Quick Summary: Missing a mortgage payment triggers a series of consequences starting with late fees (typically 5-6% of the payment) after a 15-day grace period, followed by credit reporting at 30 days past due. The Consumer Financial Protection Bureau requires servicers to give homeowners options before foreclosure, which typically doesn’t begin until 120 days of missed payments. Contact your lender immediately if you anticipate missing a payment—forbearance, payment plans, and loan modifications can help you avoid foreclosure.

Missing a mortgage payment can happen to anyone. An unexpected medical bill, job loss, or simply a banking error can leave homeowners staring at a missed due date with mounting anxiety.

But here’s the thing—one missed payment doesn’t mean immediate foreclosure. Mortgage servicers follow specific timelines governed by federal regulations, and homeowners have more protections than many realize.

Understanding what happens after that first missed payment helps borrowers take the right steps quickly. The timeline matters. The actions taken in the first 30 days can determine whether this becomes a minor setback or a serious financial crisis.

The Grace Period: Your First Safety Net

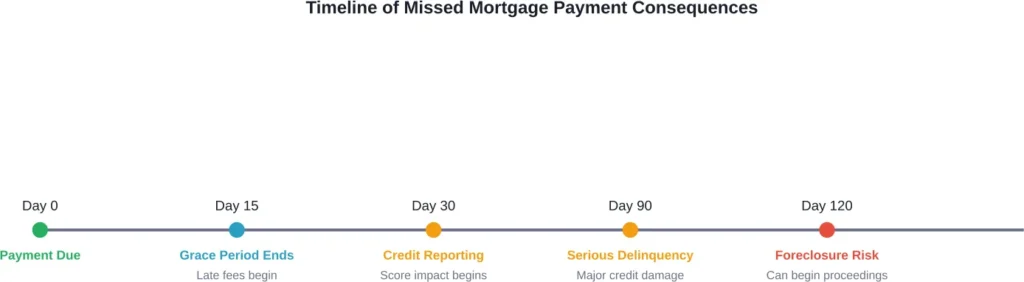

Most mortgage contracts include a grace period—typically 15 days after the due date. During this window, borrowers can make payments without facing late fees or credit reporting consequences.

If the mortgage payment is due on the first of the month, the grace period usually extends through the 15th. Payments received during this time are considered on-time, and the servicer won’t report anything negative to credit bureaus.

This grace period exists precisely for situations like autopay failures, mail delays, or short-term cash flow problems. It’s built into the loan agreement as a standard protection.

The grace period doesn’t require any special request or approval. It’s automatic. But once that 15-day window closes, the consequences begin to escalate.

What Happens After the Grace Period Ends

Once the grace period expires, mortgage servicers typically take several immediate actions that affect the borrower’s finances and credit standing.

Late Fees Kick In

The first financial consequence is the late fee. According to data from major lenders, late fees typically range from 5% to 6% of the monthly mortgage payment amount.

For a monthly payment of $2,200, a 5% late fee equals $110. That’s an additional cost on top of the already-missed payment, creating a larger financial burden for borrowers already struggling.

These fees are outlined in the mortgage contract and vary by lender. Some servicers charge a flat fee, while others use a percentage-based calculation. Either way, the cost adds up quickly if multiple payments are missed.

Lender Notifications Begin

Servicers will start contacting borrowers through multiple channels—phone calls, emails, and traditional mail. According to the Consumer Financial Protection Bureau’s mortgage servicing rules, servicers must maintain regular communication with borrowers facing payment difficulties.

These notifications aren’t just collection efforts. They’re also attempts to inform borrowers about available options and prevent the situation from worsening.

The frequency and intensity of these communications increase as more time passes without payment. What starts as a courtesy reminder can escalate to daily contact attempts.

Credit Reporting at 30 Days

This is where the credit damage begins. Once a payment is 30 days past due, mortgage servicers typically report the delinquency to the three major credit bureaus—Equifax, Experian, and TransUnion.

A 30-day late payment on a mortgage can drop credit scores significantly, sometimes by 50 to 100 points depending on the borrower’s overall credit profile. According to Consumer Financial Protection Bureau guidance, this information remains on credit reports for seven years from the date of delinquency.

The impact compounds if the delinquency continues. A 60-day late notation causes more damage than a 30-day late, and a 90-day late is worse still.

How Many Missed Payments Before Foreclosure Starts

Foreclosure doesn’t happen overnight. Federal regulations provide significant protection to homeowners facing financial difficulties.

According to the Consumer Financial Protection Bureau’s loss mitigation rules, mortgage servicers generally cannot begin foreclosure proceedings until a borrower is 120 days or more delinquent—that’s approximately four missed payments.

This 120-day rule exists to give borrowers time to explore alternatives and work with their servicer to find solutions. It’s a federally mandated protection that applies to most conventional mortgages.

But that doesn’t mean waiting until day 119 to take action is wise. The earlier borrowers engage with their servicer, the more options remain available.

Factors That Impact the Foreclosure Timeline

Several variables affect how quickly a foreclosure can proceed once it begins:

| Factor | Impact on Timeline |

|---|---|

| State Laws | Judicial foreclosure states require court proceedings, adding months to the process. Non-judicial states move faster. |

| Loan Type | FHA, VA, and USDA loans have additional protections and longer timelines than conventional mortgages. |

| Servicer Policies | Some servicers work more aggressively on loss mitigation than others, potentially delaying or preventing foreclosure. |

| Borrower Response | Active communication and loss mitigation applications can pause foreclosure proceedings. |

| Property Value | Homes with significant equity may see different servicer approaches than underwater mortgages. |

In judicial foreclosure states, the entire process from the first missed payment to actual eviction can take 18 months or longer. Non-judicial states can complete the process in as little as six months.

The variation is substantial. Community discussions show borrowers in Florida experiencing dramatically different timelines than those in Texas or California.

Options When Facing Mortgage Payment Difficulties

The Consumer Financial Protection Bureau emphasizes that borrowers shouldn’t face these challenges alone. Multiple options exist, and servicers are required to consider them before proceeding with foreclosure.

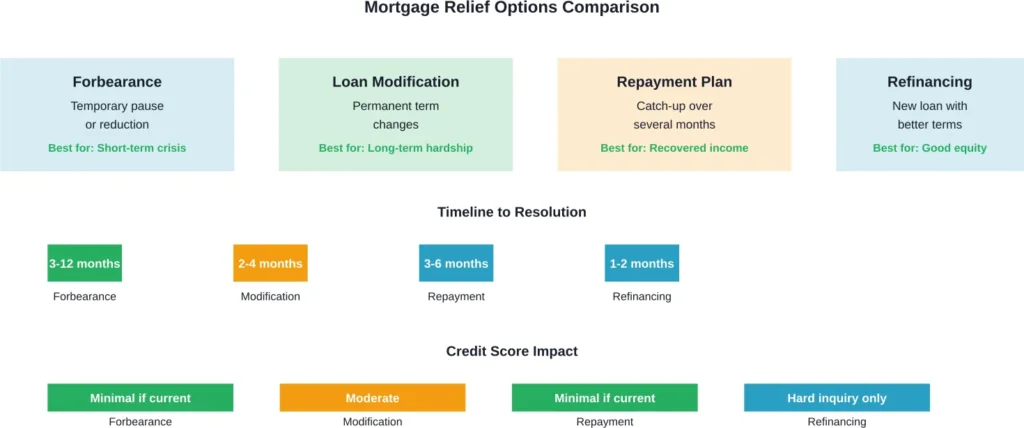

Forbearance: Temporary Payment Relief

Forbearance allows borrowers to temporarily pause or reduce mortgage payments during a financial hardship. According to CFPB guidance, servicers or lenders arrange for reduced or paused payments, with the full amount still owed and paid back later.

Forbearance works well for temporary situations—job loss with imminent rehiring, medical emergencies with defined recovery periods, or natural disaster damage with insurance payouts pending.

The missed payments don’t disappear. They’re added to the loan balance or repaid through a structured plan once the forbearance period ends. Borrowers need a clear plan for how they’ll handle the accumulated debt.

Loan Modification

Loan modifications permanently change the mortgage terms to make payments more affordable. This might include reducing the interest rate, extending the loan term, or converting from an adjustable-rate to a fixed-rate mortgage.

Modifications work better for borrowers facing long-term financial changes rather than temporary hardships. A permanent salary reduction, disability, or career change might warrant modification consideration.

Servicers evaluate modification requests based on the borrower’s current financial situation and ability to sustain modified payments. Documentation requirements are extensive—pay stubs, tax returns, bank statements, and hardship letters.

Repayment Plans

A repayment plan spreads the missed payments over several months, adding a portion to each regular payment until the delinquency is resolved.

If three payments were missed totaling $6,600, the servicer might agree to a six-month repayment plan adding $1,100 to each monthly payment. This brings the loan current without requiring a lump sum payment.

Repayment plans suit borrowers who’ve recovered from a temporary setback and can now afford slightly higher payments for a defined period.

Refinancing

For borrowers with significant equity and relatively good credit despite recent difficulties, refinancing might provide lower payments through better rates or extended terms.

This option becomes less viable once credit damage from missed payments has occurred. Timing matters—borrowers anticipating trouble should explore refinancing before missing payments, not after.

Steps to Take Immediately After Missing a Payment

Action beats inaction every time. The steps taken in the first days after a missed payment can prevent long-term consequences.

Contact Your Mortgage Servicer Right Away

According to CFPB guidance, borrowers should call their mortgage servicer immediately if they’ve missed a payment or anticipate missing one. The phone number appears on monthly mortgage statements.

This call accomplishes several things. It establishes communication, signals good faith effort to resolve the situation, and opens the door to discussing available options.

Servicers maintain dedicated loss mitigation departments specifically for these conversations. They’re not simply collection departments—they’re tasked with finding solutions that work for both parties.

Gather Financial Documentation

Most relief programs require documentation proving financial hardship and current financial status. Start collecting:

- Recent pay stubs or proof of income

- Bank statements from the past two months

- Tax returns from the past two years

- A detailed list of monthly expenses

- Documentation of the hardship (medical bills, layoff notice, etc.)

Having these documents ready accelerates the process. Servicers can’t evaluate modification or forbearance requests without understanding the complete financial picture.

Contact a HUD-Approved Housing Counselor

The Consumer Financial Protection Bureau recommends contacting a HUD-approved housing counseling agency to get free, expert assistance on avoiding foreclosure.

These counselors are trained specifically in mortgage issues and loss mitigation. They can review the situation, explain which options might work best, and guide borrowers through the process of working with their servicer.

The service is free. These agencies are government-funded precisely to help homeowners navigate financial difficulties. They have no stake in the outcome beyond helping borrowers find sustainable solutions.

Review Your Budget and Cut Expenses

While working on longer-term solutions, immediate budget adjustments can free up funds for mortgage payments. Every dollar matters when facing delinquency.

Prioritize housing payments above almost everything else. The home provides shelter and stability—protecting it should take precedence over discretionary spending and even some other debt payments.

Understanding Your Rights as a Borrower

Federal regulations provide substantial protections to mortgage borrowers facing difficulties. The CFPB’s mortgage servicing rules ensure that borrowers in trouble get a fair process to avoid foreclosure.

Servicers must evaluate complete loss mitigation applications before proceeding with foreclosure. They can’t foreclose while a borrower is being evaluated for or participating in a loss mitigation program.

Borrowers have the right to accurate information about their account, clear communication about available options, and a defined timeline for servicer responses to loss mitigation applications.

These protections prevent servicer surprises and runarounds—common complaints before the regulations took effect. The rules establish clear standards that servicers must follow.

Long-Term Credit Impact and Recovery

The credit damage from missed mortgage payments is real but not permanent. According to CFPB guidance, foreclosure information generally remains in credit reports for seven years from the date of the foreclosure.

But even with a foreclosure on record, it’s possible to qualify for a mortgage again. Federal Housing Administration loans, for example, may be available to borrowers as soon as two to three years after a foreclosure, depending on circumstances.

The key to recovery is demonstrating financial responsibility after the delinquency. On-time payments on all other accounts, reduced debt levels, and stable employment all contribute to credit score recovery.

Community discussions show borrowers recovering from mortgage delinquencies within 12 to 24 months when they address the underlying financial issues and maintain perfect payment records moving forward.

When to Consider Selling the Home

Sometimes the best financial decision is selling the home before foreclosure becomes inevitable. This option makes sense when:

- The home has positive equity that can be preserved through a sale

- Financial difficulties are permanent rather than temporary

- Monthly payments are simply unaffordable even with modification

- Relocation for employment or family reasons is already being considered

Selling voluntarily preserves credit better than foreclosure. It allows borrowers to walk away with equity rather than losing everything. And it provides a clean break rather than years of struggling with unaffordable payments.

For borrowers underwater on their mortgage, a short sale might be an option. The servicer agrees to accept less than the full loan balance, allowing the sale to proceed even when the home’s value has dropped below what’s owed.

Common Mistakes to Avoid

Certain actions can make a difficult situation worse. Avoiding these mistakes protects borrowers’ options and rights.

Ignoring Servicer Communications

The worst response to a missed payment is silence. Servicers can’t help borrowers who won’t communicate. Ignoring calls and letters doesn’t make the problem disappear—it eliminates the opportunity to find solutions before foreclosure proceedings begin.

Taking Out Additional Debt

Borrowing from credit cards, taking personal loans, or withdrawing retirement funds to make mortgage payments often just delays the inevitable while creating new financial problems.

These short-term fixes rarely address the underlying issue of unaffordable housing costs. They can leave borrowers in a worse position—still losing the home but now carrying additional high-interest debt.

Falling for Foreclosure Rescue Scams

Predatory companies target desperate homeowners with promises of guaranteed foreclosure prevention, often charging large upfront fees for services that HUD-approved counselors provide free.

Legitimate help is available at no cost through HUD-approved agencies. Any company demanding payment before providing assistance should raise immediate red flags.

Waiting Too Long to Take Action

The earlier borrowers address payment difficulties, the more options remain available. Waiting until four payments are missed and foreclosure is imminent drastically reduces the chances of finding a workable solution.

Act during the first missed payment, not the fourth.

Frequently Asked Questions

A single missed payment reported to credit bureaus can drop scores by 50 to 100 points depending on the overall credit profile. However, if the payment is made within the grace period (typically 15 days), no credit reporting occurs and there’s no score impact. The damage becomes significant once the payment is 30 days late and gets reported to the bureaus.

No. Federal regulations generally prohibit mortgage servicers from beginning foreclosure proceedings until a borrower is 120 days or more delinquent, which represents approximately four missed monthly payments. This protection gives borrowers time to explore loss mitigation options and work with their servicer to find alternatives to foreclosure.

Forbearance is a temporary pause or reduction in payments during a short-term financial hardship, with the full amount still owed and repaid later. A loan modification permanently changes the mortgage terms—such as interest rate, loan length, or payment structure—to make payments more affordable long-term. Forbearance suits temporary crises while modification addresses permanent financial changes.

If the account was current when forbearance began, the servicer typically reports the account as current during the forbearance period. However, if payments were already missed before forbearance started, those missed payments will appear on the credit report. The forbearance itself doesn’t damage credit, but any delinquency prior to entering forbearance does.

Qualification depends on the specific program, but most require documentation of financial hardship and proof of current income and expenses. Contact your mortgage servicer to discuss available options and requirements. HUD-approved housing counselors can also evaluate the situation and explain which programs might apply. Each servicer maintains different programs with varying eligibility criteria.

Refinancing becomes difficult after missed payments because the delinquency damages credit scores and creates a negative payment history. Most lenders require at least 12 months of on-time payments after resolving any delinquency before considering a refinance application. Borrowers anticipating payment difficulties should explore refinancing before missing payments, not after.

Foreclosure typically results in the loss of home equity. The lender sells the property to recover the loan balance, and while any excess proceeds theoretically go to the borrower, foreclosure sale prices are often lower than market value. Selling the home voluntarily before foreclosure allows borrowers to maximize equity recovery and avoid the severe credit damage of foreclosure.

Taking Control of the Situation

Missing a mortgage payment feels overwhelming, but it doesn’t have to end in disaster. The federal protections in place, the options servicers must offer, and the resources available through HUD-approved counselors all exist to help borrowers navigate these challenges.

The critical factors are speed and communication. Borrowers who act quickly, maintain open dialogue with their servicer, and seek professional guidance have significantly better outcomes than those who avoid the problem and hope it resolves itself.

One missed payment is a warning sign, not a death sentence for homeownership. Use it as a catalyst to address underlying financial issues, explore available assistance, and create a sustainable plan for keeping the home or exiting gracefully if that’s the better choice.

The 120-day window before foreclosure can begin provides time—use it wisely. Contact the servicer today, gather financial documentation, reach out to a HUD-approved counselor, and start exploring options. The sooner action begins, the better the outcome is likely to be.