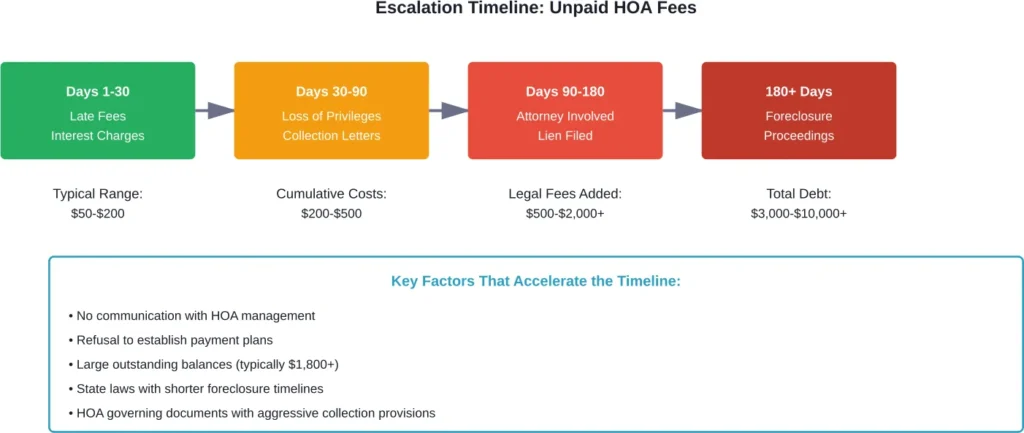

The repercussions for non-payment follow a predictable but increasingly severe pattern. Understanding this progression helps homeowners recognize how quickly minor delinquencies can become major problems.

Late Fees and Interest Charges

The first consequence appears almost immediately. Most HOAs impose late fees when payments aren’t received by the due date, typically adding a percentage of the outstanding balance or a flat fee specified in governing documents.

Interest charges may accumulate on unpaid balances according to governing documents, potentially turning a manageable debt into a growing financial burden.

Loss of Privileges and Voting Rights

Many associations suspend delinquent homeowners’ access to amenities. That community pool, fitness center, or clubhouse? Access gets revoked until accounts become current.

Voting rights often disappear too. Delinquent owners typically can’t participate in HOA elections or vote on community matters, removing their voice from governance decisions that affect their property.

Collection Efforts and Payment Plans

Once accounts reach a certain threshold—often after 30 to 90 days past due—collections begin in earnest. The HOA may offer payment plans to resolve delinquencies without legal action.

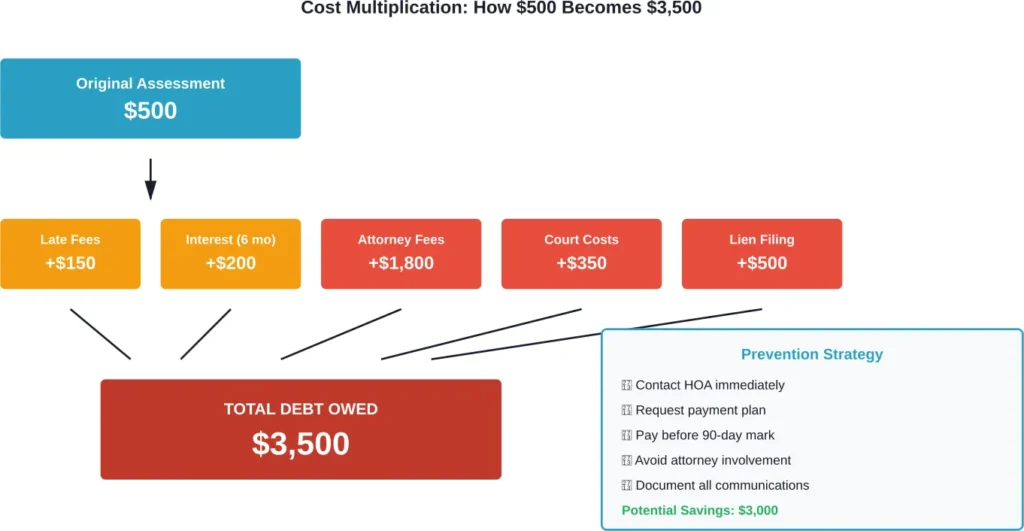

But wait. If payment arrangements fail or homeowners don’t respond, the association escalates to formal collection processes. This is where costs multiply dramatically.

Legal Actions: Liens and Foreclosure

This is where things get serious. HOAs possess powerful legal tools to collect unpaid assessments, and they’re not afraid to use them.

How HOA Liens Work

According to Washington state law (RCW 64.90.485), associations have statutory liens on units for unpaid assessments from the time those assessments become due. Similar provisions exist across most states.

These liens aren’t symbolic. They attach to the property itself, not just the owner. The lien follows the home through ownership changes and must be satisfied before clear title can transfer.

Real talk: HOA liens often take priority over other claims. While they typically rank below first mortgages and property tax liens, they can supersede second mortgages, home equity lines of credit, and other encumbrances.

The Foreclosure Process

Can an HOA actually foreclose over unpaid fees? Absolutely.

Arizona law (A.R.S. 33-1807) specifies that associations may foreclose common expense liens in the same manner as mortgage foreclosures, though only if the owner has been and remains delinquent for eighteen months or in the amount of $10,000 or more, whichever occurs first. Other states have different thresholds and timelines.

Before foreclosure proceedings begin, most states require specific notices. Washington law requires specific notices and requires the association to obtain toll-free numbers and website information from the department of commerce for inclusion in the notice. Colorado’s HB24-1233 established procedural requirements associations must follow when seeking payment of delinquent amounts.

The foreclosure process typically includes:

- Filing a formal lien against the property

- Sending required pre-foreclosure notices

- Initiating judicial or non-judicial foreclosure proceedings

- Scheduling a foreclosure sale if debts remain unpaid

- Selling the property at auction to satisfy the debt

And yes, homeowners can lose their homes over unpaid HOA fees, even if those fees amount to just a few thousand dollars.

| Consequence Type | Timeline | Typical Cost Impact | Reversibility |

|---|---|---|---|

| Late Fees | Immediate (1-15 days) | $25-$100 per month | Easy – Pay balance |

| Interest Charges | Monthly accrual | 8-18% annually | Easy – Pay balance |

| Loss of Amenities | 30-60 days | No direct cost | Easy – Pay balance |

| Attorney Fees | 60-90 days | $500-$3,000+ | Moderate – Negotiate |

| Property Lien | 90-180 days | $200-$500 filing | Moderate – Pay in full |

| Foreclosure | 180+ days (varies by state) | Loss of property | Difficult – Legal intervention |

Additional Financial Burdens

Beyond the original unpaid assessments, delinquent homeowners face mounting expenses that can quickly dwarf the initial debt.

Attorney Fees and Collection Costs

Once an HOA refers delinquent accounts to attorneys, legal fees get added to the outstanding balance. These costs aren’t trivial—they can include hourly attorney rates, court filing fees, and administrative charges.

Most governing documents allow associations to pass these collection costs directly to delinquent homeowners. Unpaid assessments can substantially increase once legal fees are factored in, potentially multiplying the original debt several times over.

Special Assessments for Community Shortfalls

Here’s something many homeowners don’t consider: when some residents don’t pay their dues, the financial burden doesn’t simply disappear. The HOA still has obligations to maintain the community and pay vendors.

If delinquencies create budget shortfalls, associations may levy special assessments on all homeowners to cover the gap. This means current-paying residents end up subsidizing their delinquent neighbors—a situation that breeds resentment and community conflict.

Impact on Credit and Future Housing

The consequences extend beyond immediate financial penalties. Unpaid HOA fees can damage credit scores when associations report delinquencies to credit bureaus or obtain judgments through court proceedings.

A lien or foreclosure on credit reports creates obstacles for future housing applications, mortgage approvals, and refinancing attempts. These marks can remain on credit reports for extended periods.

What Homeowners Can Do When Struggling to Pay

Financial hardships happen. The key is addressing the situation proactively rather than avoiding it.

Communication Is Critical

Contact HOA management immediately when payment problems arise. Most associations prefer working with homeowners to establish payment plans rather than pursuing legal action.

Many HOAs offer hardship programs, temporary payment reductions, or extended payment schedules for residents facing genuine financial difficulties.

Negotiating Payment Plans

Payment plans allow homeowners to satisfy delinquent balances over time while preventing escalation to liens or foreclosure. These arrangements typically require some upfront payment and consistent monthly installments.

The earlier homeowners engage in these discussions, the more flexibility associations typically show. Waiting until foreclosure proceedings begin drastically reduces negotiation leverage.

Understanding State-Specific Protections

Some states provide homeowner protections that limit HOA collection activities. Washington law requires specific notices and requires the association to obtain toll-free numbers and website information from the department of commerce for inclusion in the notice. Colorado’s recent legislation established procedural requirements for collection enforcement.

Research state-specific laws governing HOA collections—these can provide important safeguards and timelines that affect how quickly situations escalate.

Why HOAs Have Such Extensive Collection Powers

The enforcement authority seems heavy-handed to many homeowners. Why do HOAs wield such power?

Community associations operate as mini-governments for planned developments. They maintain infrastructure, provide services, and preserve property values. Unlike municipalities that collect property taxes, HOAs lack taxing authority.

Their only funding source is member assessments. Without effective collection mechanisms, associations couldn’t fulfill their maintenance obligations, pay insurance premiums, or fund necessary repairs.

When significant numbers of homeowners don’t pay, essential services deteriorate, property values decline, and the entire community suffers. The legal tools associations possess exist to prevent this collective harm.

Can Homeowners Avoid Paying HOA Fees?

The short answer? No.

Some homeowners believe they can simply ignore HOA obligations or refuse payment. This doesn’t work. The fees constitute legally enforceable debts backed by statutory authority.

Claiming ignorance of the HOA’s existence doesn’t provide an escape. Purchase agreements and title documents disclose HOA membership. Buyers receive governing documents before closing, creating legal acknowledgment of the obligation.

The only legitimate ways to avoid HOA fees are selling the property or ensuring the community dissolves its association—a complex process requiring supermajority owner approval that rarely succeeds.

Frequently Asked Questions

How long before an HOA can put a lien on your house? Timelines vary by state and governing documents. According to statutory law in some states, liens attach automatically when assessments become due, though recorded liens in public records typically appear after initial collection efforts.

Yes, HOAs can foreclose over unpaid assessments in most states. Arizona law permits foreclosure after eighteen months of delinquency. Other states have different thresholds, but foreclosure remains a legal option associations can pursue. Homeowners have lost properties worth hundreds of thousands of dollars over debts of just a few thousand.

HOA liens attach to the property, not the individual owner. Outstanding assessments must typically be satisfied at closing from sale proceeds. Buyers rarely accept properties with HOA liens, and title companies won’t issue clear title until debts are resolved. Some states make sellers personally liable for unpaid assessments even after sale.

Unpaid HOA fees don’t automatically appear on credit reports like mortgage or credit card delinquencies. However, when HOAs obtain court judgments or turn accounts over to collection agencies, those actions do get reported to credit bureaus. Foreclosures also appear on credit reports and severely damage credit scores.

Most HOAs can’t reduce the actual assessment amounts—those are set by budgets and applied uniformly to all owners. However, associations can offer payment plans, waive some late fees, or provide temporary hardship accommodations. The key is communicating early before accounts reach attorneys and legal fees accumulate.

Generally speaking, no exemptions exist for standard HOA assessments. All property owners in the community must pay equally based on their unit’s allocated share. Some associations offer reduced rates for specific amenities if owners opt out of using them, but basic operating assessments apply to everyone.

Perceived lack of maintenance doesn’t eliminate the legal obligation to pay assessments. Homeowners who believe the association is breaching its duties should continue paying fees while pursuing internal dispute resolution, attending board meetings, or seeking legal remedies through proper channels. Withholding payment typically violates governing documents and triggers collection actions.

Conclusion

The consequences of unpaid HOA fees escalate quickly from minor inconveniences to serious legal threats. Late fees and interest charges grow into liens, and liens can lead to foreclosure—even over relatively small debts.

But here’s what matters most: communication changes everything. HOAs prefer working with struggling homeowners rather than pursuing foreclosure. Payment plans, hardship programs, and negotiated settlements are available for residents who engage proactively.

Don’t ignore HOA payment obligations. The association’s legal powers are real, and the financial consequences compound rapidly. Reach out to HOA management at the first sign of payment difficulty. Those early conversations can prevent thousands in additional fees and protect homeownership itself.

The governing documents signed at purchase created binding obligations. Understanding those commitments and addressing payment challenges head-on provides the best path forward for homeowners in financial distress.