Quick Summary: If your car is stolen while you still owe money, you must report it to police and your insurance company immediately. Standard auto insurance only pays the vehicle’s current value, which may be less than your loan balance. You remain legally obligated to continue loan payments until the insurance claim settles, and without GAP insurance, you could owe thousands on a car you no longer have.

Getting behind the wheel each morning feels routine until one morning there’s no car to get behind. More than 850,000 vehicles were stolen in the United States in 2024, and when that stolen car still carries a loan balance, the financial nightmare multiplies fast.

Here’s the thing though—most people assume their insurance will simply pay off the loan and everyone moves on. That’s not how it works.

The stolen car creates a financial gap that can leave responsible borrowers paying for a vehicle sitting in some chop shop or already stripped for parts. Understanding what happens next determines whether this becomes a manageable crisis or a years-long financial burden.

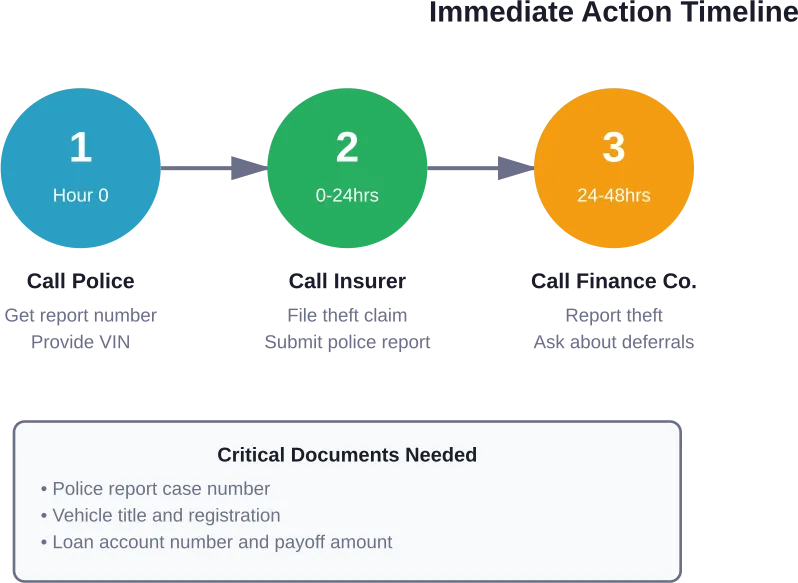

The Immediate Reality: Three Critical Calls

When a financed vehicle disappears, the clock starts ticking on multiple fronts. The order of these calls matters more than most people realize.

Report to Police First

Contact local law enforcement immediately. According to the National Highway Traffic Safety Administration, one vehicle is stolen every 31 seconds in the United States (based on 2023 data of more than 1 million vehicles stolen annually). Police need the license plate number, make, model, color, and Vehicle Identification Number (VIN).

That police report becomes the foundation for everything that follows. Insurance companies won’t process theft claims without it. Finance companies need the case number to pause collection efforts. No report means no claim, full stop.

Real talk: some stolen vehicles get recovered within 48 hours. But others never resurface.

Notify the Insurance Company

The insurer needs notification within 24 hours in most policies. Delays can complicate or invalidate claims entirely.

Comprehensive coverage is what pays for theft—liability-only policies provide zero protection. That’s a critical distinction many borrowers discover too late. Standard auto insurance only pays an amount up to the vehicle’s actual cash value, not the loan balance.

The insurance company will request the police report number, VIN, any identifying characteristics, and documentation of the loan balance.

Contact the Finance Company

The lender or leasing company must know their collateral vanished. Most finance agreements require immediate notification of theft.

This call doesn’t stop payment obligations, but it creates a paper trail. Some lenders offer temporary payment deferrals while claims process. Others don’t.

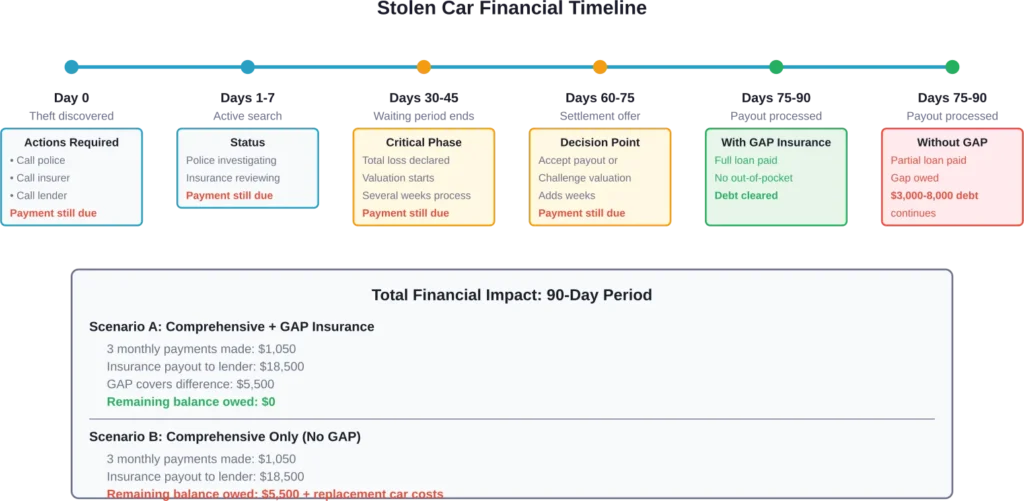

The Payment Obligation Doesn’t Stop

This shocks people most: loan payments continue even when the car is gone.

The finance agreement creates a legal obligation independent of whether the collateral still exists. Until the insurance claim settles and the lender receives payment, monthly installments remain due.

Miss those payments and the consequences stack up fast. Late fees accumulate. Credit scores drop. Collection calls start. The fact that someone stole the car doesn’t change the contract terms.

Some lenders offer forbearance or payment deferrals during active theft claims, but that’s a courtesy, not a requirement. According to the Federal Trade Commission’s guidance on auto loans, borrowers should contact lenders immediately if payment difficulties arise.

But wait—there’s more financial pain coming.

How Insurance Payouts Actually Work

Insurance companies don’t pay loan balances. They pay actual cash value.

That distinction matters enormously. Actual cash value represents what the vehicle was worth immediately before theft—accounting for depreciation, mileage, condition, and market factors.

The Depreciation Reality

New cars typically lose significant value through depreciation immediately after purchase and continue depreciating annually.

That two-year-old sedan with a $22,000 loan balance might only carry an $16,000 actual cash value. The insurance company pays $16,000. The borrower still owes $6,000 on a car they’ll never drive again.

This scenario—called negative equity or being “upside down”—is shockingly common with financed vehicles.

The Valuation Process

Insurance adjusters determine actual cash value using comparable vehicle sales, dealer quotes, and valuation databases. The valuation process typically takes several weeks after the waiting period expires.

Many insurance policies include a waiting period before declaring a stolen vehicle a total loss. This gives law enforcement time to potentially recover the car.

During that waiting period? Loan payments continue.

| Scenario Component | Amount | Who Pays |

|---|---|---|

| Outstanding loan balance | $24,000 | Borrower owes |

| Insurance actual cash value payout | $18,500 | Insurance pays lender |

| Negative equity gap | $5,500 | Borrower pays out-of-pocket |

| Deductible (if applicable) | $500 | Borrower pays |

| Total borrower pays | $6,000 | On car they don’t have |

GAP Insurance: The Financial Safety Net

Guaranteed Asset Protection insurance exists specifically for this nightmare scenario.

According to the Consumer Financial Protection Bureau, GAP is an optional product that covers the difference between the amount owed on an auto loan and the amount the insurance company pays if the car is stolen or totaled.

Standard auto insurance only pays an amount up to the vehicle’s value. GAP covers the loss when the loan balance exceeds that value.

How GAP Works in Theft Situations

When comprehensive insurance pays $18,500 on a vehicle with a $24,000 loan balance, GAP insurance covers the $5,500 difference. The borrower walks away owing nothing.

GAP insurance pricing varies and should be compared across providers before purchase. That investment prevents owing thousands on a stolen vehicle.

The Insurance Information Institute defines GAP as coverage for the difference between a car’s actual cash value when it’s stolen or wrecked and the amount the consumer owes the leasing or finance company.

Not everyone needs it though.

Who Should Consider GAP Coverage

GAP makes sense when:

- The down payment was less than 20%

- The loan term extends beyond 60 months

- The vehicle depreciates faster than average

- The loan includes rolled-in negative equity from a trade-in

- Leasing rather than buying

According to the Consumer Financial Protection Bureau, lenders and dealers cannot require GAP insurance purchase. In most situations, it’s optional.

What Happens If the Car Is Recovered

Some stolen vehicles resurface before insurance settles the claim. Now what?

The insurance company stops the theft claim process. But the condition of the recovered vehicle determines what happens next.

Recovered Intact

If police recover the car within days and it’s undamaged, the owner typically gets it back. Insurance might cover any damage from the theft—broken windows, damaged ignition, missing property.

Loan payments that continued during the theft? Those just preserved the account in good standing. No refunds there.

Recovered but Damaged

When recovered vehicles have significant damage, insurance treats it like any collision claim. Repair costs get assessed against the vehicle’s value.

When repair costs become excessive relative to vehicle value, insurers may declare a vehicle a total loss. Then it gets handled like the theft claim—actual cash value payout, potential negative equity gap, and all the same financial headaches.

The borrower can sometimes buy back the salvage and repair it, but that creates title complications and future resale problems.

Challenging Insurance Valuations

Insurance adjusters don’t always get valuations right the first time.

When the offered payout seems low, borrowers can challenge it. This requires documentation—recent comparable sales, dealer quotes for similar vehicles, evidence of recent upgrades or exceptional condition.

The process adds weeks to claim resolution, but it can increase payouts by hundreds or thousands of dollars. That matters enormously when negative equity lurks.

Some tips for stronger negotiations:

- Gather sale listings for identical make, model, year, and mileage within 50 miles

- Document any recent major repairs or upgrades with receipts

- Get independent appraisals from dealerships

- Review the adjuster’s comparable vehicles for accuracy

- Point out regional market differences that affect value

Persistence pays. Literally.

The No-Insurance Catastrophe

What about drivers without comprehensive coverage when theft strikes?

It’s financially devastating. No insurance payout means the full loan balance remains due. The borrower must continue payments on a stolen car while simultaneously securing replacement transportation.

That might mean paying $400 monthly on the stolen car’s loan while paying another $350 for a replacement vehicle. Add rental car costs when replacing a stolen vehicle, and the costs spiral impossibly fast.

According to community discussions, some lenders will negotiate settlement amounts in these situations, but they’re under no obligation to accept less than the full balance.

Credit union financing may offer competitive rates; borrowers should compare options across multiple lenders. But the financial hole remains deep.

Legal Obligations Without Insurance

The loan contract doesn’t dissolve because the collateral disappeared. Default triggers collections, credit damage, possible lawsuits, and wage garnishment.

Some borrowers assume bankruptcy offers escape, but auto loans can survive bankruptcy proceedings depending on the chapter filed and whether the lender objects.

Prevention beats cure here by a mile.

Additional Administrative Steps

Beyond the financial mess, stolen financed vehicles create paperwork obligations.

DVLA Notification

Vehicle registration authorities must know about the theft. This prevents the registered owner from liability if the stolen car gets used in crimes.

It also stops toll violations, parking tickets, and other citations from accumulating against the owner.

Tax and Registration Refunds

Some jurisdictions offer partial refunds on vehicle taxes and registration fees when theft occurs. The police report and insurance claim documentation typically qualify for these refunds.

The amounts seem small—maybe $50-200—but every dollar counts when paying off a car you’ll never see again.

Prevention Strategies That Actually Work

Stopping theft before it happens beats dealing with the aftermath.

The National Highway Traffic Safety Administration recommends multiple prevention layers:

- Always lock doors and take keys, even for quick stops

- Park in well-lit, high-traffic areas

- Never leave the car running unattended

- Install steering wheel locks or brake pedal locks

- Use car alarms and visible theft deterrent devices

- Consider GPS tracking systems for vehicle recovery

- Engrave VIN on major components to deter parts thieves

Modern cars with push-button starts face unique risks from relay attacks and signal amplification. Storing key fobs in signal-blocking pouches prevents these high-tech thefts.

Sound familiar? These basic steps stop most opportunistic thefts.

Getting Back on the Road

Once the insurance settles, securing replacement transportation becomes urgent.

Credit union financing may offer competitive rates; borrowers should compare options across multiple lenders. Shopping multiple lenders before visiting dealers strengthens negotiating position.

The theft claim and loan payoff should appear on credit reports as satisfied accounts, not defaults—assuming payments continued throughout. That maintains credit scores for replacement financing.

But buyers still nursing negative equity from the stolen car face tough decisions. Rolling that debt into new financing creates the exact same vulnerability all over again.

Frequently Asked Questions

Yes. The loan obligation continues until the insurance claim settles and the lender receives payment. Missing payments during the claim process damages credit and triggers late fees regardless of the theft.

No. Standard comprehensive coverage pays only the vehicle’s actual cash value at the time of theft, which accounts for depreciation. This amount often falls below the loan balance, especially with newer vehicles or long-term loans.

According to the Consumer Financial Protection Bureau, GAP insurance covers the difference between what insurance pays (actual cash value) and what you owe on the loan. It’s optional but valuable when the down payment was small, the loan term exceeds 60 months, or the vehicle depreciates quickly.

Many insurance policies include a waiting period before declaring a stolen vehicle a total loss, giving police time for potential recovery. After that, the valuation and settlement process typically takes several weeks. Total timeline runs 60-75 days from theft to payout.

When insurance has already settled the claim and paid the lender, the insurance company takes ownership of the recovered vehicle. The borrower cannot reclaim it. If the car is recovered before the claim settles, the owner typically gets it back, with insurance covering any theft-related damage.

No. The loan payments made before theft were required under the contract and aren’t refundable. Those payments simply maintained the account in good standing and reduced the principal balance that insurance or GAP coverage must satisfy.

Contact the lender immediately to explain the situation. The full loan balance remains due, and default consequences include collections, credit damage, and potential legal action. Some lenders negotiate reduced settlements, but they’re not obligated to. Securing replacement transportation while continuing payments on the stolen vehicle creates severe financial strain.

The Bottom Line: Protection Before Crisis

Vehicle theft with an outstanding loan creates a perfect financial storm. Standard insurance doesn’t cover the full loan balance. Payments continue on a car that’s gone. Negative equity can stretch into thousands of dollars.

GAP insurance exists specifically to prevent this scenario. The relatively small upfront cost protects against potentially catastrophic loss when theft strikes a financed vehicle.

But prevention beats insurance claims. Basic security measures—locked doors, visible deterrents, smart parking choices—stop most opportunistic thefts before they happen.

The three-step response—police, insurance, lender—must happen immediately when theft occurs. Delays complicate claims and jeopardize coverage.

Look, nobody expects their car to get stolen. But expecting it enough to buy comprehensive coverage and GAP insurance makes the difference between a manageable crisis and years of debt on a vehicle you’ll never drive again.

Review insurance coverage today. Verify comprehensive protection. Consider GAP if negative equity exists. Because discovering coverage gaps after theft is roughly 60 days too late.