Quick Summary: If you stop paying credit cards, your account becomes delinquent after 30 days, triggering late fees up to $41, penalty APRs as high as 29.99%, and immediate credit score damage. After 180 days of non-payment, the account is typically charged off and sent to collections, where debt collectors may contact you or pursue legal action, though you cannot be arrested for unpaid credit card debt alone.

Americans currently carry $1.18 trillion in credit card debt according to recent Household Debt and Credit reports. With interest rates climbing and economic pressures mounting, many people face a harsh reality: they can’t afford their credit card payments.

But what actually happens if you stop paying? The consequences are serious and far-reaching.

This isn’t a theoretical problem. Credit card delinquency rates have climbed significantly, reaching levels not seen since the Great Financial Crisis. Understanding the timeline and repercussions of non-payment helps borrowers make informed decisions rather than simply avoiding the problem.

The First 30 Days: Delinquency Begins

The moment a payment is missed, the clock starts ticking. Most credit card issuers provide a grace period of a few days, but once the payment due date passes without payment, the account is technically late.

Here’s what kicks in during that first month.

Late Fees Hit Immediately

Late fees are one of the first consequences. According to the Consumer Financial Protection Bureau, credit card companies collect approximately $12 billion each year from penalty fees, with late fees representing a significant portion.

The fee structure works like this: an initial late payment may cost up to $30. If another payment is missed within six billing cycles, subsequent late fees can reach up to $41. Some cards don’t charge late fees or waive the first occurrence, but that’s becoming less common.

These fees compound the existing debt. If someone already can’t afford the minimum payment, adding $30-41 to the balance makes the situation worse.

Promotional APRs Vanish

Many credit cards offer promotional 0% APR periods on purchases or balance transfers. Missing a payment typically triggers the immediate cancellation of these promotional rates.

That 0% rate? Gone. Replaced with the standard purchase APR, which often hovers between 18-25%. In some cases, the card issuer implements a penalty APR.

Penalty APR Takes Effect

Penalty APRs can reach 29.99% or higher. This rate applies not just to new purchases but often to the existing balance as well.

Think about the math: a $5,000 balance at 29.99% APR could generate substantial interest annually if only minimum payments are made. The debt spiral accelerates dramatically.

Days 30-60: Credit Score Damage Begins

Once an account is 30 days past due, credit card companies typically report the delinquency to the three major credit bureaus: Equifax, Experian, and TransUnion.

This is where credit score damage becomes real and lasting.

How Credit Reporting Works

Payment history accounts for roughly 35% of a FICO credit score—the largest single factor. A single 30-day late payment typically drops credit scores significantly, with estimates ranging from 60-110 points depending on starting score.

The impact varies based on the starting score. Someone with an 800 credit score will see a larger point drop than someone at 650, but the percentage damage is often more severe for those with already-compromised credit.

Late payments remain on credit reports for seven years from the original delinquency date, though their impact diminishes over time.

Compounding Effects

Credit score damage doesn’t exist in isolation. It affects:

- Interest rates on future loans and credit cards

- Auto insurance premiums in many states

- Rental applications and security deposits

- Employment opportunities for positions requiring credit checks

- Cell phone contracts and utility deposits

The ripple effects extend far beyond the credit card itself.

Days 60-180: Escalating Collection Efforts

As the delinquency period extends, credit card companies intensify collection efforts. Expect frequent phone calls, emails, and letters.

Under the Fair Debt Collection Practices Act (FDCPA) enforced by the CFPB, debt collectors are bound by specific regulations. Understanding these protections is essential.

What Debt Collectors Can Do

Debt collectors are allowed to contact borrowers by phone, mail, email, or text message. They can contact friends, family, or employers—but only to obtain contact information for the debtor, not to discuss the debt itself.

They can pursue payment through negotiation and, eventually, legal action.

What Debt Collectors Cannot Do

Under the Fair Debt Collection Practices Act (FDCPA) enforced by the CFPB, debt collectors are prohibited from:

- Threatening arrest or criminal prosecution for unpaid debt

- Using obscene or profane language

- Calling repeatedly to harass or annoy

- Calling before 8 a.m. or after 9 p.m.

- Falsely representing themselves as attorneys or government officials

- Threatening to seize property or wages without legal authority

Real talk: You cannot be arrested simply for not paying credit card debt. Debt is a civil matter, not a criminal one. However, if a creditor sues and obtains a court judgment, ignoring court orders could lead to contempt charges in some jurisdictions.

After 180 Days: Charge-Off and Collections

At roughly 180 days (six months) of non-payment, credit card companies typically charge off the account. This is a significant milestone—and not in a good way.

What “Charge-Off” Actually Means

A charge-off doesn’t mean the debt disappears. It’s an accounting term indicating the creditor has given up hope of collecting and has written off the debt as a loss for tax and regulatory purposes.

The debt still exists. The borrower still legally owes it.

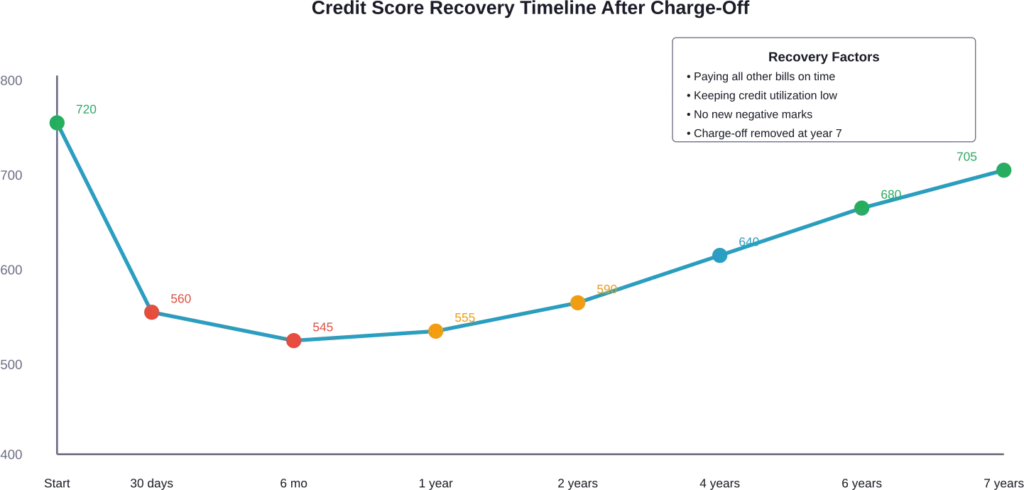

The charge-off appears on credit reports as a severely negative mark, remaining for seven years from the date of first delinquency. It devastates credit scores—often more than bankruptcy in some scoring models.

Debt Sale to Collection Agencies

After charging off an account, credit card companies often sell the debt to third-party collection agencies for pennies on the dollar. The collection agency then attempts to recover whatever it can, hoping to profit from the purchase.

This changes the dynamic. The original creditor is out of the picture. Now dealings are with debt collectors who may be more aggressive—though still bound by the FDCPA.

Legal Consequences: Lawsuits and Judgments

Debt collectors or creditors can file lawsuits to collect unpaid credit card debt. This is where the situation moves from financial inconvenience to potential legal jeopardy.

The Lawsuit Process

When sued for credit card debt, borrowers receive a summons and complaint. Ignoring this is the worst possible response.

Failing to respond or appear in court typically results in a default judgment in favor of the creditor. With a judgment, creditors can pursue:

- Wage garnishment (amounts vary by state law)

- Bank account levies

- Property liens

State laws vary significantly on what can be garnished and what’s protected.

Statute of Limitations

Credit card debt has a statute of limitations—the time period during which creditors can sue. This varies significantly by state.

Once the statute expires, the debt becomes “time-barred.” Collectors can still attempt collection, but they cannot sue successfully. However, making a payment or even acknowledging the debt in writing can restart the clock in some states.

Can You Go to Jail for Credit Card Debt?

The short answer? No.

According to the Consumer Financial Protection Bureau, debt collectors cannot have someone arrested or threaten arrest for unpaid credit card debt. The United States abolished debtors’ prisons in the 1830s.

But wait. There’s a critical exception.

If a creditor sues, wins a judgment, and the court orders the debtor to appear for a debtor’s examination or other court proceeding, failing to comply with that court order could result in contempt of court charges—which can lead to arrest.

The arrest isn’t for the debt itself, but for disobeying a court order. This distinction matters legally, even if the practical effect feels the same.

Your Options When You Can’t Pay

Stopping payment shouldn’t be the first move. Several alternatives can minimize damage or provide legitimate relief.

Contact Your Credit Card Company

Many issuers offer hardship programs for customers experiencing financial difficulties. These might include:

- Reduced minimum payments

- Lower interest rates temporarily

- Waived fees

- Payment deferrals

Card companies would rather recover some payment than deal with charge-offs and collection costs. It’s worth asking.

Credit Counseling

Nonprofit credit counseling agencies provide free or low-cost assistance. They can help create budgets, negotiate with creditors, and set up debt management plans.

A debt management plan consolidates multiple credit card payments into a single monthly payment to the counseling agency, which then distributes funds to creditors. These plans often secure reduced interest rates and fee waivers.

Debt Settlement

Debt settlement companies negotiate with creditors to accept less than the full balance owed. According to the Federal Trade Commission, this approach carries significant risks.

Settlement companies typically advise clients to stop paying creditors entirely while building up funds in a settlement account. This tanks credit scores and invites lawsuits.

Fees for these services can be substantial—often 15-25% of the enrolled debt. Additionally, forgiven debt may be reported to the IRS as taxable income. The Consumer Financial Protection Bureau notes that servicemembers have additional protections under the Servicemembers Civil Relief Act.

Balance Transfer Cards

For those with decent credit still intact, transferring high-interest balances to a 0% APR promotional card can provide breathing room. However, balance transfer fees typically run 3-5% of the transferred amount.

This strategy only works if the underlying spending problem is addressed. Otherwise, it’s just shuffling debt around.

Bankruptcy

Bankruptcy is the nuclear option, but it exists for a reason. Two primary types apply to individuals:

Chapter 7 bankruptcy liquidates non-exempt assets to pay creditors and discharges remaining eligible debts, including credit cards. It remains on credit reports for ten years but provides a genuine fresh start.

According to the U.S. Courts, debtors must pass a means test comparing current monthly income to state median income levels to qualify.

Chapter 13 bankruptcy allows debtors to develop a repayment plan over three to five years while keeping property. It’s designed for individuals with regular income who want to catch up on debts while protecting assets like homes or cars.

Both chapters include an automatic stay that halts collection actions immediately upon filing.

| Option | Credit Impact | Cost | Time to Complete | Best For |

|---|---|---|---|---|

| Hardship Program | Minimal | None | Varies | Temporary financial setback |

| Credit Counseling | Moderate | Low fees | 3-5 years | Multiple high-interest debts |

| Debt Settlement | Severe | 15-25% of debt | 2-4 years | Those facing default anyway |

| Chapter 7 Bankruptcy | Very severe (10 years) | $300-400 filing + attorney | 4-6 months | Overwhelming debt, few assets |

| Chapter 13 Bankruptcy | Severe (7 years) | $300-400 filing + attorney | 3-5 years | Regular income, protecting assets |

The Long-Term Credit Impact

Credit damage from unpaid credit cards extends years into the future. Research from West Virginia University examining credit card behaviors shows that credit card spending and borrowing patterns tend to persist over decades.

A charge-off remains on credit reports for seven years from the date of first delinquency. During that time:

- Mortgage applications become difficult or impossible

- Auto loans carry significantly higher interest rates

- New credit card approvals are unlikely

- Employment in financial services may be blocked

Recovery is possible but requires years of rebuilding through secured cards, timely payments on remaining obligations, and patience.

What About the Debt After All This?

Here’s what people often misunderstand: even after charge-off, even after the statute of limitations expires, the debt technically still exists until it’s paid, settled, discharged in bankruptcy, or the creditor abandons collection efforts.

Charge-off and statute expiration don’t erase the debt. They limit what creditors can do about it.

Some debts are eventually abandoned by collectors who determine they’re uncollectible. Others persist for years through repeated sales to different collection agencies.

Protecting Yourself From Collection Scams

The debt collection industry attracts scammers. According to the FTC, common scams include:

- Phantom debt collectors claiming you owe debts that don’t exist

- Collectors demanding payment via gift cards or wire transfers

- Threats of immediate arrest or legal action

- Refusal to provide debt validation when requested

Always request debt validation in writing within 30 days of first contact. Legitimate collectors must provide proof of the debt, the original creditor, and the amount owed.

Frequently Asked Questions

Credit card companies can file lawsuits at any time after default, but most wait until accounts are several months delinquent, often around 90-180 days. Some never sue at all, opting instead to sell the debt to collection agencies. The decision depends on the debt amount, state laws, and the creditor’s internal policies.

Defaulting on one credit card doesn’t directly affect accounts with other creditors—unless those creditors monitor your credit report. Many issuers include “universal default” clauses allowing them to raise interest rates if they detect credit problems elsewhere. Additionally, credit score damage from one default makes approval for new credit more difficult across the board.

Yes, through debt settlement, some portion of credit card debt can be forgiven. However, according to the Consumer Financial Protection Bureau, forgiven debt may be reported to the IRS as taxable income. Settlement also severely damages credit scores and doesn’t guarantee all creditors will agree to reduced payments.

Most credit card issuers in the U.S. require minimum payments of approximately 1% of the principal balance plus interest and fees. According to research from the Brookings Institution, this low minimum payment structure may extend debt repayment periods significantly, as payments barely cover interest charges on large balances.

A charge-off is an accounting action where the original creditor writes off the debt as a loss after roughly 180 days of non-payment. The account then typically goes to collections, where either the original creditor’s internal collection department or a third-party agency attempts recovery. Both appear on credit reports as separate negative marks, compounding the damage.

Absolutely. Credit card issuers often prefer negotiating directly rather than pursuing costly legal action or selling debt at a loss. Many offer hardship programs with reduced payments, lowered interest rates, or temporary forbearance. Contact the issuer as soon as financial difficulty arises—before default—for the best negotiation leverage.

Authorized users typically aren’t legally responsible for debt incurred by the primary cardholder. However, the account’s delinquent status will appear on the authorized user’s credit report, damaging their credit score. Authorized users should remove themselves from the account immediately if the primary cardholder begins missing payments.

The Bottom Line

Stopping credit card payments triggers a predictable cascade of consequences: late fees within days, credit score damage within weeks, charge-offs within months, and potential lawsuits within a year or two.

But these outcomes aren’t inevitable if action is taken early.

Communication with creditors, exploration of hardship programs, consultation with nonprofit credit counselors, and understanding legal protections under the Fair Debt Collection Practices Act can all mitigate damage and create paths forward.

The worst approach? Ignoring the problem entirely. Debt doesn’t disappear through avoidance. It compounds, both financially through accumulating fees and interest, and psychologically through stress and anxiety.

If credit card debt feels overwhelming, reach out to a nonprofit credit counseling agency for a free consultation. Nonprofit credit counseling agencies accredited by organizations like the National Foundation for Credit Counseling provide legitimate, low-cost assistance.

Understanding what happens when payments stop is the first step toward making informed decisions—whether that means negotiating with creditors, pursuing debt management plans, or considering bankruptcy as a last resort.

The key is acting deliberately rather than reactively, armed with knowledge of both the consequences and the available options.