Quick Summary: Going without health insurance means facing high out-of-pocket costs for medical care, potential medical debt, delayed treatment, and limited preventive care access. While the federal tax penalty ended in 2018, some states still impose fees. Coverage options exist through the Health Insurance Marketplace, Medicaid, employer plans, and charity care programs.

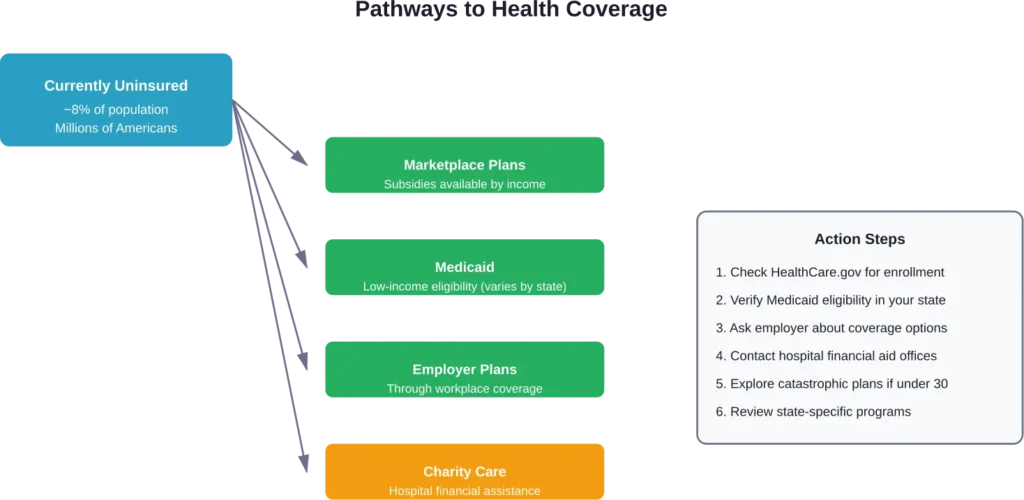

Millions of Americans face each year without health insurance. According to KFF, approximately 8% of the population remains uninsured, with numbers actually increasing in 2024 for the first time since 2019.

But what does that actually mean for someone without coverage?

The consequences extend beyond just missing doctor appointments. Financial risks, limited healthcare access, and potential long-term health impacts create a complex situation that affects individuals, families, and entire communities.

The Federal Tax Penalty Is Gone (But State Penalties Exist)

Here’s something many people don’t realize: the federal tax penalty for not having health insurance ended in 2018. The Tax Cuts and Jobs Act reduced the individual shared responsibility payment to zero starting with tax year 2019.

This means when filing federal tax returns, there’s no longer a penalty for being uninsured. No exemption forms needed either.

That said, some states implemented their own mandates. California, Connecticut, the District of Columbia, and Maryland have their own exemptions processes for residents without health coverage.

These state penalties are calculated when filing state tax returns. Some states may offer exemptions based on specific circumstances.

The Real Financial Impact of Being Uninsured

Forget tax penalties. The actual financial risk comes from medical bills.

Without insurance, healthcare providers charge full price. A simple emergency room visit can cost thousands of dollars. Surgery? Tens of thousands. Chronic condition management? An ongoing financial drain that never stops.

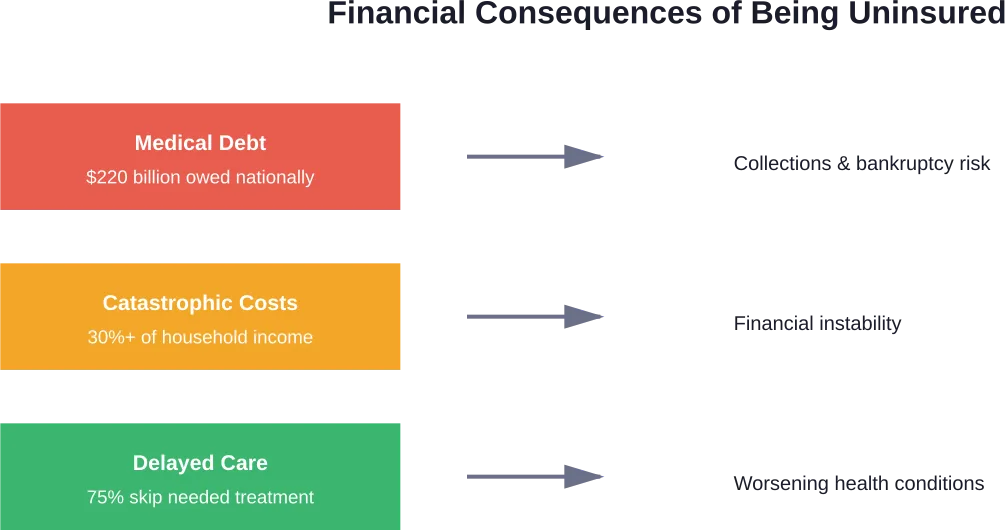

According to KFF, people in the United States owe at least $220 billion in medical debt. Approximately 14 million people carry over $1,000 in medical debt, and about 3 million owe more than $10,000.

The burden hits uninsured populations hardest. Research shows that catastrophic health expenditures—defined as out-of-pocket costs exceeding 30% of household income—affect hundreds of thousands of additional Americans when coverage isn’t available.

Limited Access to Healthcare Services

Money isn’t the only barrier. Access becomes severely restricted without insurance.

Many healthcare providers require insurance verification before scheduling appointments. Specialists often won’t see uninsured patients. Hospitals provide emergency care regardless of insurance status, but follow-up treatment? That’s another story.

KFF polling data reveals that about 36% of adults skipped or postponed needed healthcare in the past 12 months due to cost. Among uninsured adults under 65, that number jumps to 75%.

Three-quarters of uninsured people delaying care. Think about that.

This delay has consequences. Conditions that could be managed early become serious health crises. Preventive screenings that detect cancer, diabetes, or heart disease early? Often inaccessible to the uninsured population.

Preventive Care Goes Untapped

Most health plans provide 100% coverage for certain in-network preventive care services. Annual check-ups, vaccinations, cancer screenings, blood pressure monitoring—all designed to catch problems before they escalate.

Without insurance, these services carry price tags that discourage utilization. The uninsured tend to seek care only when symptoms become unbearable, missing the window when treatment is simplest and most effective.

Health Outcomes Suffer Without Coverage

The health impacts extend beyond inconvenience. Research from the Keck School of Medicine at USC, Boston University, and the University of Amsterdam examined what happens when Medicaid access gets reduced.

Their findings? Eliminating Medicaid expansion could drive millions to delay needed care and result in increased deaths. Low-income rural populations face disproportionate impact.

Research from Yale School of Public Health on uninsured communities in New Haven during the COVID-19 pandemic examined health impacts and barriers to healthcare access. Participants experienced moderate to severe changes in family income, stress levels, and access to social support.

Having no insurance doesn’t just affect individuals. Families and entire communities feel the ripple effects through reduced economic productivity, strained emergency services, and public health challenges.

What Coverage Options Exist for the Uninsured

Being uninsured doesn’t mean being without options. Several pathways to coverage exist, depending on circumstances.

| Coverage Option | Who Qualifies | Key Features |

|---|---|---|

| Health Insurance Marketplace | Anyone, especially those with moderate income | Premium tax credits and subsidies available based on income; open enrollment periods and special enrollment qualifying events |

| Medicaid | Low-income individuals and families (varies by state) | Free or very low-cost comprehensive coverage; eligibility expanded in many states under the ACA |

| Catastrophic Plans | Under 30 or hardship exemption holders | Low premiums, high deductibles; covers essential health benefits after deductible is met |

| Employer Coverage | Employees of applicable large employers | Shared premium costs; must meet affordability and minimum value standards |

| Charity Care Programs | Low-income individuals at qualifying hospitals | Free or reduced-fee care at hospitals accepting federal funding; varies by institution |

Health Insurance Marketplace

The Health Insurance Marketplace offers private plans with potential subsidies. Premium tax credits reduce monthly costs for those with income between 100% and 400% of the federal poverty level (though temporary expansions have modified these thresholds).

Open enrollment typically runs from November through mid-January, though special enrollment periods apply for qualifying life events like losing other coverage, moving, getting married, or having a baby.

Medicaid Eligibility

Medicaid provides comprehensive coverage for low-income populations. Eligibility varies significantly by state, particularly in states that chose not to expand Medicaid under the Affordable Care Act.

In expansion states, adults with income up to 138% of the federal poverty level generally qualify. Non-expansion states maintain more restrictive eligibility criteria, often leaving low-income adults without affordable options.

Hospital Financial Assistance

Hospitals that accept federal funding must provide certain amounts of free or reduced-fee care. Financial aid departments evaluate applications based on income and household size.

This isn’t insurance, but it can significantly reduce bills for eligible patients. Requirements and availability vary by institution.

The Cost of Healthcare Without Insurance

National health expenditures continue climbing. According to the CMS Office of the Actuary, health spending is projected to grow at an average of 5.1% over 2021-2030, with total health expenditures expected to reach nearly $6.8 trillion by 2030.

The U.S. far exceeds other wealthy nations in per capita health spending. Despite this massive investment, millions remain uninsured and healthcare represents a much larger share of the economy compared to peer nations.

For uninsured individuals, this translates to crushing bills. A single emergency can create debt that takes years to repay. Chronic conditions require ongoing treatment that becomes financially impossible to sustain.

Special Considerations for Specific Populations

People with Disabilities

Individuals with disabilities who don’t qualify for disability benefits still have Marketplace options. Applications evaluate eligibility for private plans with premium tax credits based on income.

Medicaid may also provide coverage depending on disability status and state regulations. Some states offer specialized programs beyond standard Medicaid expansion.

Young and Healthy Individuals

Many young adults question whether insurance makes sense when they’re healthy. The thinking goes: why pay premiums when medical needs seem minimal?

But unexpected accidents happen. Sports injuries, car crashes, sudden illnesses—none of these come with advance warning. A single emergency room visit and hospital stay can create tens of thousands in debt.

Catastrophic plans offer one solution: low monthly premiums with high deductibles. These cover essential health benefits after the deductible is met and provide protection against worst-case scenarios.

Frequently Asked Questions

No. The federal individual shared responsibility payment ended in 2018. However, California, Connecticut, the District of Columbia, and Maryland have their own exemptions processes for residents without coverage.

Hospital emergency departments cannot refuse emergency treatment regardless of insurance status or ability to pay. However, non-emergency care and follow-up treatment may require payment arrangements or proof of ability to pay.

Costs vary widely based on income, age, location, and plan type. Premium tax credits and subsidies can significantly reduce monthly premiums for eligible individuals. Check HealthCare.gov for current pricing specific to your situation.

Unpaid medical bills typically go to collections, which damages credit scores. Some providers may sue for payment. Many hospitals offer payment plans or financial assistance programs. Bankruptcy remains an option for overwhelming medical debt, though it carries serious long-term consequences.

Eligibility depends on income, household size, and state of residence. In Medicaid expansion states, adults with income up to 138% of the federal poverty level generally qualify. Non-expansion states have more restrictive criteria. Apply through HealthCare.gov or your state Medicaid office to determine eligibility.

Special enrollment periods allow Marketplace enrollment after qualifying life events such as losing other coverage, moving to a new coverage area, getting married or divorced, having or adopting a child, or experiencing certain other circumstances. Medicaid and CHIP accept applications year-round.

Catastrophic plans have lower monthly premiums but much higher deductibles. They’re available only to people under 30 or those with hardship exemptions. These plans cover three primary care visits per year and preventive services before the deductible, then cover essential health benefits after the deductible is met. Regular plans offer more comprehensive coverage with lower deductibles but higher premiums.

Taking Action on Health Coverage

Being uninsured creates real risks—financial, medical, and personal. Medical debt can accumulate quickly. Health conditions worsen without treatment. Preventive care that catches problems early remains inaccessible.

But options exist. The Health Insurance Marketplace, Medicaid programs, employer coverage, catastrophic plans, and charity care all provide pathways to coverage.

Start by visiting HealthCare.gov to explore Marketplace options and determine eligibility for subsidies. Check Medicaid eligibility in your state. If employed, review workplace coverage offerings. Contact hospital financial assistance departments about charity care programs.

Coverage matters. Not just for financial protection, but for health outcomes, peace of mind, and access to care when it’s needed most. The system remains complex and fragmented, but resources exist to help navigate it.

Take that first step. Check eligibility. Explore options. The cost of remaining uninsured—in dollars, health, and stress—far exceeds the effort required to find coverage.