Quick Summary: Not paying collections debts can lead to serious consequences including lawsuits, wage garnishment, damaged credit scores, and aggressive collection attempts. However, debt collectors must follow strict federal rules under the Fair Debt Collection Practices Act, and in some states, old debts may become time-barred from legal action. Understanding your rights and responding strategically can help you navigate collections effectively.

When a debt goes unpaid long enough, creditors often sell or transfer it to a collection agency. At that point, many people wonder whether ignoring these collectors will make the problem disappear.

The short answer? No, it won’t.

But the consequences of not paying collections are more nuanced than most people realize. Federal laws protect consumers from harassment, statutes of limitations can expire on old debts, and sometimes paying a collection can actually hurt your credit score.

Here’s what actually happens when you don’t pay a debt in collections—and what you should know before deciding how to respond.

What It Means When Debt Goes to Collections

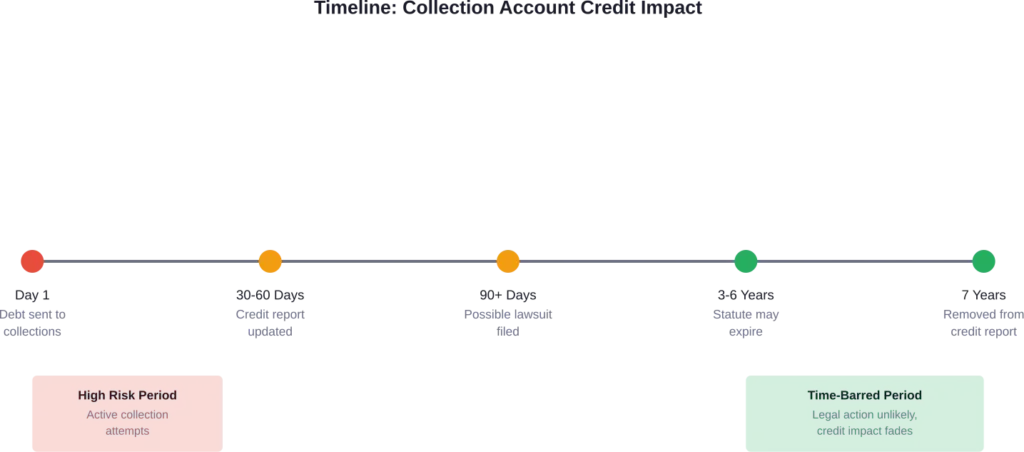

A debt typically gets sent to collections after 30 to 180 days of nonpayment, depending on the creditor. This can happen with credit cards, medical bills, personal loans, utility bills, and other consumer debts.

The original creditor either sells the debt to a third-party collection agency for a fraction of its face value, or hires an agency to collect on their behalf. According to a Federal Trade Commission case, collection agencies purchased over 2.2 million NSF checks with an estimated face value of $348 million for small fractions of those amounts.

Once in collections, the debt doesn’t just vanish. The collection agency now owns it or has been hired to recover it, and they’re motivated to get payment.

How Debt Collectors Are Allowed to Contact You

The Fair Debt Collection Practices Act (FDCPA) regulates how debt collectors can communicate with consumers. According to the FTC, debt collectors must follow specific rules about contact frequency and methods.

Under the CFPB’s Debt Collection Rule finalized in recent years, collectors can contact you through phone calls, text messages, emails, and even social media—but with limitations. Under the CFPB’s Debt Collection Rule, there are limitations on call frequency, though the specific seven-day waiting period after speaking with you is not explicitly stated in the available source material.

Collectors must provide validation of the debt, and when provided in writing or electronically (called a validation notice), they must provide certain information about the debt.

Immediate Consequences of Not Paying Collections

When you don’t respond to or pay a debt collector, several things typically happen in sequence.

Credit Report Damage

According to the Consumer Financial Protection Bureau, debt collectors can report your debt to credit reporting companies after following proper notification procedures. This collection account will appear on your credit report and can significantly damage your credit score.

Collection accounts typically remain on your credit report for seven years from the date of first delinquency. This impacts your ability to get approved for credit cards, loans, mortgages, and sometimes even employment or housing.

That said, The CFPB finalized a rule to remove medical bills from credit reports used by lenders, offering relief for those with medical debt in collections.

Continued Collection Attempts

Ignoring a debt collector won’t make them stop. According to the Consumer Financial Protection Bureau, while ignoring collectors is unlikely to make them cease contact, they may find other ways to reach you.

Collectors might contact you at work, send letters, or leave voicemails. Under the FDCPA, they generally can contact third parties only to locate you, and they cannot discuss the details of your debt with anyone except you, your spouse, or your attorney.

The harassment can feel relentless. But here’s the thing: debt collectors must follow federal rules. They can’t threaten violence, use profane language, call before 8 a.m. or after 9 p.m., or misrepresent the amount you owe.

Legal Consequences: Lawsuits and Wage Garnishment

This is where things get serious.

If you continue not paying, the collection agency may file a lawsuit against you. According to the FTC, when a debt collector sues you, it’s critical to respond—either yourself or through an attorney.

What Happens If You’re Sued

Research examining Virginia hospitals found that 50,387 lawsuits were filed by 67 hospitals for unpaid medical bills during the study period, including 33,204 warrant in debt lawsuits and 17,183 wage garnishment lawsuits.

When sued, you’ll receive court documents detailing the claim. If you ignore these documents and don’t appear in court, the collector will likely win a default judgment against you. This judgment gives them legal authority to:

- Garnish your wages (taking money directly from your paycheck)

- Place liens on your property

- Freeze or levy your bank accounts

- Add interest and court costs to the original debt

Wage garnishment limits vary by state, but federal law caps it at 25% of your disposable earnings. Some income sources, like Social Security benefits, are generally protected from garnishment.

When You Should Definitely Respond to a Lawsuit

According to the FTC’s guidance on responding to debt collection lawsuits, you should file an answer with the court by the deadline stated in the court papers. In your answer, you can dispute the debt, argue that the statute of limitations has expired, or raise other defenses.

Many collection lawsuits succeed simply because defendants don’t show up. Filing a response forces the collector to prove they own the debt and that the amount is correct—something they can’t always do.

Understanding Time-Barred Debts

Here’s something debt collectors won’t advertise: many states have statutes of limitations on debt collection.

According to the CFPB, a debt doesn’t generally expire until it’s paid, but in many states, there may be a time limit on how long creditors or debt collectors can use legal action to collect. These statutes typically range from three to six years, depending on the state and type of debt.

Once a debt becomes time-barred, collectors can still contact you about it—but they can’t successfully sue you in court. The statute of limitations is an affirmative defense you can raise if sued.

The Trap of Restarting the Clock

As the FTC warns in their guidance on time-barred debts, making a payment or even acknowledging the debt in writing can restart the statute of limitations in some states. This resets the clock, giving collectors renewed legal power to sue you.

This is why understanding whether a debt is time-barred before you respond or pay is critical.

| Debt Age | Legal Risk | Credit Impact | Recommended Action |

|---|---|---|---|

| Under 3 years | High lawsuit risk | Severe damage | Negotiate or pay if possible |

| 3-6 years | Moderate risk (depends on state) | Ongoing damage | Verify statute of limitations |

| 6+ years | Low lawsuit risk (likely time-barred) | Impact decreasing | Consider waiting for removal |

| 7+ years | Very low risk | Removed from credit report | Verify removal, don’t restart clock |

Your Rights Under the Fair Debt Collection Practices Act

The FDCPA provides significant protections for consumers dealing with debt collectors.

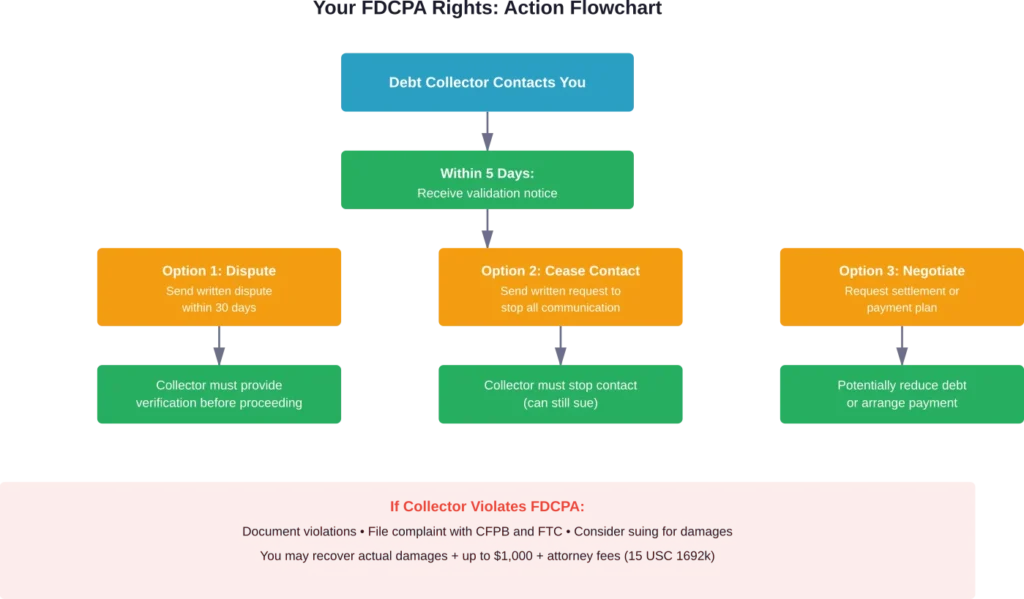

According to the Federal Trade Commission’s overview of the FDCPA, debt collectors who violate the law can be held liable for damages. Under the FDCPA (15 USC 1692k), you can sue a debt collector for actual damages sustained by the violation, plus statutory damages, and attorney’s fees.

What Debt Collectors Cannot Do

The FDCPA prohibits debt collectors from:

- Calling you repeatedly to harass or annoy you

- Using threatening, profane, or abusive language

- Falsely claiming to be attorneys or government representatives

- Threatening arrest or legal action they don’t intend to take

- Contacting you at work after you’ve told them your employer prohibits such calls

- Discussing your debt with friends, family, neighbors, or coworkers

- Misrepresenting the amount you owe

You have the right to request that a debt collector stop contacting you entirely. Send a written “cease contact” letter, and they must stop—though they can still sue you.

Verifying the Debt

Within five days of first contacting you, collectors must send a written validation notice explaining the debt amount, the creditor’s name, and your right to dispute the debt. If you dispute the debt in writing within 30 days, the collector must obtain verification before continuing collection efforts.

This is a powerful protection. Many collection agencies can’t actually prove they own the debt or that the amount is accurate.

Should You Pay a Collection Agency?

This is the million-dollar question, and the answer isn’t always straightforward.

Paying a collection might seem like the responsible thing to do—and sometimes it is. But other times, paying can actually make your situation worse.

When Paying Makes Sense

Consider paying if:

- The debt is recent (under three years) and within the statute of limitations

- You need to improve your credit score for an upcoming major purchase

- The collector offers a significant settlement (pay-for-delete agreements are rare but possible)

- You’re being sued or threatened with imminent legal action

- The debt is legitimate and you have the financial means to pay

Negotiate before paying. Collection agencies may accept settlements for less than the full amount in some cases. Get any agreement in writing before sending payment.

When Paying Might Hurt You

Avoid paying if:

- The debt is time-barred (check your state’s statute of limitations first)

- You’re close to the seven-year credit reporting period ending

- The collector can’t verify the debt or prove they own it

- Paying would restart the statute of limitations in your state

- The collection is for medical debt (as of 2026, these won’t appear on credit reports used by lenders)

Real talk: paying an old collection won’t remove it from your credit report unless the collector specifically agrees to a pay-for-delete arrangement. Credit impact of paid collections versus unpaid collections may vary depending on the credit scoring model used.

Alternative Options to Consider

Not paying collections doesn’t mean doing nothing. Several strategic alternatives exist.

Debt Validation and Disputes

Request debt validation within 30 days of first contact. Many collection agencies can’t actually prove the debt is valid or that they own it. Without proper documentation, they can’t legally collect.

Common grounds for disputing include incorrect amounts, debts already paid, identity theft, or debts outside the statute of limitations.

Bankruptcy Protection

For overwhelming debt, bankruptcy might be the best option. Chapter 7 bankruptcy can discharge many unsecured debts entirely, including most collections. Chapter 13 creates a manageable payment plan.

According to the FTC’s guidance on getting out of debt, bankruptcy has serious long-term consequences for your credit, but it also provides a fresh start and immediate protection from collection efforts through an automatic stay.

Federal student loans and certain other debts generally can’t be discharged in bankruptcy, as noted by the CFPB.

Credit Counseling and Debt Management Plans

Nonprofit credit counseling agencies can help you create a debt management plan, negotiate with collectors, and consolidate payments. The FTC advises looking for legitimate counseling services—avoid companies that charge high upfront fees or promise unrealistic results.

How to Report Illegal Collection Practices

If a debt collector violates the FDCPA, you have recourse.

According to the FTC, you can file a complaint with both the Federal Trade Commission and the Consumer Financial Protection Bureau. You can also sue the collector in state or federal court within one year of the violation.

Document everything: save voicemails, record call dates and times, keep letters and emails, and note any violations. This evidence is crucial if you decide to take legal action.

Frequently Asked Questions

Not without a court judgment. If a collector sues you and wins a judgment, they can then seek a bank levy to freeze and withdraw funds from your account. However, certain funds like Social Security benefits are typically protected from garnishment. They cannot access your account without first going through the legal process.

No. According to the CFPB, a debt doesn’t generally expire or disappear until it’s paid. However, the statute of limitations for legal action varies by state (typically three to six years), and the debt will be removed from your credit report after seven years from the date of first delinquency. Ignoring collectors won’t stop them from contacting you or potentially suing you.

Debt collectors can contact third parties only to obtain your contact information, and they generally can’t contact the same person more than once. They cannot discuss the details of your debt with anyone except you, your spouse, or your attorney. If you tell a collector your employer prohibits such calls, they must stop contacting you at work.

Paying an old collection won’t extend how long it stays on your credit report—it will still be removed seven years from the original delinquency date. However, in some states, making a payment can restart the statute of limitations for lawsuits. Before paying an old debt, verify whether it’s time-barred and consider whether paying provides any actual benefit.

Yes. Collection agencies often purchase debts for pennies on the dollar, so they’re frequently willing to settle for 30-60% of the balance. Always negotiate settlements in writing before paying, and try to get a pay-for-delete agreement where the collector agrees to remove the collection from your credit report once paid. Never give collectors direct access to your bank account.

This depends on your state’s statute of limitations for the type of debt involved, typically ranging from three to six years. After this period expires, the debt becomes time-barred, meaning collectors can’t successfully sue you in court. However, they can still attempt to collect the debt, and it can remain on your credit report for seven years from first delinquency.

According to the FTC, you must respond by the deadline stated in the court papers, either yourself or through an attorney. File an answer with the court raising any defenses, such as the statute of limitations has expired, the debt isn’t yours, the amount is incorrect, or the collector can’t prove they own the debt. Never ignore a lawsuit—doing so will result in a default judgment against you, allowing wage garnishment and bank levies.

Taking Control of Your Collection Situation

Not paying a debt in collections carries real consequences. Credit damage, persistent contact attempts, lawsuits, and wage garnishment are all possibilities.

But understanding your rights under the FDCPA changes the dynamic. You’re not powerless. Debt collectors must follow strict federal rules, and violations can result in them owing you money. Time-barred debts lose their legal teeth. Debt validation requests force collectors to prove their claims.

The best approach depends on your specific situation: the debt’s age, the statute of limitations in your state, your financial circumstances, and your short-term credit needs. Sometimes paying or settling makes sense. Other times, strategic inaction is the smarter move.

What matters most is making an informed decision rather than reacting out of fear or simply hoping the problem disappears. It won’t—but with the right strategy and knowledge of your rights, you can navigate collections effectively and minimize the damage to your financial future.

If you’re facing collection attempts, document everything, know your rights, and consider consulting with a consumer rights attorney or nonprofit credit counselor to explore your best options.