Quick Summary: Not using a credit card can lead to account closure or credit limit reduction by the issuer. These actions may increase your credit utilization ratio and potentially lower your credit score. Keeping cards active with occasional small purchases helps maintain account status and credit health.

That credit card sitting unused in your wallet might seem harmless. After all, if it’s not being used, it can’t rack up debt, right?

But here’s the thing—credit card issuers don’t see it that way. They view inactive accounts as unprofitable liabilities, and they have the power to take actions that could impact your financial health.

Understanding what happens when credit cards go unused helps cardholders make informed decisions about their credit management strategies.

What Happens When You Don’t Use Your Credit Card

Credit card companies monitor account activity closely. When a card remains dormant for an extended period, issuers typically respond in one of two ways.

The most common consequence is account closure. According to Experian, credit card issuers may close accounts that show no activity after a certain timeframe. This period varies by issuer, with most companies reviewing inactive accounts at the six to 12-month mark.

Alternatively, issuers might reduce the credit limit on inactive accounts instead of closing them entirely. This approach allows them to reduce their risk exposure while keeping the account technically open.

Neither action requires advance notification in many cases. Cardholders often discover their account has been closed only when they attempt to use the card or check their credit report.

How Card Issuers Define Inactivity

What counts as inactivity? Generally speaking, any account with zero transactions over several consecutive billing cycles falls into this category.

Some issuers consider an account inactive after just six months without purchases. Others may extend this timeline to 12 or even 24 months before taking action.

The specific inactivity threshold isn’t always disclosed in cardholder agreements. Each financial institution sets its own policies based on portfolio management strategies and risk assessment.

The Credit Score Impact of Unused Credit Cards

When an issuer closes an inactive credit card or reduces its limit, the ripple effects can reach your credit score. Two key credit scoring factors come into play.

Credit Utilization Ratio Changes

The credit utilization ratio measures how much credit is being used compared to the total available credit. The Consumer Financial Protection Bureau recommends keeping this ratio below 30%.

Here’s where account closure creates problems. When a card gets closed, its credit limit disappears from the calculation, potentially driving up the utilization ratio even if spending habits haven’t changed.

Consider an example: Three credit cards with limits of $2,000, $3,000, and $5,000 provide $10,000 in total available credit. With a $1,500 balance on one card, the utilization ratio sits at 15%.

But if the $3,000 limit card gets closed, total available credit drops to $7,000. That same $1,500 balance now represents 21.4% utilization—a significant jump that credit scoring models notice.

Credit History Length Considerations

Credit age matters for scoring purposes. Older accounts demonstrate a longer track record of credit management.

According to Experian, closed accounts that aren’t past due generally remain on credit reports for up to 10 years. During this time, they continue contributing to credit history length calculations.

However, once that closed account eventually falls off the report, average account age may decrease if the closed card was one of the oldest accounts.

Will You Be Charged for Not Using Your Credit Card?

The good news? Issuers don’t charge inactivity fees.

Federal Reserve regulations ban credit card companies from charging inactivity fees, such as fees based on the consumer’s failure to use the account to make new purchases. This protection was implemented as part of the Credit Card Accountability Responsibility and Disclosure (CARD) Act of 2009.

That said, cardholders still need to watch for annual fees. These charges apply whether the card sees regular use or sits dormant. An unused card with a $95 annual fee still generates that charge each year.

For cards with annual fees, the cost-benefit analysis becomes straightforward: If the card isn’t being used enough to justify the fee, closure might make financial sense despite the potential credit score impact.

How Long Can a Credit Card Remain Inactive?

Inactivity timelines vary significantly across issuers. According to Experian, inactivity is defined as accounts with no balance for the last six to 12 months, and inactive accounts may be closed by lenders after a certain period of time.

Some major issuers wait longer—up to 24 months in certain cases—before taking action. Premium cards with annual fees sometimes receive more lenient treatment since they generate revenue even without transaction activity.

The type of card can influence these decisions as well. Store credit cards and co-branded cards may have different inactivity thresholds than general-purpose cards.

No universal standard exists. Each issuer applies its own risk management criteria when determining which inactive accounts to close or modify.

Should You Close an Unused Credit Card Yourself?

According to the Consumer Financial Protection Bureau (CFPB), closing a credit card may be a good financial decision in certain situations despite potential credit impacts.

Valid reasons to close an unused card include:

- The card charges an annual fee that outweighs any benefits

- Managing multiple cards creates organizational challenges

- The temptation to overspend remains a concern

- The card offers poor terms compared to alternatives

Before closing any card, evaluate the potential credit utilization impact. If other cards have sufficient available credit to keep utilization ratios low, closure may have minimal effect.

Cards without annual fees, however, rarely benefit from closure. Keeping them open and occasionally active typically provides more credit score benefit than closing them.

Smart Strategies to Keep Credit Cards Active

Maintaining account activity doesn’t require significant spending. Small, strategic purchases can keep cards in good standing while avoiding debt accumulation.

Effective Activation Tactics

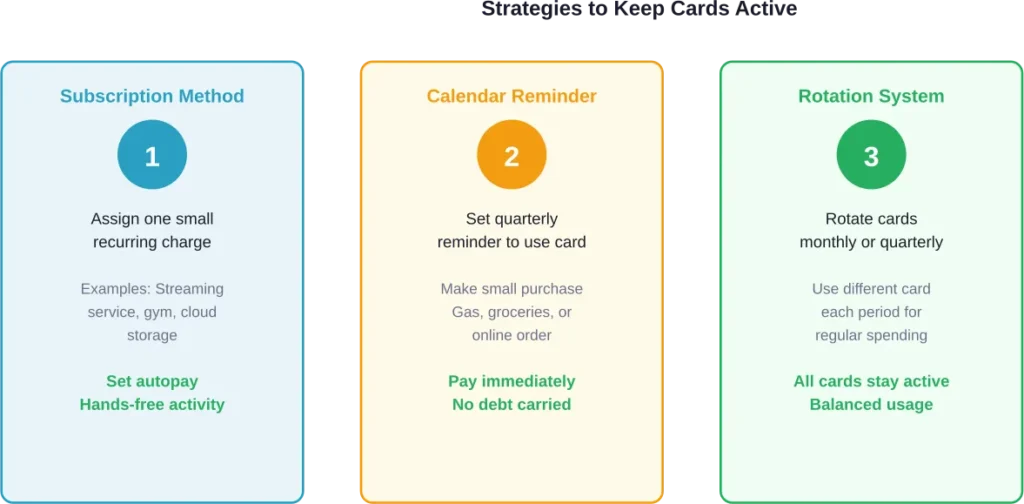

The subscription method works particularly well. Assign one small recurring charge to each card—a streaming service, gym membership, or cloud storage subscription. Set up automatic payments to handle the balance each month.

This approach requires zero ongoing effort once established. The card shows regular activity, and autopay prevents missed payments or interest charges.

Alternatively, set calendar reminders to use each card quarterly. Make a small purchase, pay it off immediately, and the account remains active without accumulating debt.

Some cardholders rotate their cards on a schedule, using different cards for regular spending each month or quarter. This strategy distributes activity across all accounts naturally.

What Counts as Activity?

Any transaction posted to the account typically counts as activity for issuer purposes. This includes:

- Purchases of any amount

- Recurring subscription charges

- Balance transfers or cash advances

Even a $5 purchase every few months usually suffices to keep an account in active status.

Monitoring Your Credit Card Accounts

Regular account monitoring helps catch issues before they escalate. Check all credit card accounts monthly, even those rarely used.

Look for:

- Unauthorized charges that might indicate fraud

- Annual fee posting dates

- Changes to terms and conditions

- Communications from the issuer about account status

Setting up account alerts provides another layer of oversight. Most issuers offer notifications for purchases over certain amounts, payment due dates, and unusual activity patterns.

Annual credit report reviews reveal whether any accounts have been closed without notification. The three major credit bureaus—Experian, Equifax, and TransUnion—each provide free annual credit reports that show all open and closed accounts.

Frequently Asked Questions

Most issuers review inactive accounts after six to 12 months of no activity. Some wait up to 24 months before closing accounts. The specific timeline varies by issuer and card type, with no universal industry standard.

It depends on the situation. According to consumerfinance.gov, closing an existing card can increase your credit utilization ratio and lower your score. Additionally, closing an old account may impact the length of your credit history. The effect varies based on overall credit profile and remaining available credit.

Some issuers allow recently closed accounts to be reopened, typically within 30 to 90 days of closure. Contact the issuer directly to inquire about reinstatement options. Beyond this window, a new application is usually required.

Cards reach their printed expiration dates regardless of usage. However, issuers may choose not to send replacement cards for inactive accounts. The account itself may be closed before the card’s expiration date if inactivity continues.

Generally speaking, keeping no-fee cards open benefits credit scores by maintaining available credit and account history. Making occasional small purchases prevents closure while avoiding costs or debt accumulation.

Reward point policies vary by issuer. Some programs allow points to remain indefinitely, while others expire after 12 to 24 months of account inactivity. Check the specific terms for each rewards program to avoid losing accumulated points.

Yes. Issuers generally have the right to reduce credit limits on inactive accounts without advance notice, though many do provide notifications. Terms and conditions typically grant this authority as part of account management practices.

Taking Control of Inactive Credit Cards

Credit card inactivity creates real consequences—from account closures to credit score impacts. But these outcomes are entirely preventable with minimal effort.

The key lies in strategic account management. Small recurring charges or quarterly purchases keep cards active without creating debt. Monitoring all accounts regularly catches changes before they become problems.

For cards worth keeping, establish simple systems to maintain activity. For those that no longer serve a purpose—especially cards with annual fees—evaluate whether closure makes sense despite potential credit impacts.

Review credit card portfolios today. Identify inactive accounts, assess their value, and implement activation strategies for those worth maintaining. Taking action now prevents unwanted surprises later.