Quick Summary: If you total a leased car, your insurance pays the leasing company up to the vehicle’s actual cash value. You remain responsible for any gap between what insurance pays and what you owe on the lease unless you have gap insurance. The leasing company still requires full payment of the remaining lease balance, and you’ll need to continue making payments until the claim settles.

Leasing a car offers flexibility and lower monthly payments, but what happens when that leased vehicle gets totaled in an accident? The situation differs dramatically from owning a car outright.

Unlike a financed vehicle where you’re building equity, a leased car never belongs to you. This creates unique complications when the vehicle becomes a total loss. The financial and legal responsibilities don’t simply disappear because the car is destroyed.

Understanding these responsibilities before an accident happens can save thousands of dollars and prevent serious financial headaches.

How Car Leases Actually Work

A car lease is essentially a long-term rental agreement with the dealership or leasing company. Rather than purchasing the vehicle, the arrangement allows use of the car for a specified period—typically two to four years.

Monthly lease payments cover the vehicle’s depreciation during the lease term, not the full purchase price. This explains why lease payments tend to be lower than financing payments for the same vehicle.

The leasing company retains ownership throughout the entire lease period. At the end, the option exists to either return the vehicle, purchase it for the predetermined residual value, or lease another car.

According to the Consumer Financial Protection Bureau’s Regulation M, lessors must disclose all terms clearly, including early termination fees, excess mileage charges, and responsibilities in the event of vehicle damage or loss.

The Difference Between Leased and Owned Vehicles

Ownership status creates the fundamental difference when an accident occurs. With a purchased car—even one with an outstanding loan—equity exists in the vehicle. The owner keeps any insurance payout after the lender receives their portion.

Leased vehicles provide no equity whatsoever. Every dollar of the insurance settlement goes directly to the leasing company, not the driver.

Another critical difference involves insurance requirements. The Federal Trade Commission notes that leasing companies typically require more comprehensive coverage than state minimums, including collision and comprehensive insurance with lower deductibles.

Here’s the ownership structure comparison:

| Aspect | Leased Vehicle | Owned Vehicle |

|---|---|---|

| Legal Owner | Leasing company | Buyer (or lender until paid off) |

| Equity | None | Increases with payments |

| Insurance Payout Recipient | Leasing company | Owner (after lender payoff) |

| Monthly Payment Covers | Depreciation only | Principal and interest |

| End-of-Term Options | Return, buy, or lease new | Keep or sell |

What Does “Totaled” Actually Mean?

Insurance companies declare a vehicle totaled when repair costs exceed a certain percentage of the car’s actual cash value. This threshold varies by state and insurer but typically falls between 70% and 80%.

Actual cash value represents what the vehicle is worth at the time of the accident, accounting for depreciation. This amount is almost always less than what’s still owed on a lease, especially in the early years.

A total loss determination doesn’t require complete destruction. Even moderate damage can total a vehicle if repair costs approach the vehicle’s current market value.

The Insurance Information Institute explains that new vehicles can lose 20% or more of their value in the first year alone. This rapid depreciation creates the gap between lease payoff amounts and insurance settlements.

The Insurance Claims Process for a Totaled Lease

When a leased vehicle is totaled, the insurance claim follows a specific sequence. First, the at-fault party’s insurance should cover the loss. If the driver of the leased vehicle caused the accident, their own collision coverage applies.

The insurance company conducts an investigation to determine the vehicle’s actual cash value. They’ll review comparable vehicles in the local market, consider mileage, condition, and any modifications or damage that existed before the accident.

Once the value is established, the insurer issues payment directly to the leasing company as the legal owner. This happens regardless of who was driving or who caused the accident.

But here’s where it gets complicated. The settlement amount rarely covers the full remaining lease balance.

Who Pays the Remaining Lease Balance?

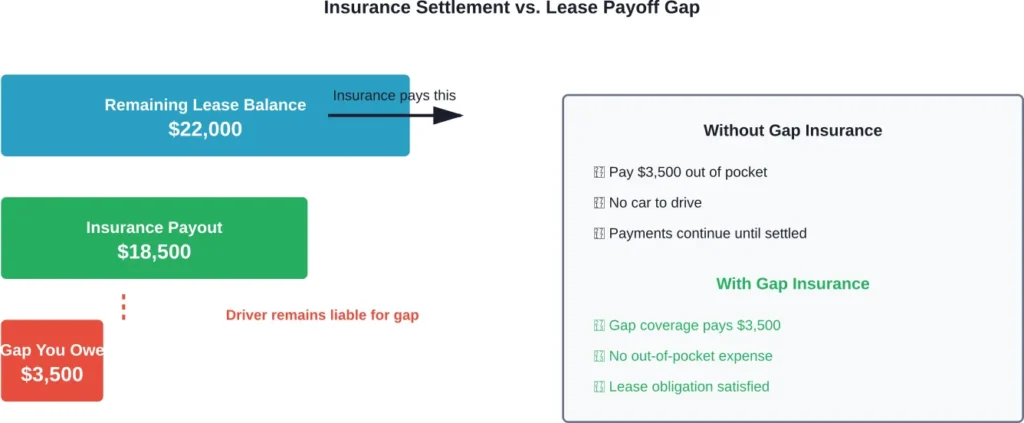

The driver remains responsible for the entire remaining lease balance. This obligation doesn’t change because the vehicle is destroyed.

If the insurance payout is $18,500 but the lease payoff is $22,000, someone needs to pay that $3,500 difference. Without gap insurance, that burden falls entirely on the person who leased the vehicle.

The leasing company will continue to expect monthly payments until the balance is settled in full. Missing these payments can damage credit scores and potentially result in collections or legal action.

Many drivers don’t realize this until after an accident occurs. The assumption that insurance “takes care of everything” proves costly and incorrect.

Gap Insurance: The Critical Protection

Gap insurance—or Guaranteed Asset Protection—covers the difference between the insurance payout and the remaining lease or loan balance. The Insurance Information Institute identifies this coverage as particularly important for leased vehicles.

In the event of an accident where the vehicle is badly damaged or totaled, gap insurance covers the difference between what the vehicle is currently worth and the amount actually owed on it.

Most leasing companies either require gap insurance or build it into the lease agreement. However, not all leases include this coverage automatically, making it essential to verify before driving off the lot.

Gap coverage can be purchased through the leasing company, the insurance provider, or the dealership. Costs vary, but purchasing through an insurance company may offer better rates than dealer financing options.

When Gap Insurance Applies

Gap insurance activates only when a vehicle is declared a total loss or stolen and not recovered. It won’t cover mechanical repairs, regular wear and tear, or accidents where the vehicle can be repaired.

The coverage also won’t pay for lease penalties like excess mileage charges, security deposit losses, or fees for excessive wear and damage that existed before the total loss event.

Understanding these limitations prevents surprises during the claims process.

Immediate Steps After a Leased Car Accident

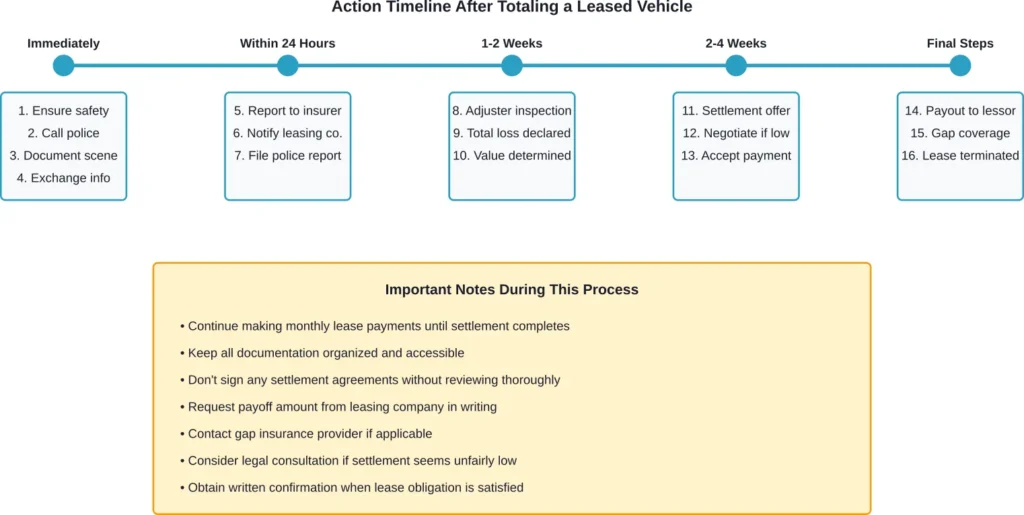

Taking the right actions immediately after an accident protects both legal and financial interests. First, ensure everyone’s safety and call law enforcement if there are injuries or significant property damage.

Document everything at the scene. Take photos of all vehicles involved, the surrounding area, road conditions, traffic signs, and any visible damage. Get contact information from witnesses and the other driver, including insurance details.

Report the accident to the insurance company within 24 hours. Provide basic information about the accident location and the identities of everyone involved, but avoid admitting fault or making detailed statements before consulting with the insurance adjuster.

Contact the leasing company promptly as well. The lease agreement likely requires notification of accidents within a specific timeframe, and failure to report can constitute a lease violation.

What If the Accident Wasn’t Your Fault?

When the other driver causes the accident, their liability insurance should cover the damages. However, the process still involves the leasing company as the legal owner receiving payment.

The at-fault driver’s insurance pays the leasing company for the vehicle’s actual cash value. If that amount doesn’t cover the remaining lease balance, gap insurance still applies—assuming the coverage exists.

If the at-fault driver lacks insurance or carries insufficient coverage, uninsured/underinsured motorist coverage on the lease holder’s policy may provide protection. This underscores why comprehensive coverage matters even when not at fault.

One advantage in not-at-fault scenarios: the potential to recover the deductible from the other driver’s insurance. This doesn’t happen automatically but can be pursued through the claims process or small claims court.

Leasing Company Requirements and Expectations

Leasing companies impose specific insurance requirements precisely because they own the vehicle. According to the Insurance Information Institute, lessors typically require collision and comprehensive coverage regardless of state minimum requirements.

These requirements usually include lower deductibles than drivers might choose otherwise—often lower deductibles than standard policies. The leasing company wants to ensure adequate compensation if the vehicle is damaged or destroyed.

The lease agreement also specifies procedures for accident reporting and repair authorization. Violating these terms can result in additional fees or penalties beyond the financial responsibility for the vehicle itself.

Most leasing companies include gap insurance in their lease agreements, but some offer it as an optional add-on. Reading the lease contract carefully before signing prevents costly assumptions later.

Financial Responsibilities Beyond Insurance

Even with comprehensive coverage and gap insurance, certain costs may still fall on the driver. Deductibles must be paid out of pocket before insurance coverage applies.

If the accident occurred while violating lease terms—such as allowing an unauthorized driver or using the vehicle for commercial purposes—the leasing company might deny gap coverage or pursue additional damages.

Outstanding fees from the lease agreement don’t disappear either. Excess mileage charges calculated up to the accident date, disposition fees, or penalties for wear and tear beyond normal use may still be owed.

The lease agreement remains a binding contract. Total loss of the vehicle terminates the use portion but not necessarily all financial obligations.

Disputing a Low Insurance Settlement

Insurance companies sometimes offer settlements below the vehicle’s fair market value. Drivers have the right to challenge these valuations.

Gather evidence of comparable vehicles in the local market. Check online listings, dealership prices, and valuation tools to demonstrate the settlement offer is inadequate.

Present this information to the insurance adjuster with a formal request for reconsideration. Many insurers will adjust their offer when faced with solid evidence.

If the insurance company refuses to budge and the difference is substantial, consulting with an attorney specializing in insurance claims may be worthwhile. Legal representation can pressure insurers to make fair offers.

Preventing Financial Loss on Future Leases

Several strategies minimize financial risk when leasing vehicles. First, always secure gap insurance before driving the vehicle. If the dealer’s gap insurance seems expensive, check with the auto insurance provider for potentially better rates.

Consider making a larger down payment to reduce the gap between the lease balance and the vehicle’s value. This approach reduces monthly payments and decreases exposure if the car is totaled early in the lease term.

Choose shorter lease terms when possible. Three-year leases create less depreciation gap than four or five-year agreements.

Maintain comprehensive documentation of the vehicle’s condition, maintenance records, and any improvements. This evidence supports higher valuations during insurance settlements.

| Protection Strategy | How It Helps | Typical Cost |

|---|---|---|

| Gap Insurance (via insurer) | Covers lease balance shortfall | $20-60 per year |

| Gap Insurance (via dealer) | Covers lease balance shortfall | $400-700 added to lease |

| Higher Down Payment | Reduces initial negative equity | Varies by vehicle |

| Lower Deductibles | Reduces out-of-pocket costs | $50-150 per year increase |

| Shorter Lease Term | Less depreciation exposure | Higher monthly payments |

State-Specific Considerations

Insurance requirements and total loss procedures vary by state. Some states use different thresholds for declaring vehicles totaled, affecting when gap coverage applies.

Certain states require insurance companies to include sales tax in total loss valuations, while others don’t. This difference can impact whether the insurance settlement covers the full lease payoff.

State laws also govern how quickly insurance companies must settle claims and issue payments. These timelines affect how long drivers must continue making lease payments while waiting for resolution.

Check state-specific requirements with the insurance department or a local attorney familiar with auto insurance law.

Common Mistakes to Avoid

Several errors compound the financial impact of totaling a leased vehicle. One frequent mistake is stopping lease payments immediately after the accident. Payments must continue until the lease is officially terminated through the settlement process.

Another error is accepting the first insurance settlement offer without verification. Always compare the offer against actual market data for similar vehicles.

Some drivers fail to notify the leasing company promptly, violating lease terms and potentially voiding gap coverage. Others make the mistake of authorizing repairs before getting approval from both the insurance company and the leasing company.

Finally, many drivers don’t read their lease agreement until after an accident. Understanding obligations beforehand prevents costly surprises.

Frequently Asked Questions

Yes, lease payments must continue until the insurance settlement is processed and the lease is officially terminated. This process typically takes several weeks to complete. Stopping payments can damage credit and result in late fees or default penalties.

Generally speaking, no. The insurance payout goes directly to the leasing company as the vehicle’s legal owner. Without gap insurance, drivers actually owe additional money if the settlement doesn’t cover the remaining lease balance. Refunds only occur in rare circumstances where the insurance payout exceeds the total lease payoff and all associated fees.

Without gap insurance, drivers remain personally responsible for the difference between the insurance settlement and the remaining lease balance. This amount can range from a few hundred to several thousand dollars depending on when the accident occurred in the lease term. The leasing company will pursue collection of this debt through the same methods used for any unpaid financial obligation.

This depends on the financial situation and credit standing. If gap insurance covers the entire balance and credit remains good, leasing another vehicle is possible. However, if money is still owed on the totaled lease, that debt affects credit and may prevent approval for a new lease until resolved.

Insurance companies pay the actual cash value of the vehicle at the time of the total loss, not the lease buyout or payoff amount. The actual cash value accounts for depreciation and represents what the vehicle would sell for in the current market. This amount is typically lower than the lease payoff, which is why gap insurance exists.

If the at-fault driver is uninsured, the uninsured motorist coverage on the lease holder’s policy should apply. This coverage works similarly to collision coverage, paying for the vehicle damage. The driver’s own gap insurance would still cover any shortfall between the payout and lease balance. Without uninsured motorist coverage, recovering the loss becomes significantly more difficult.

The process typically takes two to six weeks from the accident date to final settlement. Timeline factors include inspection scheduling, value determination, negotiation, and payment processing. During this entire period, the lease holder must continue making monthly payments. Delays can occur if disputes arise over the vehicle’s valuation or if multiple parties are involved in the accident.

Moving Forward After a Total Loss

Totaling a leased car creates immediate financial and logistical challenges. Understanding the responsibilities beforehand and maintaining proper insurance coverage makes the situation manageable rather than catastrophic.

Gap insurance transforms a potentially devastating financial loss into a resolved insurance claim. The relatively small cost provides enormous protection against the depreciation gap that affects virtually all leased vehicles.

When an accident occurs, prompt action, thorough documentation, and clear communication with all parties—insurance companies, leasing companies, and other drivers—protects both legal rights and financial interests.

The lease agreement remains binding even when the vehicle is destroyed. Meeting those obligations, understanding the insurance settlement process, and knowing when to challenge inadequate offers prevents the situation from becoming worse.

Drivers considering leasing should factor these potential scenarios into their decision-making process. The lower monthly payments that make leasing attractive come with specific responsibilities that don’t apply to purchased vehicles.

With proper preparation and coverage, totaling a leased car becomes a manageable insurance claim rather than a financial disaster. Take time now to review insurance policies, verify gap coverage, and understand lease agreement terms before an accident makes that information urgently necessary.