Quick Summary: If you contribute more than the IRS limit to your 401(k), you must withdraw the excess by April 15 of the following year to avoid double taxation. The excess amount and any earnings will be taxed as income for the year contributed, and if not corrected, the earnings will be taxed again when distributed at retirement.

Contributing aggressively to a 401(k) is smart. But there’s a line you can’t cross without consequences.

The IRS sets strict annual limits on how much employees can defer to their 401(k) plans. According to the IRS, the limit for 2024 is $23,000, and for 2025, this rises to $23,500. The 2026 limit is $24,500. Those 50 and older can add catch-up contributions of $7,500 in 2025 and $8,000 in 2026. Individuals aged 60 to 63 can make “super” catch-up contributions of $11,250 in 2025 and 2026.

Cross these thresholds, and the IRS wants its money back. Sort of.

Understanding the 401(k) Contribution Limits

IRC Section 402(g) establishes the maximum amount of elective deferrals a participant may exclude from taxable income in a calendar year. These limits apply across all your employer-sponsored plans combined—401(k) plans, 403(b) arrangements, SIMPLE IRAs, and SAR-SEPs.

The contribution limits have increased over recent years to account for inflation adjustments:

| Year | Standard Limit | Catch-Up (50+) | Super Catch-Up (60-63) |

|---|---|---|---|

| 2024 | $23,000 | $7,500 | N/A |

| 2025 | $23,500 | $7,500 | $11,250 |

| 2026 | $24,500 | $8,000 | TBD |

These are employee deferral limits under IRC Section 402(g). They don’t include employer matching contributions, which fall under separate IRC Section 415(c) limits.

Real talk: Most people won’t accidentally exceed these limits. But it happens more often than you’d think, especially in specific situations.

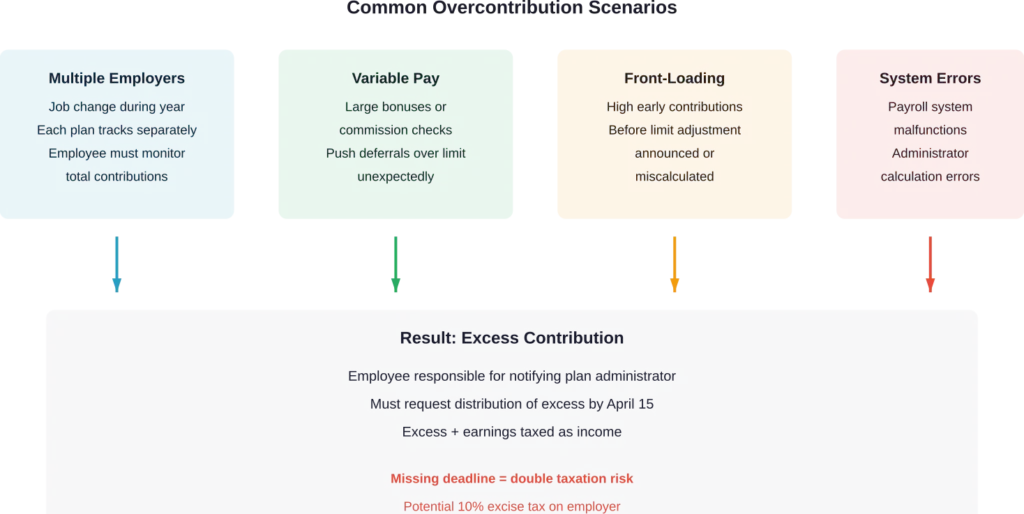

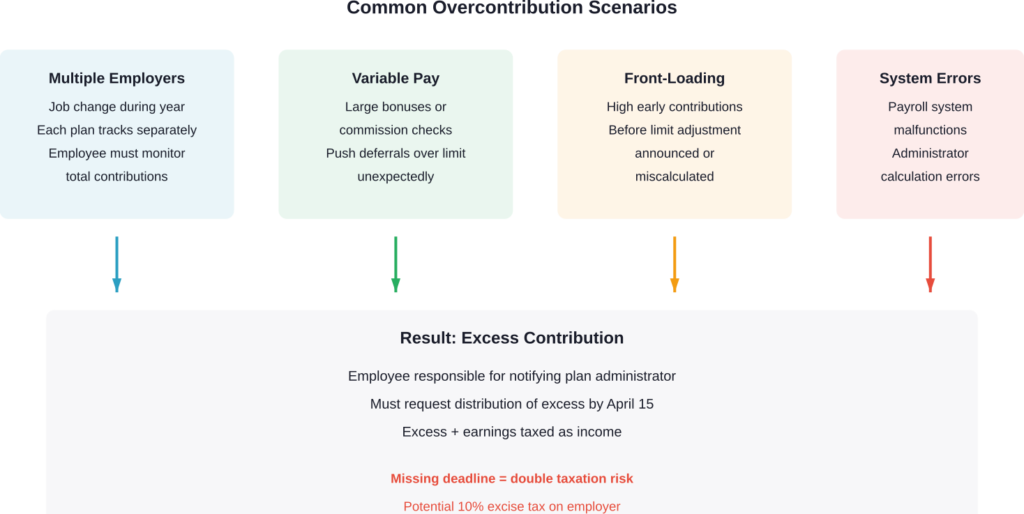

How Excess Contributions Happen

Several common scenarios where overcontributions occur:

Multiple Employer Plans

The 402(g) limit applies across all plans you participate in during a calendar year. If you change jobs mid-year and both employers sponsor 401(k) plans, you’re responsible for tracking your total deferrals.

Each employer’s payroll system only knows about contributions to their plan. They can’t see what you contributed elsewhere.

Fluctuating Pay and Bonus Structures

High earners with variable compensation—commissions, bonuses, stock compensation—sometimes miscalculate their annual deferrals. A deferral percentage that works most months might push you over the limit when a large bonus hits.

Mid-Year Limit Changes

When the IRS announces inflation adjustments, the new limits take effect January 1. Participants who front-load contributions early in the year based on the previous year’s limit might overcontribute if they don’t adjust quickly.

Plan Administrator Errors

Less common, but payroll systems occasionally malfunction or plan administrators miscalculate limits for catch-up contributions.

Tax Consequences of Excess Deferrals

Here’s the thing though—the IRS doesn’t just say “oops, take it back.” The tax treatment gets complicated fast.

If You Withdraw by April 15

According to the IRS, if an employee withdraws the excess deferral by April 15 of the year following the overcontribution, the withdrawn amount is taxable in the year it was originally contributed.

The plan must also distribute any earnings attributable to the excess deferral. Those earnings are taxable in the year withdrawn.

The excess amount won’t be reported again as part of distributions from the plan in later years. You avoid double taxation if you meet the deadline.

If You Miss the April 15 Deadline

This is where it gets expensive. The excess deferral remains in the plan and becomes part of your cost basis. But it’s still taxable income for the year contributed.

When you eventually take distributions in retirement, the IRS will tax those distributions again—including the excess that was already taxed. Double taxation.

Plus, the plan might face qualification issues. IRC Section 401(a)(30) requires plans to distribute excess deferrals. Failure to do so could jeopardize the plan’s tax-qualified status.

Excise Tax on the Employer

Under IRC Section 4979, there is imposed a tax equal to 10% of excess contributions for the employer’s taxable year. This creates compliance headaches for plan administrators.

| Scenario | Tax Treatment | Penalty Risk |

|---|---|---|

| Corrected by April 15 | Excess taxed once in contribution year; earnings taxed in withdrawal year | None |

| Corrected after April 15 | Excess taxed twice (contribution year + distribution); earnings taxed at distribution | Possible 10% employer excise tax |

| Never corrected | Double taxation at retirement; potential plan disqualification | 10% employer excise tax; plan compliance issues |

How to Fix Excess Contributions

The correction process isn’t automatic. Participants must take action.

Step 1: Identify the Excess

Check your W-2 Box 12 codes. Code D shows 401(k) deferrals, Code E shows 403(b) deferrals. Add them up across all employers.

Compare the total to the annual limit for that tax year. Any amount over the limit is an excess deferral.

Step 2: Notify the Plan Administrator

Contact your plan administrator in writing before March 1 of the year following the overcontribution. Some plans have specific forms for this request.

You’ll need to specify which plan should distribute the excess if you contributed to multiple plans. Strategically, you might choose the plan with lower earnings to minimize the taxable distribution.

Step 3: Request Distribution

The plan administrator must distribute the excess deferral plus attributable earnings by April 15 of the year following the overcontribution. They’ll calculate the earnings based on the plan’s allocation method—typically allocating gains and losses proportionally.

Step 4: Report Correctly on Tax Returns

The excess deferral is taxable income in the year contributed. It should appear on your W-2 for that year.

The distribution you receive (excess plus earnings) will generate a 1099-R for the year you receive it. Box 7 should show distribution code 8 or P, indicating it’s a corrective distribution.

Don’t double-count the excess on your tax return. The earnings portion is the only amount taxable in the year of distribution.

Special Situations and Considerations

Roth 401(k) Excess Contributions

The 402(g) limit applies to the combined total of traditional and Roth 401(k) deferrals. An excess in a Roth 401(k) follows the same correction rules.

But here’s a wrinkle: When excess Roth deferrals are distributed, they’re not taxable again since they were already taxed. Only the earnings are taxable.

Excess Catch-Up Contributions

Participants 50 and older have higher limits due to catch-up provisions. Make sure the plan administrator correctly applies these limits. Some payroll systems automatically stop all contributions once the base limit is reached, preventing legitimate catch-up deferrals.

Multiple Plan Participation

When excess deferrals occur across multiple unrelated employers, the participant chooses which plan should make the corrective distribution. This decision can have strategic tax implications based on which plan had better or worse investment performance.

Prevention Strategies

To avoid this situation, set your deferral as a specific dollar amount per paycheck rather than a percentage if your pay fluctuates. Divide the annual limit by your number of pay periods and stick to that amount.

Monitor your contributions throughout the year, especially if you change jobs. Most plan websites show year-to-date contribution totals.

Communicate with your new employer’s HR department about contributions you’ve already made to a previous employer’s plan. While they can’t enforce the limit across employers, good payroll systems can help you set appropriate deferral rates.

If you’re approaching the limit late in the year, reduce or suspend your deferrals to avoid overshooting.

Frequently Asked Questions

The employee deferral limit for 2026 is $24,500. Participants aged 50 and older can contribute an additional $8,000 in catch-up contributions, for a total of $32,500. These limits apply to the combined total across all 401(k), 403(b), SIMPLE IRA, and SAR-SEP plans.

Check your W-2 Box 12 for code D (401(k) deferrals) or code E (403(b) deferrals). Add up these amounts across all employers for the calendar year. If the total exceeds the annual limit, you’ve made an excess deferral. Your year-end pay stub or plan account statement will also show total contributions.

The excess amount will be taxed twice—once in the year contributed and again when distributed at retirement. Any earnings on the excess will also be taxed at retirement. The employer may face a 10% excise tax on the excess contributions, and the plan could face qualification issues with the IRS.

Yes, the same correction process applies to Roth 401(k) excess deferrals. Since Roth contributions are made with after-tax dollars, the excess amount itself isn’t taxed again when distributed. However, any earnings attributable to the excess are taxable in the year you receive the corrective distribution.

The 402(g) limit applies to your total deferrals across all plans. You’re responsible for monitoring this total and notifying one of the plan administrators to request a corrective distribution. You can choose which plan should distribute the excess, which may affect the taxable earnings amount based on each plan’s investment performance.

There’s no direct penalty to the participant if the excess is corrected by April 15 of the following year. However, if you miss this deadline, you face double taxation on the excess amount. The employer may face a 10% excise tax on excess contributions that aren’t timely corrected under IRC Section 4979.

You must notify your plan administrator by March 1 of the year following the overcontribution. The plan administrator must then distribute the excess deferral plus attributable earnings by April 15 of that same year. Meeting this April 15 deadline is critical to avoid double taxation.

Conclusion

Overcontributing to a 401(k) isn’t the end of the world, but it requires prompt action. The IRS provides a clear correction path through timely distribution of excess deferrals.

The April 15 deadline isn’t negotiable. Miss it, and the tax consequences compound quickly—double taxation on the excess, taxes on earnings at retirement, and potential excise taxes for the employer.

Monitor your contributions throughout the year, especially if you change jobs or have variable pay. Check your year-end statements and W-2 forms carefully. If you spot an excess, contact your plan administrator immediately.

The rules exist for good reason—maintaining the tax-favored status of retirement plans while ensuring fairness across income levels. Stay within the limits, and if you cross them, fix it fast.