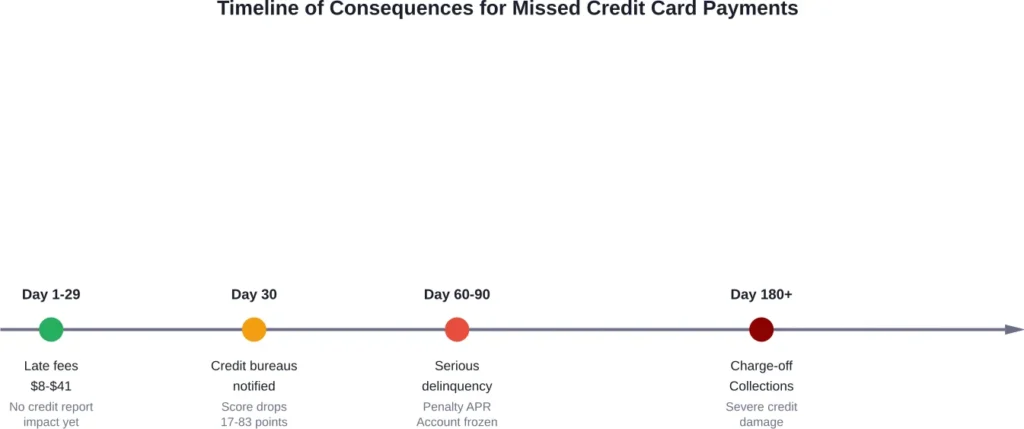

Quick Summary: Missing a credit card payment triggers a series of consequences that escalate over time. Within 30 days, you’ll face late fees (typically $8-$32 based on recent regulations) and potential interest rate increases. After 30 days, the missed payment gets reported to credit bureaus, damaging your credit score by 17-83 points depending on your current standing. Extended non-payment leads to account closure, collections, and lasting credit damage.

Life happens. Bills pile up, paychecks arrive late, or that payment notification gets buried in an overflowing inbox. Before you realize it, the credit card payment deadline has passed.

But what actually happens next? The consequences aren’t immediate disasters, but they do escalate the longer the payment remains outstanding.

Understanding the timeline and impacts can help minimize damage and inform better financial decisions moving forward.

The First 29 Days: Immediate Consequences

Here’s something most cardholders don’t realize: credit card companies typically provide a grace period before the serious penalties kick in. If the payment arrives within the first 30 days after the due date, the damage stays relatively contained.

Late Fees Hit Your Account

The first consequence comes fast. Most issuers charge a late fee as soon as the payment misses the due date, even by a single day.

According to the Consumer Financial Protection Bureau, credit card late fees cost American families more than $14 billion annually before recent regulatory changes. In March 2024, the CFPB finalized rules cutting excessive late fees by reducing the typical late fee from $32 to $8.

However, these regulations face ongoing legal challenges, and not all issuers have implemented the reduced fees yet. Many cards still charge the higher amounts.

Late fees follow a tiered structure. Under the CFPB’s 2024 rule, the typical late fee is capped at $8. However, card agreements may allow higher fees for repeat violations, and some issuers may still charge amounts up to $41 during the transition period before full rule implementation.

Interest Continues Accumulating

Beyond the late fee itself, interest charges continue piling up on the unpaid balance. Some issuers also revoke the grace period on new purchases, meaning interest starts accruing immediately on all transactions until the account returns to good standing.

This seemingly small change can significantly increase carrying costs over time.

No Credit Report Impact Yet

The silver lining? Creditors generally don’t report late payments to credit bureaus until they reach 30 days past due. This means a payment that’s five, ten, or even 25 days late won’t show up on credit reports from Equifax, Experian, or TransUnion.

This grace period offers a critical window to minimize long-term damage by bringing the account current before the 30-day mark.

After 30 Days: Credit Score Damage Begins

Once a payment hits 30 days late, the situation escalates significantly. This is when creditors typically report the delinquency to the three major credit bureaus.

Credit Score Takes a Hit

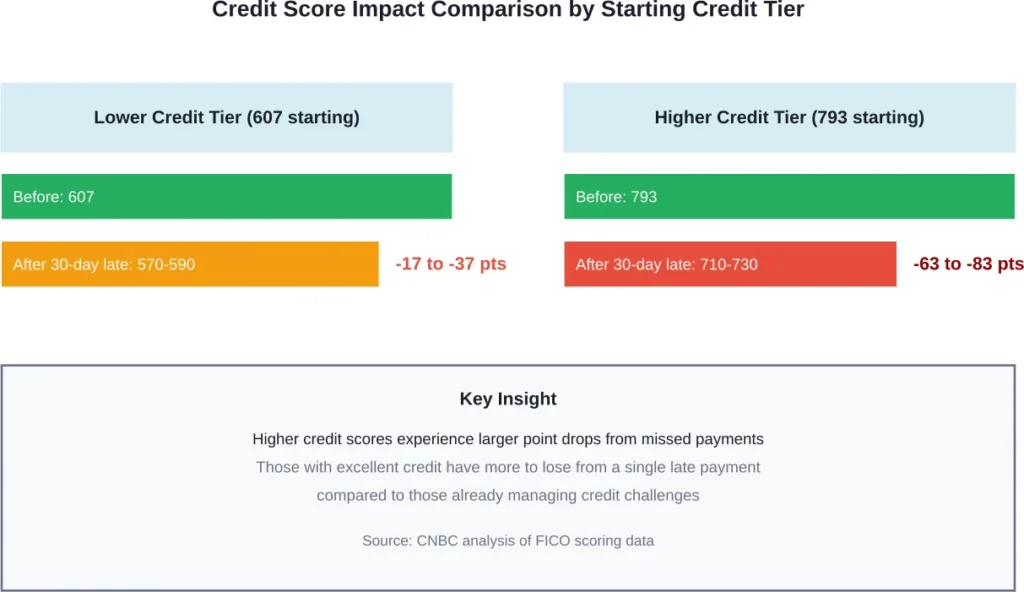

Payment history represents the single most influential factor in credit scoring models, accounting for a substantial portion of overall scores. A single 30-day late payment creates a negative mark that remains visible for seven years from the date of the missed payment.

According to CNBC’s analysis of FICO data, the actual score impact varies considerably based on the starting credit profile:

| Credit Profile | Starting Score | Score After 30-Day Late Payment | Total Drop |

|---|---|---|---|

| Lower credit tier | 607 | 570-590 | 17-37 points |

| Higher credit tier | 793 | 710-730 | 63-83 points |

Notice the pattern? Individuals with higher starting scores experience larger point drops. Someone with excellent credit has more to lose from a single misstep compared to someone already managing credit challenges.

Penalty APR May Apply

Many credit card agreements include penalty APR clauses that activate after missed payments. This penalty rate—sometimes reaching 29.99% or higher—replaces the standard purchase APR and dramatically increases interest charges.

Some issuers apply penalty rates after a single 30-day late payment. Others wait until 60 or 90 days. The specific terms live in the cardholder agreement fine print.

Penalty APRs can remain in effect indefinitely or until consecutive on-time payments demonstrate renewed reliability. Six months of consistent payments often triggers a review for rate reduction, but issuers aren’t required to restore the original rate.

60 to 90 Days Past Due: Serious Delinquency Territory

Missing two or three consecutive payment cycles moves the account into serious delinquency status. The consequences intensify.

Credit bureaus receive updated reports showing 60-day or 90-day late payment statuses. Each additional milestone creates a separate negative entry that further suppresses credit scores.

Card issuers may reduce credit limits or freeze the account entirely at this stage. The account becomes unusable for new purchases, though interest and fees continue accruing on existing balances.

Federal Reserve data shows credit card delinquency rates have risen to levels not observed since the Great Financial Crisis, with delinquencies reaching about 125 basis points above early 2023 levels as of Q3 2024. This trend reflects broader economic pressures affecting household budgets.

Beyond 120 Days: Charge-Offs and Collections

After approximately 180 days of non-payment, issuers typically charge off the account. This accounting term means the creditor considers the debt unlikely to be collected and writes it off as a loss.

What a Charge-Off Actually Means

Despite the name, a charge-off doesn’t eliminate the debt. Cardholders still legally owe the full amount, including accumulated interest and fees.

Charge-offs create one of the most damaging entries possible on credit reports. They signal extreme credit management failure and remain visible for seven years from the date of first delinquency.

Third-Party Collections Begin

Charged-off accounts often get sold to debt collection agencies or transferred to internal collections departments. Collection agencies purchase debts for pennies on the dollar and then pursue payment aggressively.

Once an account enters collections, consumers gain certain protections under the Fair Debt Collection Practices Act. According to FTC guidance, debt collectors cannot use abusive, unfair, or deceptive practices when attempting to collect debts.

Collection accounts add another negative entry to credit reports, compounding the damage from the original late payments and charge-off.

How to Recover From a Missed Payment

Okay, so the damage is done. What now?

Recovery strategies depend on how quickly the situation gets addressed and how far the delinquency has progressed.

Make Payment Immediately

The single most important step is bringing the account current as quickly as possible. Even if the payment has already been reported to credit bureaus, stopping additional late payment entries prevents further deterioration.

Contact the card issuer to confirm the total amount needed to restore the account to current status, including any accumulated late fees and interest.

Request Fee Waivers

Cardholders with otherwise strong payment histories sometimes successfully negotiate late fee waivers. Issuers aren’t obligated to waive fees, but many do as a customer retention gesture—especially for first-time offenses.

A simple phone call to customer service explaining the circumstances may result in fee reversal. Success rates vary by issuer and account history.

Consider Goodwill Adjustment Letters

For payments that have already been reported to credit bureaus, some consumers attempt goodwill adjustment requests. These written letters ask creditors to remove accurate but negative information as a courtesy.

Goodwill adjustments are entirely discretionary. Creditors have no obligation to remove accurately reported information. However, consumers with long positive histories occasionally receive favorable responses, particularly when unusual circumstances caused the missed payment.

Dispute Inaccurate Information

According to FTC consumer advice on credit report disputes, consumers have the right to dispute incomplete or inaccurate information on their credit reports. If a late payment was reported incorrectly—perhaps a payment that actually arrived on time—formal disputes through the credit bureaus can result in corrections.

This process applies only to genuinely inaccurate information. Disputes regarding accurate negative information typically get verified rather than removed.

Prevention Strategies That Actually Work

Prevention beats recovery every time. These strategies help avoid missed payments before they occur.

Automate Minimum Payments

Setting up automatic minimum payments ensures at least the baseline requirement gets paid each month. Most issuers offer autopay options tied directly to checking accounts.

While paying only minimums isn’t ideal for debt reduction, it prevents late payment reporting and associated fees.

Calendar Reminders and Alerts

Mobile banking apps and credit card platforms typically offer customizable payment alerts. Set reminders for several days before due dates to allow processing time.

Multiple reminder points—at seven days, three days, and one day before the due date—create redundancy that catches payments even during busy periods.

Align Due Dates With Income

Many issuers allow cardholders to request payment due date changes. Aligning due dates with paycheck deposits ensures funds are available when payments process.

This simple adjustment can eliminate timing mismatches that cause missed payments despite adequate income.

Maintain Emergency Reserves

Financial buffer accounts provide backup when unexpected expenses disrupt normal payment patterns. Even a modest reserve of $500-$1,000 can cover essential bills during temporary income interruptions.

When Financial Hardship Makes Payment Impossible

Sometimes missed payments aren’t about forgetfulness—they’re about insufficient funds. Economic pressures, job loss, medical expenses, or other financial shocks can make credit card payments genuinely unaffordable.

According to Federal Reserve data from November 2025, credit card delinquency rates increased significantly after peaking at all-time lows during the pandemic. Delinquencies reached levels not seen since the Great Financial Crisis, reflecting real household financial stress.

Contact the Issuer Proactively

When payments become unaffordable, proactive communication with creditors often yields better outcomes than avoiding contact. Many issuers offer hardship programs that temporarily reduce minimum payments, lower interest rates, or defer payments.

These programs vary by issuer but typically require documentation of financial hardship and commitment to a structured payment plan.

Explore Credit Counseling

Nonprofit credit counseling agencies help consumers develop debt management plans and negotiate with creditors. These services typically charge modest fees but can consolidate multiple credit card payments into single monthly amounts with reduced interest rates.

The Federal Trade Commission provides resources for identifying legitimate credit counseling organizations and avoiding predatory debt settlement scams.

Understand Bankruptcy as Last Resort

When debt becomes truly unmanageable, bankruptcy provides legal protection from creditors. This serious step has long-lasting consequences but sometimes represents the most viable path forward.

Bankruptcy should only be considered after exploring all other options and consulting with qualified legal counsel.

Frequently Asked Questions

A payment that’s only seven days late typically won’t impact credit scores. Creditors generally don’t report late payments to credit bureaus until they reach 30 days past due. However, late fees still apply even for payments just one day overdue, and the account needs to be brought current quickly to prevent escalation.

Late payments remain visible on credit reports for seven years from the date of the first missed payment. This applies whether the account was eventually brought current or charged off. The impact on credit scores diminishes over time, especially if subsequent payment history remains positive.

Accurately reported late payments generally cannot be removed unless they’re truly erroneous. Some consumers successfully request goodwill adjustments from creditors who voluntarily remove accurate negative information as a courtesy, but this is entirely discretionary. If a late payment was reported incorrectly, formal disputes through credit bureaus can result in corrections.

A late payment occurs when an account isn’t paid by its due date. A charge-off happens after approximately 180 days of non-payment when the creditor writes off the debt as unlikely to be collected. Both damage credit reports, but charge-offs represent more severe delinquency. Importantly, charge-offs don’t eliminate the debt—it remains legally owed and often gets transferred to collections.

Yes. Paying at least the minimum required payment by the due date prevents late payment reporting to credit bureaus and avoids late fees. However, paying only minimums while carrying balances results in substantial interest charges and extends repayment timelines significantly. Minimum payments prevent immediate damage but don’t represent optimal debt management.

Legal action becomes possible after accounts enter collections, though it’s not automatic. Creditors typically pursue legal remedies for larger balances when other collection efforts fail. Lawsuits can result in court judgments allowing wage garnishment or bank account levies. The Fair Debt Collection Practices Act provides certain consumer protections during collection processes.

Once accounts reach collections or charge-off status, some creditors accept settlement offers for less than the full balance owed. Settlement negotiations typically occur when creditors believe partial payment is more likely than full recovery. Settled accounts still appear on credit reports as “settled for less than full balance,” which remains negative but less damaging than continued non-payment.

Taking Control After a Missed Payment

Missing a credit card payment triggers escalating consequences, but the situation rarely becomes irreparable if addressed quickly. The 30-day threshold represents the critical dividing line between contained damage and lasting credit impact.

For payments still within the first 30 days, immediate action prevents credit bureau reporting. Beyond 30 days, focus shifts to damage control—minimizing additional late entries, negotiating penalty rate removal, and rebuilding payment history.

The path forward depends on whether the missed payment was an isolated oversight or symptomatic of broader financial challenges. One-time mistakes require different responses than chronic payment difficulties stemming from insufficient income or overwhelming debt loads.

Prevention through automation, alerts, and financial buffers offers the most reliable protection. But when prevention fails, quick response and honest assessment of underlying causes enable better outcomes than avoidance.

Take action today: review payment due dates, set up autopay for at least minimum amounts, and contact creditors immediately if upcoming payments look uncertain. Financial institutions respond better to proactive communication than after-the-fact excuses.