Quick Summary: If you crash a rental car, you must document the accident, report it to the rental company and police, and determine coverage through your personal auto insurance, credit card benefits, or rental company protection plans. Liability depends on fault, insurance coverage, and whether you purchased optional waivers. Without adequate coverage, you could face costs for vehicle damage, loss of use fees, administrative charges, and potential lawsuits.

Getting into an accident is stressful enough. But when it happens in a rental car, the situation becomes significantly more complicated.

Who pays for the damage? What does the rental company expect? Will insurance cover everything?

These questions run through anyone’s mind after crashing a rental vehicle. The answers depend on several factors: the type of insurance coverage in place, who caused the accident, and what protections were purchased at the rental counter.

Here’s everything that happens after a rental car crash and how to navigate the aftermath without unnecessary financial exposure.

Immediate Steps After a Rental Car Accident

The first actions taken at the accident scene determine how smoothly everything unfolds afterward.

Safety and Documentation Come First

Before anything else, ensure everyone’s safety. Move vehicles out of traffic if possible and activate hazard lights. Call emergency services if anyone is injured.

Once safety is secured, documentation becomes critical. Take photos of all vehicle damage from multiple angles, road conditions, traffic signs, and the accident scene layout. Capture license plates, VIN numbers, and vehicle positions.

Exchange information with other drivers involved: names, contact details, insurance information, and driver’s license numbers. If witnesses are present, get their contact information as well.

According to GSA accident management guidelines, stopping safely and documenting facts immediately helps with claims processing and third-party disputes.

Contact Law Enforcement

Many rental agreements require a police report for any accident, regardless of severity. Even minor fender benders should be reported.

Wait for officers to arrive and file an official report. Request the report number and the responding officer’s information. This document becomes essential evidence for insurance claims and rental company procedures.

Notify the Rental Company Immediately

Most rental agreements require notification within a specific timeframe—often 24 hours. Delaying this call can void certain protections.

The rental company will provide specific instructions, which typically include filling out their incident report form. This differs from the police report and captures details the company needs for their records.

According to University of Maryland Baltimore’s risk management guidelines, signing rental contracts with the driver’s name followed by organizational affiliations can affect liability protection—this principle applies to how rental companies process accident claims.

Understanding Liability: Who Pays for What?

Financial responsibility after a rental car crash isn’t always straightforward.

When You’re at Fault

If you caused the accident, responsibility for damages typically falls on whatever insurance coverage is active. This could be personal auto insurance, credit card benefits, or rental company protection products.

Without any coverage, personal liability kicks in. The rental company will charge for vehicle repairs, loss of use (revenue they lose while the car is being fixed), administrative fees, and towing costs.

Rental companies typically charge retail repair rates plus additional administrative and processing fees.

When Another Driver Is at Fault

If another driver caused the accident, their liability insurance should cover rental vehicle damage. However, collecting from a third party can take weeks or months.

The rental company typically requires the renter to handle the vehicle damage costs initially, then seek reimbursement from the at-fault driver’s insurance carrier. This means fronting potentially thousands of dollars while waiting for claims to process.

The Rental Company’s Role

Rental companies rarely accept direct liability for accidents unless company negligence contributed—such as defective brakes or bald tires they failed to maintain.

Their rental agreements typically place full responsibility on the driver for any damage occurring during the rental period, with limited exceptions for normal wear and tear or acts of nature.

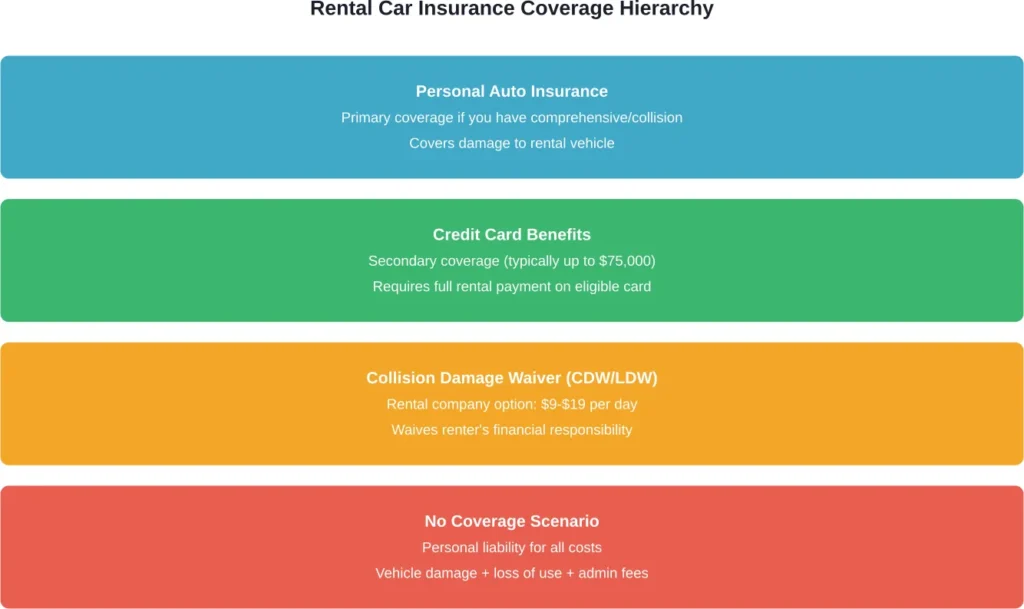

Insurance Coverage Options for Rental Cars

Multiple layers of potential coverage exist. Understanding which applies requires checking several sources.

Personal Auto Insurance

Most personal auto insurance policies extend coverage to rental vehicles. If the policy includes comprehensive and collision coverage for owned vehicles, it typically applies to rentals as well.

However, this isn’t universal. Some policies exclude rentals or only cover liability, not damage to the rental vehicle itself. Checking with the insurance carrier before renting is essential.

According to the Insurance Information Institute, comprehensive and collision coverage for rentals typically applies with similar deductibles to owned vehicles.

Credit Card Rental Car Coverage

Many credit cards offer rental car protection as a cardholder benefit. But there’s a catch: this coverage is almost always secondary, not primary.

Secondary coverage means it only applies after personal auto insurance is exhausted. The card benefit covers the deductible and any costs beyond personal policy limits.

Some premium cards provide primary coverage, meaning they pay first without requiring personal insurance involvement. Coverage limits typically reach $75,000, according to card benefit documentation.

This protection requires paying for the entire rental with the eligible card and declining the rental company’s collision damage waiver. Certain vehicle types—luxury cars, trucks, vans—often aren’t covered.

Collision Damage Waiver (CDW/LDW)

The rental company’s own protection product is technically not insurance—it’s a waiver. By purchasing it, the company waives its right to charge the renter for vehicle damage.

According to the Insurance Information Institute, loss damage waivers generally cost between $9 and $19 per day, though costs may vary. For a two-week rental, that’s $126 to $266 in additional costs.

The waiver typically covers the rental vehicle damage, towing, and loss of use fees. But it comes with important exclusions.

When Waivers Become Void

Loss damage waivers contain strict terms. Violations void the protection, leaving the renter personally liable despite paying for coverage.

Common exclusions include: – Driving under the influence of alcohol or drugs – Speeding or reckless driving – Operating the vehicle on unpaved roads – Allowing unauthorized drivers – Using the vehicle for commercial purposes

According to Insurance Information Institute materials, waivers may become void if the accident resulted from prohibited activities, even if the renter paid daily waiver fees throughout the rental period.

Supplemental Liability Protection

Beyond damage to the rental vehicle itself, liability for injuries and property damage to others matters.

Rental companies offer Supplemental Liability Protection (SLP), which provides additional liability coverage beyond what personal auto insurance includes. According to Enterprise documentation, supplemental liability protection costs vary by location, averaging between $5.99 and $15.67 per day.

Personal auto insurance liability limits transfer to rental vehicles in most cases. Someone with 100/300/100 liability coverage on their personal policy maintains that protection when driving a rental.

Costs Beyond Vehicle Repairs

The actual repair bill is just one component of total accident costs.

Loss of Use Charges

Rental companies charge for revenue lost while the damaged vehicle sits in a repair shop instead of generating rental income.

These fees accumulate daily and can significantly increase total accident costs. Loss of use fees typically range from $30 to $75 per day according to rental industry standards.

Administrative and Processing Fees

Rental companies apply administrative fees for processing accident claims, coordinating repairs, and handling paperwork. These flat fees range from $50 to several hundred dollars.

Diminished Value Claims

Some rental companies pursue diminished value claims—the difference between the vehicle’s pre-accident value and post-repair value, even after proper repairs.

A car with accident history sells for less than an identical vehicle without accidents. Rental companies sometimes charge renters for this market value reduction.

| Cost Component | Typical Range | Who Pays |

|---|---|---|

| Vehicle Repairs | $500 – $15,000+ | Insurance or renter |

| Loss of Use | $30 – $75 per day | Usually renter liability |

| Administrative Fees | $50 – $500 | Renter liability |

| Towing/Storage | $100 – $400 | Covered by most waivers |

| Diminished Value | 10-20% of vehicle value | Disputed, often renter |

What Happens If You Don’t Have Insurance

Crashing a rental without any coverage creates maximum financial exposure.

The rental company will charge the renter’s credit card on file for all costs: repairs, loss of use, administrative fees, and any other expenses. If the card limit is insufficient, the company pursues payment through collections or legal action.

Without insurance coverage, there’s no entity negotiating repair costs or challenging excessive charges. Rental companies charge retail rates, which exceed what insurance companies pay after negotiated discounts.

According to University of Maryland Baltimore risk management documentation, self-insured entities face deductibles of $1,000 per incident as a baseline—individual renters without coverage face the full amount.

Dealing with the Rental Company After the Crash

Rental companies follow specific procedures after accidents.

The Damage Assessment Process

The company inspects the vehicle and documents all damage. This assessment determines the repair scope and cost estimate.

Renters should request to be present during this inspection when possible. Challenging damage claims becomes difficult after the fact.

Incident Reports and Documentation

Rental companies require completed incident reports with detailed accident information. Accuracy matters—inconsistencies between the police report, incident report, and insurance claim create complications.

Keep copies of everything: the rental agreement, incident report, police report, photos, and all correspondence with the rental company.

Charges and Billing

Most rental companies charge the credit card on file immediately for estimated damages. They may place holds for thousands of dollars while final costs are determined.

If insurance will cover the costs, the renter still typically pays first, then seeks reimbursement from their insurance carrier. This creates cash flow issues for many people.

When Legal Help Becomes Necessary

Some rental car accident situations require legal representation.

Disputes Over Responsibility

When the rental company pursues charges the renter believes are unfair or excessive, legal assistance helps navigate the dispute.

Renters should be aware that disputes can arise regarding pre-existing damage assessments, repair cost calculations, or loss of use fee determinations.

Third-Party Injury Claims

If other people were injured in the accident, they may file claims or lawsuits against the renter. Legal representation becomes essential, especially if injury claims exceed insurance policy limits.

Coverage Denials

Insurance companies sometimes deny coverage for rental car accidents based on policy exclusions or alleged contract violations. Attorneys specializing in insurance disputes can challenge these denials.

Special Situations and Considerations

International Rentals

Crashing a rental car abroad introduces additional complexity. Personal U.S. auto insurance often doesn’t extend to international rentals. Credit card coverage may or may not apply depending on the card terms and country.

Many countries require purchasing the rental company’s insurance regardless of other coverage. Navigating foreign legal systems and insurance claims processes presents significant challenges.

Long-Term Rentals

Extended rental periods—weeks or months—sometimes involve different insurance arrangements. Some long-term rental agreements include insurance in the daily rate, while others require proof of personal coverage.

Business vs. Personal Rentals

Rentals for business purposes may be covered under commercial auto policies rather than personal insurance. Company policies vary widely in how they handle rental vehicle coverage.

According to UCSD risk management guidelines, institutional rentals require specific contract signing procedures to secure proper liability protection—similar principles apply to business rentals.

Preventing Rental Car Accidents

While not foolproof, certain practices reduce accident risk.

Thoroughly inspect the rental before leaving the lot. Document existing damage with photos and ensure it’s noted on the rental agreement. This prevents disputes over pre-existing damage later.

Familiarize yourself with the vehicle’s controls, blind spots, and handling characteristics before entering traffic. Rental cars vary significantly from personal vehicles.

Drive defensively and follow all traffic laws. Remember that loss damage waivers become void with traffic violations like speeding.

Avoid risky situations: don’t drive on unpaved roads unless the rental agreement specifically permits it, don’t let unauthorized drivers operate the vehicle, and never drive impaired.

Frequently Asked Questions

Most personal auto insurance policies extend liability coverage to rental vehicles. Comprehensive and collision coverage typically applies to rentals as well, but not all policies include this. Check with your insurance carrier before renting to confirm your specific coverage and understand your deductible amount.

A collision damage waiver (CDW) or loss damage waiver (LDW) is the rental company’s protection product that waives their right to charge you for vehicle damage. According to the Insurance Information Institute, these cost between $9 and $19 per day. Whether you need it depends on your existing coverage through personal insurance and credit cards. If you lack comprehensive and collision coverage on your personal policy and don’t have credit card rental protection, purchasing the waiver provides important protection.

Credit card rental car coverage typically provides secondary protection up to $75,000, meaning it covers amounts after your personal auto insurance is applied. Some premium cards offer primary coverage. However, this protection usually excludes certain vehicle types like luxury cars, large SUVs, and trucks. Coverage only applies if you paid for the entire rental with the eligible card and declined the rental company’s collision damage waiver.

Without insurance coverage, you become personally liable for all costs: vehicle repairs, loss of use fees while the car is being fixed, administrative charges, towing, and any other expenses. The rental company will charge your credit card on file for these costs and pursue collections or legal action if the charges exceed available credit. Total costs can easily reach thousands or tens of thousands of dollars depending on damage severity.

Yes, rental agreements typically make the renter responsible for damage regardless of fault. The rental company expects you to pay for damages initially, then you must seek reimbursement from the at-fault driver’s insurance carrier. This process can take weeks or months, during which you’ve already paid the rental company or had charges applied to your credit card.

Most rental agreements require notification within 24 hours of an accident, though specific timeframes vary by company. Failing to report within the required window can void coverage protections and violate the rental agreement terms. Contact the rental company as soon as safely possible after the accident, even for minor damage.

Beyond actual repair costs, rental companies typically charge loss of use fees (daily rental revenue lost while the car is being repaired), administrative processing fees, towing and storage costs, and sometimes diminished value claims for the vehicle’s reduced resale value after repairs. According to typical rental company practices, loss of use fees range from $30 to $75 per day, and administrative fees can reach several hundred dollars.

Taking Control After a Rental Car Crash

Accidents in rental vehicles create complicated situations with multiple parties, insurance layers, and potential financial exposure.

The key to minimizing problems: know your coverage before renting, document everything thoroughly if an accident occurs, report immediately to all relevant parties, and understand your rights and responsibilities under the rental agreement.

Most rental car accident situations resolve through existing insurance coverage—personal auto policies, credit card benefits, or purchased waivers. But gaps in coverage can create significant out-of-pocket costs.

Before picking up the rental keys, verify what protection already exists through personal insurance and credit cards. Consider whether purchasing the rental company’s collision damage waiver makes financial sense based on coverage gaps and deductible amounts.

If an accident does occur, act quickly and methodically. Document, report, and preserve all evidence. Challenge unreasonable charges and seek legal assistance when rental companies pursue excessive fees or when coverage disputes arise.

Understanding these processes transforms a potentially overwhelming situation into a manageable one with clear steps and known options. Take the time to review coverage before the rental—that preparation makes all the difference when accidents happen.