Quick Summary: The top fintech web development companies for 2026 combine deep compliance expertise, secure infrastructure, and user-centric design to build platforms people trust with their money. This guide profiles 15 agencies—from EPAM Systems’ enterprise-scale engineering to Shakuro’s product design precision—covering what they build, who they serve, and how to evaluate the right partner for payment gateways, neobanks, blockchain platforms, and embedded finance solutions.

Fintech doesn’t tolerate weak engineering. Money moves through these systems. Regulators watch every transaction. Users demand speed, clarity, and zero friction.

A fintech web development company builds the infrastructure that powers digital banking, payment processing, lending platforms, blockchain applications, and embedded finance tools. They design for trust—because one confusing checkout flow or slow load time costs conversions. They architect for compliance—because non-compliance in fintech can trigger fines reaching €35 million or 7% of global annual turnover under the EU AI Act, with enforcement that began in 2025.

And they build for scale. According to research from the University of Chicago, 75% of fintech firms operate platform-based business models, compared to just 16% of non-fintech financial firms. That structural difference demands development partners who understand API ecosystems, real-time data synchronization, ledger logic, and multi-sided marketplace dynamics.

This guide profiles 15 fintech web development companies building production systems in 2026. No fluff, no invented metrics—just what they build, who they serve, and what sets them apart.

Why Fintech Web Development Is Different

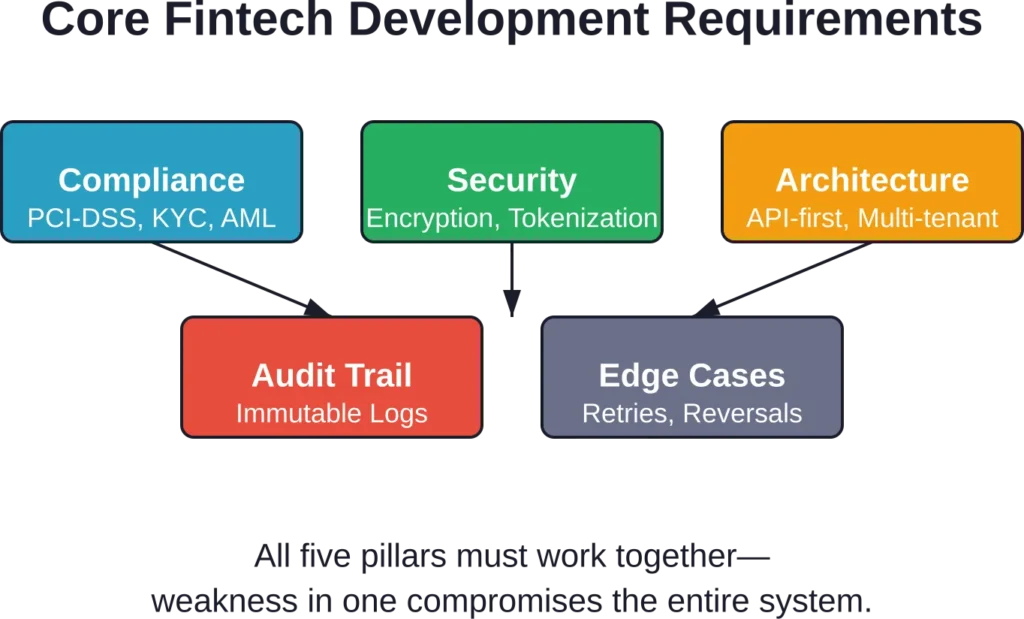

Financial software fails in ways other software doesn’t. A delayed API response in a social app annoys users. In a trading platform, it triggers regulatory scrutiny and customer losses.

Most fintech failures come from back-end logic and integrations. Strong vendors design for messy edge cases: retries, duplicates, reversals, delayed statuses, disputes. A proper ledger and audit trail aren’t optional features—they’re core to trust, reconciliation, and defensible balances.

Compliance is shared: legal sets rules, engineering implements them. PCI-DSS for payment card data. KYC and AML workflows that verify identity without creating friction. GDPR for European users. SOC 2 Type II for enterprise trust. The vendor you choose either understands these frameworks deeply or learns them on your budget.

Security isn’t a feature—it’s the foundation. Encryption at rest and in transit. Role-based access control. Tokenization of sensitive data. Penetration testing and vulnerability scanning as part of the development cycle, not an afterthought.

Platform Economics in Fintech

Research from the University of Chicago shows that 51% of fintech firms highlight customer data as a value source, nearly double the rate of traditional financial institutions. That data focus drives product decisions: personalized dashboards, predictive analytics, embedded insights that turn transaction history into actionable intelligence.

Platform models dominate because they create network effects. More users attract more merchants. More merchants attract more users. The development partner you select needs to architect for multi-tenant infrastructure, marketplace mechanics, and the API-first design that lets third parties integrate seamlessly.

Top 15 Fintech Web Development Companies for 2026

These agencies build production fintech systems. They’ve navigated compliance. They’ve scaled payment infrastructure. They understand the edge cases that break financial software.

1. Lengreo

Lengreo acts as a complete marketing and tech partner for fintech companies seeking growth through digital channels. They combine B2B lead generation, website development, and performance marketing to help financial technology firms acquire clients and scale operations efficiently.

Their strength lies in data-driven execution. They run hyper-personalized outreach campaigns, LinkedIn and email sequences, SEO optimization, and paid advertising across Meta and LinkedIn while building high-converting landing pages and client portals. Their approach focuses on measurable outcomes such as cost-per-lead reduction and opportunity generation for technology-driven financial services.

Lengreo handles full-funnel digital presence: marketing audits, conversion-focused website development, lead nurturing systems, and demand generation strategies tailored for fintech. They support both early-stage companies launching new products and established players expanding customer acquisition in competitive financial markets.

Best for: fintech companies needing consistent qualified lead flow, digital marketing optimization for financial products, teams that want integrated tech-enabled growth services.

Contact Information:

- Website: Lengreo.com

- Phone: +31 686 147 566

- Email: [email protected]

- Address: Vrijstraat 9 C/D, 5611 AT Eindhoven, Netherlands

- LinkedIn: Lengreo

- Twitter: @Lengreo

- Instagram: @lengreo

2. Gilzor

Gilzor delivers custom web and mobile development for fintech startups and product companies. They focus on turning ideas into secure, scalable digital financial products that users and investors trust.

Their strength is full-cycle product creation. They provide idea validation, business analysis, UI/UX design, web development, quality assurance, and go-to-market support using modern technology stacks that ensure performance and security. Their teams emphasize clean architecture and user-centric interfaces critical for financial applications.

Gilzor builds everything from personal finance tools and investment platforms to payment solutions and internal fintech automation systems. They handle product discovery, rapid prototyping, full development, and post-launch maintenance with a strong focus on reducing risk and achieving product-market fit.

Best for: fintech startups validating and launching new digital products, product studios expanding financial features, companies needing reliable custom web and mobile solutions.

Contact Information:

- Website: www.gilzor.com

- Email: [email protected]

- Address: Poland, Warsaw, Office 58, street Adama Mickiewicza 37, 01-625

- LinkedIn: www.linkedin.com/company/gilzor-softwaredevelopment

3. Oski

Oski builds smart, well-engineered web solutions for fintech enterprises and ambitious startups. With deep expertise in cloud architecture, modern frontend frameworks, and AI integration, they create secure and scalable financial technology platforms.

Their strength is accelerated development powered by experienced teams and modern practices. They deliver cloud-native applications, responsive frontends, and intelligent features using technologies such as React, Node.js, AWS, and Azure while maintaining high standards in security and user experience.

Oski handles complex fintech projects including digital banking interfaces, payment systems, data-driven financial tools, and AI-enhanced decision platforms. They support cloud migration, system integration, and ongoing optimization for companies that require both innovation and reliability.

Best for: fintech companies building or modernizing web-based financial platforms, teams needing AI and cloud integration, enterprises seeking high-quality custom development.

Contact Information:

- Website: oski.site

- Phone: +48571282759

- Email: [email protected]

- Address: Kaupmehe tn 7, 10114 Tallinn, Estonia

- LinkedIn: www.linkedin.com/company/oski-solutions

4. A-Listware

A-Listware provides dedicated software development teams and consulting for fintech organizations. They focus on delivering secure, high-quality web and enterprise applications through flexible outsourcing and team augmentation models.

Their strength is rapid team assembly and seamless integration. They supply experienced developers, architects, QA specialists, and DevOps engineers who work as an extension of the client’s team, with strong capabilities in legacy modernization, cloud applications, and custom fintech solutions.

A-Listware covers the full spectrum: custom software development, CRM/ERP integrations for financial services, data analytics platforms, and cybersecurity implementations. They support both greenfield fintech projects and the evolution of existing financial systems.

Best for: fintech companies scaling development capacity, organizations modernizing legacy financial software, teams requiring dedicated or augmented engineering resources.

Contact Information:

- Website: a-listware.com

- Phone: +1 (888) 337 93 73

- Email: [email protected]

- Address: North Bergen, NJ 07047, USA

- LinkedIn: www.linkedin.com/company/a-listware

- Facebook: www.facebook.com/alistware

5. Mobian Studio

Mobian Studio builds dedicated engineering teams that deliver production-ready fintech web and mobile solutions on time and within budget. They specialize in mobile-first and AI-powered applications for financial technology companies.

Their strength is focused, high-velocity delivery. They offer two engagement models — full outsourcing and outstaffing — with senior engineers experienced in clean architecture, scalable systems, and domain-specific requirements such as payment flows and regulatory compliance.

Mobian handles end-to-end development: web platforms, mobile banking apps, AI-driven fraud detection, automation workflows, and legacy system integrations. They provide ongoing support, scaling assistance, and documentation that ensures long-term maintainability.

Best for: fintech companies needing reliable dedicated teams, mobile and web financial product development, organizations integrating AI into core financial processes.

Contact Information:

- Website: mobian.studio

- Phone: [email protected]

- Address: Harju maakond, Tallinn, Kesklinnalinnaosa, Masina tn 22, 10113

- LinkedIn: www.linkedin.com/company/mobian-studio

6. TRIARE

TRIARE develops custom financial software with focus on banking, insurance, and investment management. Their technical capabilities span back-end systems, mobile applications, web platforms, and third-party integrations.

They build core banking modules, loan origination systems, insurance policy management platforms, and trading applications. Their teams have experience with financial protocols and industry standards: ISO 20022 for payment messaging, FIX protocol for trading, ACORD for insurance data exchange.

TRIARE’s approach emphasizes business analysis before architecture. They map existing workflows, identify bottlenecks, and design systems that improve operational efficiency while meeting regulatory requirements. Their documentation includes technical specs, API references, and compliance matrices.

They work with both established financial institutions modernizing systems and fintechs building new products. Their engagement models range from fixed-scope projects to dedicated teams that scale up or down based on product roadmap needs.

Best for: banking and insurance software, companies needing industry protocol expertise, projects requiring business process analysis.

7. Itexus

Itexus specializes in blockchain and cryptocurrency development alongside traditional fintech applications. They build decentralized finance (DeFi) platforms, crypto exchanges, wallet applications, and tokenization systems.

Their blockchain expertise covers multiple protocols: Ethereum, Binance Smart Chain, Polygon, Solana. They develop smart contracts, implement consensus mechanisms, and design tokenomics. Their security practices include smart contract audits, penetration testing, and vulnerability assessments—critical for systems where bugs cost millions.

Beyond blockchain, Itexus builds payment platforms, lending applications, and financial management tools. They integrate blockchain capabilities with traditional banking APIs, creating hybrid systems that leverage both centralized and decentralized infrastructure.

Their teams understand the regulatory landscape for digital assets, including securities law implications, AML requirements for crypto transactions, and licensing considerations for exchanges and wallet providers.

Best for: blockchain and cryptocurrency projects, DeFi platforms, companies integrating digital assets, hybrid centralized/decentralized systems.

8. Code & Pepper

Code & Pepper develops web and mobile fintech products with emphasis on payments, lending, and personal finance. Their technical stack includes React, Angular, Node.js, and native mobile development (Swift, Kotlin).

They build payment processing systems that integrate with Stripe, PayPal, and banking APIs. Their architecture supports PCI-DSS requirements: tokenization, secure card storage, and encrypted transmission. They implement 3D Secure authentication and fraud detection rules.

Code & Pepper’s product development process includes user research, wireframing, visual design, development, and post-launch optimization. They run A/B tests on critical flows, instrument analytics, and iterate based on data. Their clients have reported conversion increases after interface redesigns that simplified multi-step processes.

They provide ongoing maintenance and feature development, functioning as a long-term product partner rather than a one-time vendor. Their retainer models support continuous improvement and rapid response to regulatory changes.

Best for: payment platforms, lending applications, companies needing PCI-DSS compliant development, long-term product partnerships.

9. Skywell Software

Skywell Software builds custom fintech applications with focus on banking, wealth management, and insurance. They handle complex integration projects: connecting modern front-ends to legacy core banking systems, migrating data from mainframes to cloud databases, and building API layers over decades-old infrastructure.

Their engineering teams have experience with both modern and legacy technologies: COBOL, Java, .NET, Python, microservices, and cloud platforms. They design migration strategies that minimize downtime and maintain data integrity during transitions.

Skywell’s process emphasizes risk management. They document dependencies, create rollback plans, and implement phased migrations that allow incremental validation. Their testing protocols include unit tests, integration tests, load tests, and user acceptance tests that catch issues before production.

They work with regional banks, credit unions, and insurance companies that need to modernize without replacing core systems entirely. Their hybrid architectures let clients build new customer experiences while preserving investments in existing infrastructure.

Best for: legacy system modernization, banking and insurance companies, projects requiring integration with mainframe systems, phased migration strategies.

10. Inoxoft

Inoxoft develops fintech software using Python, Django, React, and React Native. Their portfolio includes payment systems, trading platforms, robo-advisors, and financial analytics tools.

They architect for data intensity: systems that process transaction streams, calculate risk metrics, generate reports, and display real-time dashboards. Their back-end designs use message queues, caching layers, and optimized database queries to handle high-throughput scenarios.

Inoxoft’s security implementation includes multi-factor authentication, role-based access control, encryption key management, and audit logging. They’ve helped clients pass security assessments from banks, pass SOC 2 audits, and meet GDPR requirements for European users.

Their engagement model emphasizes transparency: weekly demos, sprint retrospectives, and open access to project management tools. They integrate with client Slack channels, attend product planning sessions, and collaborate on technical decisions.

Best for: data-intensive fintech applications, trading and analytics platforms, companies using Python/Django stacks, teams that value transparent collaboration.

11. EPAM Systems

EPAM operates at enterprise scale. With over 18 years of experience and a global delivery model, they build core banking platforms, payment processing systems, and wealth management applications for Fortune 500 financial institutions.

Their strength is engineering depth. They maintain teams with expertise in front-end frameworks, back-end microservices, cloud architecture (AWS, Azure, GCP), AI-enhanced applications, and full product lifecycle support. They staff from the top 1.6% of engineers globally, which translates to teams that can navigate complex regulatory requirements and legacy system integrations.

EPAM handles the full spectrum: digital transformation for incumbent banks, greenfield neobank development, payment gateway integrations, and blockchain infrastructure. They’re built for projects that span multiple countries, require SOC 2 compliance, and integrate with decades-old core banking systems.

Best for: enterprises modernizing legacy financial systems, banks launching digital channels, large-scale payment infrastructure.

12. Shakuro

Shakuro specializes in product design and development for fintech startups and scaleups. Their portfolio shows depth in mobile banking apps, investment platforms, and payment interfaces that prioritize user experience without sacrificing security.

They combine UI/UX design, front-end development, and product strategy. Their process emphasizes user research, rapid prototyping, and iterative testing—critical for fintech products where one confusing flow kills conversion.

Shakuro’s case studies demonstrate measurable results. They’ve delivered financial management platforms that achieved 30% engagement increases through interface simplification and interaction design improvements. Their design systems balance regulatory disclosure requirements with clean visual hierarchies.

They work with venture-backed fintechs launching MVPs and established companies redesigning customer-facing applications. Their agile approach fits product teams that iterate based on user feedback and analytics.

Best for: fintech startups building consumer-facing apps, scaleups redesigning core products, teams that prioritize design quality.

13. JetRuby Agency

JetRuby builds custom web and mobile applications for fintech companies using Ruby on Rails, React, and React Native. Their technical stack fits products that need rapid development cycles and clean, maintainable code.

Their fintech portfolio includes lending platforms, peer-to-peer payment systems, cryptocurrency wallets, and investment management tools. They handle end-to-end development: architecture design, API integrations, payment processor connections, and compliance implementations.

JetRuby emphasizes product discovery before development. They run workshops to define MVP scope, validate assumptions through prototypes, and establish technical architecture that scales beyond launch. Their teams integrate with client product and engineering organizations, functioning as an extension rather than a vendor.

They’ve built systems that process thousands of transactions daily, integrate with banking APIs, and meet PCI-DSS requirements. Their approach suits companies that need custom solutions rather than templated builds.

Best for: mid-market fintech companies, custom lending platforms, cryptocurrency applications, products requiring Ruby on Rails expertise.

14. BairesDev

BairesDev operates as a nearshore development partner with delivery centers across Latin America. They build software for financial services companies, payment processors, and fintech startups that need dedicated development teams.

Their model provides staff augmentation and dedicated teams: engineers, designers, QA specialists, and DevOps professionals who integrate with client organizations. They maintain rigorous hiring standards, selecting engineers with financial services experience.

BairesDev’s fintech work spans mobile banking applications, payment gateways, fraud detection systems, and blockchain platforms. They support both greenfield development and legacy modernization, with teams experienced in integrating modern APIs with older COBOL and mainframe systems.

Their delivery model emphasizes time zone alignment with US clients, English fluency, and agile processes. They handle security audits, penetration testing, and compliance documentation as part of standard delivery.

Best for: companies needing dedicated development teams, staff augmentation for fintech projects, nearshore delivery with US time zone overlap.

15. TechMagic

TechMagic builds web and mobile fintech products using JavaScript frameworks (React, Node.js, React Native) and AWS cloud infrastructure. Their technical focus suits startups and growth-stage companies launching digital financial products.

Their portfolio includes challenger banks, payment applications, personal finance management tools, and investment platforms. They architect for AWS, implementing serverless functions, managed databases, and auto-scaling infrastructure that handles traffic spikes without manual intervention.

TechMagic’s process integrates DevOps from day one: CI/CD pipelines, automated testing, infrastructure as code, and monitoring dashboards. Their teams build products that deploy daily, with feature flags and gradual rollouts that minimize risk.

They emphasize speed without compromising security. Their baseline includes encryption, tokenization, secure authentication (OAuth 2.0, JWT), and logging that supports compliance audits. They’ve helped clients achieve SOC 2 certification and pass security assessments from enterprise customers.

Best for: fintech startups building AWS-native products, companies prioritizing JavaScript stacks, teams that deploy frequently.

How to Evaluate a Fintech Development Partner

Not every agency that builds software can build fintech software. The selection criteria differ.

Portfolio Depth in Financial Services

Look for case studies that show payment flows, ledger logic, or regulatory approval processes. Generic “we built an app” portfolios don’t translate. The agency should demonstrate:

- Integration with payment processors (Stripe, Plaid, Adyen, etc.)

- Implementation of KYC/AML workflows

- Handling of financial reconciliation and reporting

- Multi-currency and cross-border transaction support

- Audit trail and compliance documentation

Security Posture and Certifications

Ask about their own security practices. Do they hold SOC 2 certification? ISO 27001? Do they run internal penetration tests? What’s their incident response protocol?

A vendor building fintech products should treat security as infrastructure, not a checklist. Their development environment should enforce code reviews, automated security scanning, and secrets management. If they can’t articulate their internal security stack, they’re not ready to build yours.

Compliance Knowledge

Regulations vary by jurisdiction. PSD2 in Europe. Dodd-Frank in the US. Open Banking standards in the UK. A strong fintech development partner either has direct experience in your target markets or demonstrates a structured approach to learning new regulatory frameworks.

They should ask questions about your compliance requirements early—during scoping, not after development starts. If they don’t, they’re learning compliance on your timeline.

Technical Architecture Philosophy

Strong fintech vendors design for failure. They build idempotent APIs (so retrying a failed payment doesn’t charge twice). They implement circuit breakers (so one failing service doesn’t cascade). They log everything (so disputes can be traced to the exact API call).

Ask how they handle eventual consistency. How they design for high availability. How they test disaster recovery. The answers reveal whether they’ve built production fintech systems or just talked about them.

Team Structure and Continuity

Fintech projects accumulate domain knowledge over time. The engineer who built your ledger logic understands edge cases the documentation doesn’t capture. High team turnover means that knowledge walks out the door.

Ask about team stability. How long do engineers typically stay? What’s their knowledge transfer process? Do they document architectural decisions? Strong agencies treat institutional knowledge as an asset and invest in preserving it.

| Selection Criterion | What to Look For | Red Flags |

|---|---|---|

| Portfolio | Specific fintech case studies with payment flows, compliance workflows, and financial reconciliation examples | Generic app projects with no financial services depth |

| Security | SOC 2 or ISO 27001 certification, documented security practices, automated scanning in CI/CD pipeline | Vague answers, no certifications, security treated as a feature |

| Compliance | Asks detailed questions about regulatory requirements during discovery, has experience in target jurisdictions | Doesn’t mention compliance until late in scoping, no regulatory experience |

| Architecture | Discusses idempotency, circuit breakers, audit trails, and disaster recovery proactively | Focuses only on front-end design, no mention of failure handling |

| Team Stability | Low turnover, documented knowledge transfer, long-term client relationships | High churn, frequent team changes, lack of continuity |

Industry Trends Shaping Fintech Development in 2026

The fintech landscape keeps shifting. Development priorities follow.

AI Integration and Agentic Finance

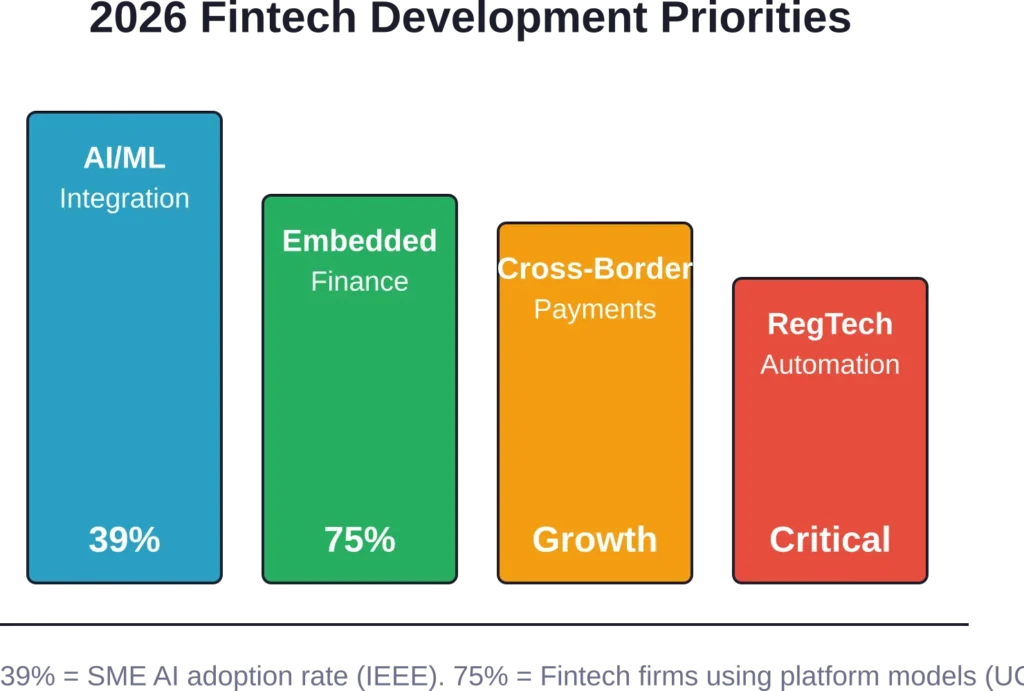

According to IEEE Standards Association research, 39% of SMEs now use AI applications in 2026, up from 26% in 2024. Fintech leads that adoption. AI powers fraud detection, credit scoring, customer support chatbots, and personalized financial recommendations.

But 2026 introduces agentic AI—systems that make decisions and execute transactions autonomously. A May 2025 Wolters Kluwer survey found that 6% of finance leaders currently use agentic AI, with another 38% planning adoption within 12 months. That puts pressure on infrastructure: corporate finance software built for human approval queues doesn’t fit an economy where AI agents move money on their own behalf.

Stripe, FIS, and a new wave of agent-native fintech startups are racing to build the infrastructure layer. Development companies that understand this shift are designing APIs for machine clients, implementing rate limits that prevent runaway spending, and building audit systems that explain automated financial decisions.

Embedded Finance and Platform Models

Non-financial companies are embedding banking, payments, and lending directly into their products. Software platforms offer business bank accounts. E-commerce sites provide instant financing at checkout. Accounting tools connect to payment processors and automate reconciliation.

That embedded model demands modular architecture: APIs that let non-fintech companies add financial features without building regulatory infrastructure. Development partners need to design systems that function as both standalone products and embeddable components.

Cross-Border Payments and Emerging Markets

Research from Harvard Business School shows payment costs in Sub-Saharan Africa range from 8.7% to 12.6% of transaction value—far above the UN Sustainable Development Goal target of 3%. Fintech innovations in cross-border payments are closing that gap.

Startups like Airwallex (valued at $6.2 billion after a $300 million round) and Nala are building infrastructure that reduces friction and cost. Development companies working in this space handle multi-currency support, foreign exchange calculations, correspondent banking integrations, and compliance with regulations in multiple jurisdictions simultaneously.

According to Harvard research, venture capital flowing to African fintech reached $1 billion in 2025, with companies like Flutterwave (valued at $3 billion in 2022) leading the ecosystem. Development partners serving these markets need to design for mobile-first users, low-bandwidth conditions, and offline functionality.

Regulatory Technology (RegTech)

Compliance costs keep rising. RegTech automates regulatory reporting, transaction monitoring, and risk assessment. Development companies are building tools that:

- Monitor transactions in real time for suspicious patterns

- Generate regulatory reports automatically

- Track changes in regulations and update systems accordingly

- Verify customer identities through biometric authentication and document verification

- Maintain audit trails that regulators can access during examinations

According to Forbes, companies like Socure verified 5 billion identity requests in 2025 and generated $200 million in revenue. The demand for identity verification and fraud prevention creates opportunities for development agencies that understand both the technology and the regulatory requirements.

Buy Now, Pay Later (BNPL) and Alternative Lending

BNPL services have embedded credit directly into online checkout flows. Companies like Tabby (implied valuation of $4.5 billion after a secondary share sale in late 2025) and Tamara (which secured a $2.4 billion financing package in 2025) are expanding across markets.

Development work in BNPL requires integration with e-commerce platforms, real-time credit decisioning, payment scheduling, collections workflows, and regulatory compliance for consumer lending. The technical architecture must handle high transaction volumes during peak shopping periods without latency or failures.

Cryptocurrency and DeFi Maturation

According to Forbes, crypto platforms like Hyperliquid processed $2.95 trillion in trading volume in 2025, less than two years after launch. Ripple reached a $40 billion valuation after a $500 million funding round. The infrastructure is maturing.

Development agencies working in crypto focus on security (smart contract audits, multi-signature wallets, cold storage), scalability (layer-2 solutions, optimistic rollups), and regulatory compliance (travel rule for transfers, securities classification for tokens). The technical challenges differ from traditional fintech but the stakes—security, compliance, user trust—remain identical.

What to Expect During the Development Process

Fintech projects follow a different cadence than other software development. Here’s what the process typically looks like.

Discovery and Compliance Mapping

Strong agencies start with discovery workshops that map business requirements to regulatory obligations. They identify which jurisdictions apply, what licenses you need, which data protection laws govern user information, and what reporting requirements exist.

This phase produces compliance matrices: documents that list every regulatory requirement and show how the system architecture addresses it. That documentation becomes critical during audits, security assessments, and licensing applications.

Architecture Design

The architecture phase defines the technical foundation: database schemas, API contracts, authentication flows, payment processor integrations, and infrastructure components. Strong vendors produce architecture diagrams, API specifications, data flow diagrams, and threat models.

This phase should address scalability early. How does the system handle 10x transaction volume? What happens when a third-party API goes down? How does the ledger maintain consistency during network partitions?

Iterative Development

Most fintech projects use agile methodology: two-week sprints, regular demos, continuous integration. But fintech agile differs from generic agile. Test coverage requirements are higher. Code review standards are stricter. Security checks happen in every sprint, not just before launch.

Expect slower initial velocity as teams establish patterns, security protocols, and testing frameworks. Velocity accelerates once those foundations solidify.

Security Testing and Compliance Validation

Before launch, strong vendors run penetration tests, vulnerability scans, and compliance audits. They test for common vulnerabilities: SQL injection, cross-site scripting, insecure authentication, exposed secrets. They validate that the system meets PCI-DSS requirements, implements required disclosures, and logs transactions appropriately.

This phase often uncovers issues that require rework. Budget time for remediation cycles—they’re normal in fintech, not a sign of poor development.

Staged Rollout

Financial systems rarely launch to full user bases immediately. The pattern: soft launch to internal users, beta with limited external users, gradual expansion with monitoring at each stage. Feature flags let teams enable functionality for subsets of users and disable it instantly if issues appear.

Monitoring during rollout tracks transaction success rates, API latency, error rates, and user behavior. Dashboards show real-time system health. Alerts notify teams of anomalies before users complain.

Common Pitfalls When Choosing a Fintech Developer

Certain mistakes appear repeatedly. Here’s what to avoid.

Prioritizing Cost Over Competence

Cheap fintech development is expensive. The agency that costs 40% less but lacks compliance experience will cost multiples more when regulators find gaps or security audits fail. Fixing production security issues costs 10-100x more than building security correctly from the start.

Ignoring Regulatory Experience

Agencies that build e-commerce sites can’t simply pivot to fintech. The regulatory knowledge, security protocols, and architectural patterns differ fundamentally. Verify that the agency has shipped production fintech systems that passed compliance audits.

Skipping Security Assessments

Ask to see the agency’s own security practices. If they can’t produce SOC 2 reports, security policies, or penetration test results, they’re not prepared to build your secure system. Vendor security matters—data breaches often originate from third-party access.

Underestimating Integration Complexity

Payment processor APIs look simple in documentation. Real implementations handle webhooks that arrive out of order, idempotency keys, dispute workflows, refunds, partial captures, and currency conversions. Budget 30-50% more time for integrations than initial estimates suggest.

Neglecting Ongoing Maintenance

Fintech products require continuous maintenance: regulatory updates, security patches, API version migrations, infrastructure updates, and performance optimization. One-time development contracts create technical debt. Structure engagements to include ongoing support.

Questions to Ask Potential Development Partners

These questions reveal whether an agency understands fintech development:

- “Show me three fintech projects you’ve launched. What compliance frameworks did they need to meet?” Vague answers or projects that didn’t face regulatory requirements are red flags.

- “How do you handle PCI-DSS compliance?” Strong answers discuss tokenization, secure storage, network segmentation, and annual audits. Weak answers focus only on using third-party processors.

- “What’s your approach to audit trails?” Look for specific technical details: immutable logs, cryptographic signatures, retention policies, and query interfaces for compliance teams.

- “How do you test payment integrations?” Strong vendors use sandbox environments, mock failing API calls, test idempotency, and verify webhook handling.

- “What happens when a payment processor API goes down?” Good answers discuss circuit breakers, fallback providers, user communication, and manual reconciliation processes.

- “How do you stay current with regulatory changes?” Agencies should describe monitoring processes, legal partnerships, or compliance advisory relationships.

- “What’s your security incident response protocol?” Detailed runbooks, defined communication channels, and tested procedures indicate maturity.

The True Cost of Fintech Development

Fintech development costs more than generic software development. Security requirements, compliance work, integration complexity, and testing rigor all drive costs higher.

Typical cost drivers include:

- Compliance implementation: Building KYC workflows, implementing data protection controls, creating audit trails, and documenting regulatory coverage.

- Security infrastructure: Encryption, tokenization, secure authentication, intrusion detection, and penetration testing.

- Payment integrations: Connecting to processors, handling edge cases, implementing reconciliation, and building admin tooling.

- Testing: Unit tests, integration tests, security tests, load tests, and user acceptance tests require more coverage than non-fintech projects.

- Documentation: API references, architecture diagrams, security documentation, and compliance matrices.

Budget appropriately. Underfunding fintech development creates technical debt that compounds. Systems built without proper security require expensive rewrites. Compliance gaps discovered late trigger costly remediation cycles.

Frequently Asked Questions

Fintech development requires deep compliance knowledge, security-first architecture, and handling of financial edge cases that generic development doesn’t encounter. Agencies must understand regulatory frameworks (PCI-DSS, KYC, AML), implement proper audit trails, design idempotent APIs, and build systems where bugs have financial consequences. Most fintech failures come from back-end logic and integrations, not design issues.

Timelines vary by complexity. A basic MVP payment integration takes 3-4 months. A neobank with lending features takes 9-18 months. Enterprise banking modernization can span 2-3 years. Compliance validation, security testing, and integration work add 30-50% to initial estimates. Phased rollouts are standard—financial systems rarely launch to full user bases immediately.

Look for SOC 2 Type II certification (proves ongoing security controls), ISO 27001 (information security management), and documented experience with PCI-DSS implementations. The agency should demonstrate knowledge of regulatory frameworks in your target markets: PSD2 in Europe, Dodd-Frank in the US, Open Banking standards in the UK. Ask for compliance matrices from previous projects.

Specialized agencies like Itexus build blockchain infrastructure, DeFi platforms, crypto exchanges, and tokenization systems. Blockchain development requires different expertise: smart contract security, consensus mechanisms, protocol selection, and crypto-specific regulatory compliance. According to Forbes data, platforms like Hyperliquid processed $2.95 trillion in trading volume in 2025, showing mature infrastructure demand.

Strong development partners implement currency conversion with real-time exchange rates, handle correspondent banking integrations, manage multi-jurisdictional compliance, and design for the high costs of emerging markets. Harvard Business School research shows Sub-Saharan Africa payment costs range from 8.7% to 12.6% of transaction value. Companies like Airwallex (valued at $6.2 billion) and Nala are building infrastructure that reduces these frictions.

AI powers fraud detection, credit scoring, customer support automation, and personalized recommendations. According to IEEE research, 39% of SMEs now use AI applications in 2026, up from 26% in 2024. Agentic AI—systems that make autonomous financial decisions—creates new architectural demands. Development partners design APIs for machine clients, implement guardrails to prevent runaway spending, and build audit systems that explain automated transactions.

Specialized fintech agencies bring regulatory knowledge, security protocols, and architectural patterns that general developers lack. They’ve navigated compliance audits, passed security assessments, and handled financial edge cases. Generic agencies learning fintech on your project increase risk and timeline. University of Chicago research shows 75% of fintech firms operate platform-based models requiring specific technical architecture—specialist agencies understand these patterns.

Conclusion: Choosing the Right Fintech Development Partner

Fintech development isn’t a commodity. The agency you choose becomes responsible for systems that handle real money, face regulatory scrutiny, and require user trust.

The 15 companies profiled here—EPAM Systems, Shakuro, JetRuby Agency, BairesDev, TechMagic, TRIARE, Itexus, Code & Pepper, Skywell Software, and Inoxoft—bring proven fintech expertise. They’ve shipped production systems. They understand compliance. They design for the edge cases that break financial software.

But the right partner depends on your specific needs. Enterprise modernization requires different capabilities than startup MVPs. Blockchain platforms demand different expertise than payment gateways. Cross-border remittances face different challenges than domestic lending.

Start by mapping your requirements: regulatory jurisdictions, compliance frameworks, integration needs, security standards, and scale expectations. Then evaluate agencies against those criteria. Look for portfolio depth in relevant project types. Verify security certifications. Ask detailed questions about compliance implementation and edge-case handling.

Budget appropriately. Underfunded fintech projects accumulate technical debt that costs multiples to fix later. Strong security, proper compliance, and robust architecture aren’t optional—they’re the foundation that determines whether your product survives regulatory scrutiny and earns user trust.

The fintech landscape keeps evolving. AI integration, embedded finance, cross-border innovation, RegTech automation, and cryptocurrency maturation all create new development demands. The agencies that keep pace—investing in new capabilities, understanding emerging regulations, and adapting architecture patterns—become valuable long-term partners.

Choose carefully. Production financial systems don’t forgive mistakes. But with the right development partner, you can build platforms that process transactions securely, meet compliance requirements, and deliver experiences that users trust.

Ready to start your fintech development project? Research the agencies listed here, review their portfolios, and schedule discovery calls with those that match your project requirements. Ask tough questions. Verify claims. And build on a foundation that supports growth, not one that requires expensive rebuilds.